Macro pressures have significantly hurt stocks in the technology sector, including the mighty FAANG stocks – Meta Platforms (META), previously called Facebook, Amazon (AMZN), Apple (NASDAQ: AAPL), Netflix (NASDAQ: NFLX), and Google’s parent company Alphabet (NASDAQ: GOOGL). Despite the year-to-date pullback, Wall Street analysts remain bullish on some of the FAANG stocks due to their long-term growth prospects and ability to navigate the ongoing challenges. Using the TipRanks Stock Comparison Tool, we placed Apple, Alphabet, and Netflix against each other to pick the best FAANG stock.

Apple

Apple’s earnings per share (EPS) fell nearly 8% to $1.20 for the third quarter of Fiscal 2022 (ended June 25, 2022) amid supply chain pressures, inflation, and currency headwinds. That said, the company surpassed analysts’ earnings and revenue expectations, driven by strong execution.

Apple’s revenue grew 1.9% to $82.96 billion, as higher iPhone sales and increased Services revenue more than offset lower sales of Mac computers, iPads, and wearables. Despite a tough operating environment, iPhone sales grew 2.8%, reflecting strong demand trends.

Looking ahead, Apple expects revenue growth to accelerate in Q4 FY22 despite forex headwinds. It anticipates supply constraints to persist in Q4 but expects the impact to be lower than in Q3. Also, Apple expects Services revenue to increase in Q4, but decelerate compared to the June quarter due to macro challenges and currency fluctuations.

Following the print, Raymond James analyst Melissa Fairbanks lowered her price target for Apple stock to $185 from $190 but maintained a Buy rating. Fairbanks highlighted Apple’s strong June quarter despite multiple headwinds, like currency movements, China lockdowns, macroeconomic challenges, and component shortages.

The analyst noted that while Apple didn’t issue a specific Q4 FY22 guidance, management’s outlook commentary seems better than what consumer trends suggest. Fairbanks remains optimistic that Apple would weather the storm better than other consumer device makers.

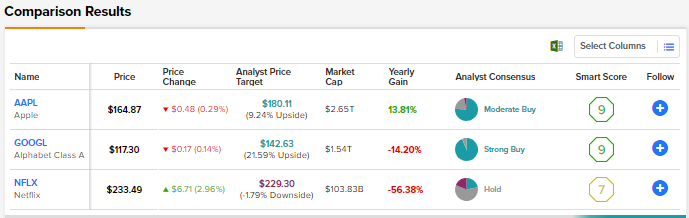

Overall, the Street is cautiously optimistic on Apple stock, with a Moderate Buy consensus rating based on 22 Buys, six Holds, and one Sell. At $180.11, the average price target implies 9.24% upside potential from current levels.

Alphabet

Alphabet’s second-quarter results lagged analysts’ expectations, but investors were still relieved as the company displayed resilience compared to its peers who are also dependent on online ad spending, like Snap (SNAP).

Alphabet’s Q2 revenue grew 13% to $69.7 billion, fueled by Google Search and Cloud businesses. However, EPS came in at $1.21, down 11% as increased costs and losses on certain investments weighed on the bottom line.

Alphabet is facing tough year-over-year comparisons. Also, competition from players like TikTok is impacting its YouTube revenues. However, the company’s Google Search business continues to display strength despite near-term pressures. Google Search and other advertising revenues grew 13.5% to $40.7 billion in Q2, thanks to travel and retail.

Recently, Tigress Financial analyst Ivan Feinseth raised his price target for Alphabet stock to $186 from $183, and maintained a Buy rating. The analyst noted that management’s Q2 earnings commentary emphasized the strength in ad spending as Alphabet’s “search model is not subject to privacy restrictions that limit app-embedded advertising.”

Feinseth believes that the company’s artificial intelligence investments are driving “increasingly focused and helpful experiences for users and businesses across all key product lines.”

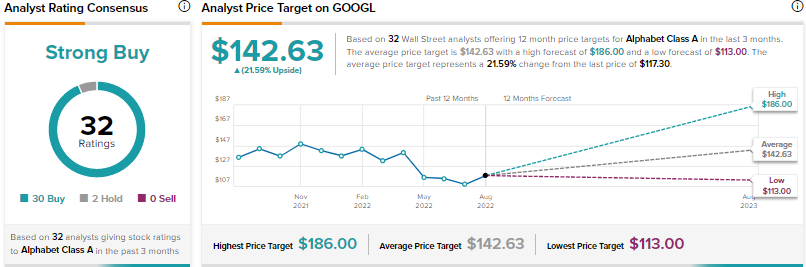

Overall, Alphabet earns a Strong Buy consensus rating backed by 30 Buys and two Holds. The average price target of $142.63 implies 21.59% upside potential from current levels.

Netflix

Streaming giant Netflix delivered revenue of $7.97 billion in Q2, reflecting an increase of 8.6%. While the company’s revenue missed Wall Street’s expectations, EPS grew 7.7% to $3.20 and surpassed estimates.

Despite mixed results, investors reacted positively as Netflix lost fewer subscribers than it had earlier predicted. The company lost nearly 970,000 subscribers in the second quarter, lower than its guidance of a loss of 2 million subscribers. Netflix cited better content, mainly Stranger Things, and other efforts, as the reasons for the better-than-feared subscriber numbers.

For Q3, Netflix anticipates revenue to grow by 5% and the addition of one million net new subscribers. However, analysts were expecting 1.8 million new subscribers.

From working on better content to implementing a crackdown on password sharing, Netflix is taking several measures to ensure better performance. The company expects to launch its lower-cost, ad-supported tier in early 2023. Under a recently announced deal, Microsoft (MSFT) will be Netflix’s technology and sales partner for the launch of the ad-supported tier.

Oppenheimer analyst Jed Kelly believes that any near-term upside in Netflix stock could be quickly moderated by increased churn concerns due to streaming competition and inflationary pressures. However, the analyst views the ad-supported tier and the password-sharing crackdown as two catalysts to re-accelerate top-line growth. Kelly opines that these catalysts along with easing comparisons present an attractive set-up heading into next year. For now, Kelly reiterated a Hold rating on Netflix stock.

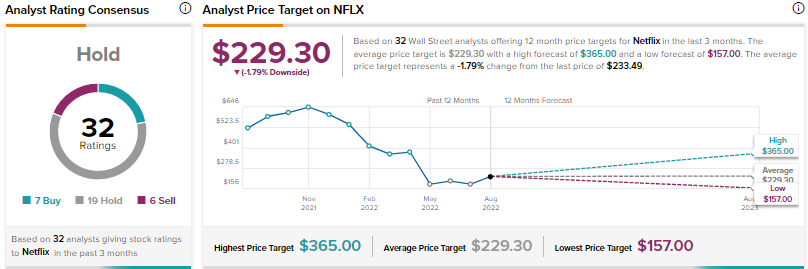

Overall, analysts are sidelined on Netflix stock, with a Hold consensus rating based on seven Buys, 19 Holds, and six Sells. The average price target of $229.30 implies a 1.79% possible downside from current levels. Netflix stock is down over 60% year-to-date.

Conclusion

FAANG stocks could continue to face macro pressures and currency headwinds over the near term. Despite near-term challenges, Wall Street analysts are highly bullish on Alphabet based on the dominant position of Google Search, tremendous growth opportunities in the Cloud, and strong cash flows that can support the company’s Other Bets division. Furthermore, Wall Street analysts estimate that Alphabet stock has higher upside potential than Apple and Netflix combined.

As per TipRanks Smart Score System, Alphabet scores a nine out of 10, indicating that the stock might outperform the broader market.