Zynga (ZNGA) is a premier provider of social game services.

The company develops, markets, and operates mobile games as live services played on platforms such as Apple’s iOS and Google’s Android, and social networking platforms (e.g., Facebook and Snapchat), among others.

With all of Zynga’s games remaining free to play, the company generates the majority of its revenues through the sale of in-game virtual items (online game revenue), and advertising services (advertising revenue).

The company has been developing its game portfolio for years, consistently growing revenues and bookings.

The stock has rallied in line with revenues over the years, though it has recently slid significantly. Zynga is currently trading 39.7% lower than its 52-week high of $12.32.

While the mobile gaming industry is extremely competitive, Zynga showcases a robust track record of growing its financials. Following the recent decline, the stock is trading at an attractive valuation considering the company’s profitability growth prospects.

For this reason, I am bullish on the stock. (See Insiders’ Hot Stocks on TipRanks)

Recent Results, Bookings

Zynga’s Q2 results marked another impressive quarter in terms of growth. The company reported the highest quarterly revenue in its history, while bookings remained near record levels.

Revenue reached a record high of $720 million, up 59% year-over-year, while bookings closed at $712 million, up 37% versus the prior-year period.

It’s quite noteworthy that bookings growth remains robust, as this represents the commitment of a customer (e.g., an advertiser) to spend money with Zynga.

To simplify, think of bookings as a contract with a customer who has signed, but hasn’t yet used the service, nor paid Zynga. For example, assume that a customer signs up for a 12-month deal to advertise around $100 a month, at the start of Q2.

Because they are committing to spending $1,200 with Zynga, the company will recognize $1,200 in bookings, but only $300 in revenues for Q2. Total bookings, therefore, refer to total revenues adjusted for change in deferred revenues (cash not yet collected, but expected), which is derived from the sale of virtual items.

Due to the company’s bookings hovering near record levels, Q3 and Q4 revenues should also come out strong.

Profitability, Valuation

Due to Zynga’s digital business model being incredibly scalable, the company’s gross margins are equally juicy. They stood at 64.8% in Q2.

In terms of the bottom line, Zynga had remained borderline unprofitable over the past few years, as the company kept reinvesting back into the business/acquiring new games.

However, profitability seems to be getting closer and closer, with the company guiding for an adjusted EBITDA of $575 million for the year. Further, Zynga is expected to post EPS of $0.36 for the year, which implies that the stock is trading with a forward P/E of 20.6 attached.

This makes for a very attractive entry point, considering Zynga’s exceptional growth track record, record bookings, and the continuous expansion of video game sales in general.

Wall Street’s Take

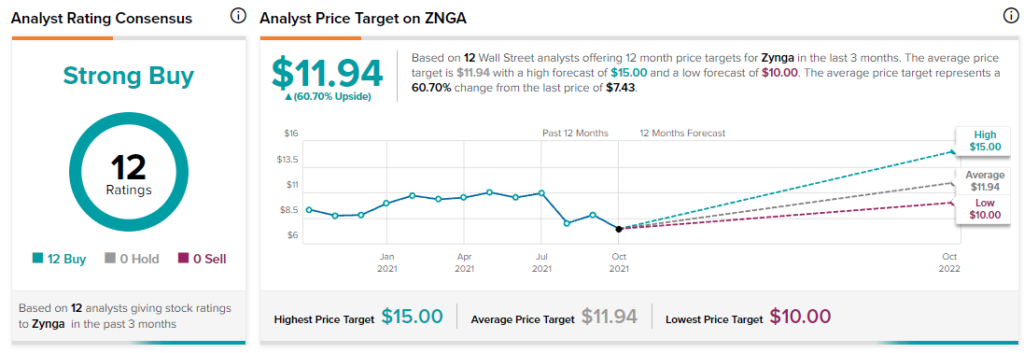

Turning to Wall Street, Zynga has a Strong Buy consensus rating, based on 12 Buys assigned in the past three months. At $11.94, the average Zynga price target implies 60.70% upside potential.

Disclosure: At the time of publication, Nikolaos Sismanis did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.