The recent wave of market selling has hit the retail stocks in recent weeks, with the broader basket falling in anticipation of a consumer slowdown. The Federal Reserve is raising rates at a staggering pace. Another 75 bps (triple) hike could hit in July and induce even more pain to the consumer-facing retailers.

Indeed, the stage seems set for stagflation in the second half, with many retailers delivering downbeat forecasts and consumers looking to tighten in response to pressures on their personal budgets.

As the Fed attempts to engineer a “soft-ish” landing, retail stocks are sure to be stomach-churningly volatile over the coming quarters. Still, with recession risks mostly baked into certain retail stocks, Wall Street may not be so quick to turn their backs at the first signs of weakness.

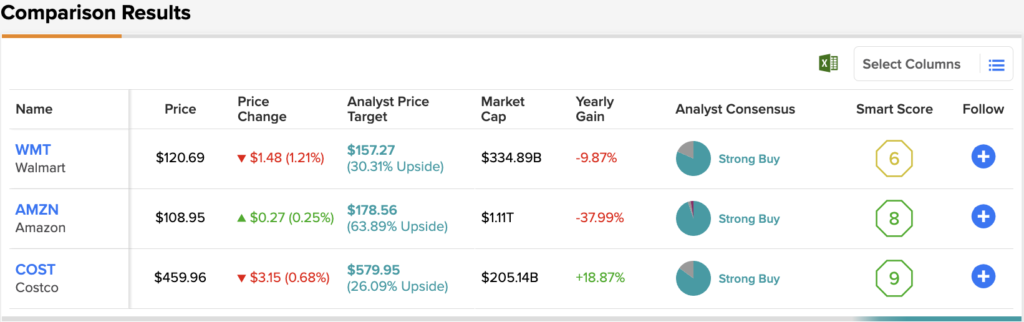

In this piece, we used TipRanks’ Comparison Tool to evaluate three retailers that may be oversold and undervalued.

Walmart (WMT)

Walmart is a retail behemoth that’s shed around 25% of its value from peak to trough. Thanks in part to weak market-wide sentiment and a tough quarterly earnings result, Walmart now finds itself in a tough spot as it continues to fight off inflationary headwinds and ongoing pandemic disruptions.

In an inflationary environment, many consumers have flocked to low-cost retailers like Walmart. Sales for the latest quarter were robust. Still, the margin pressures were a major reason investors decided to bail on the stock. Walmart is an incredibly well-run company with exceptional purchasing power. However, it’s hard for any firm to avoid the impact of high inflation.

In due time, the Fed will stomp out inflation and Walmart’s margin pressures will come to pass. Though a resulting economic slowdown could impact retail sales, Walmart’s low-cost edge over rivals will help it avoid a substantial sales plunge. If anything, tougher times should incentivize consumers to gravitate towards lower-cost retailers that offer a better bang for one’s buck.

Walmart’s cost profile will normalize in due time. Until then, expect the stock to be a choppy ride until inflation data shows some sort of peak. At writing, Walmart stock trades at 26.3 times trailing earnings and 0.6 times sales, with a 1.83% dividend yield.

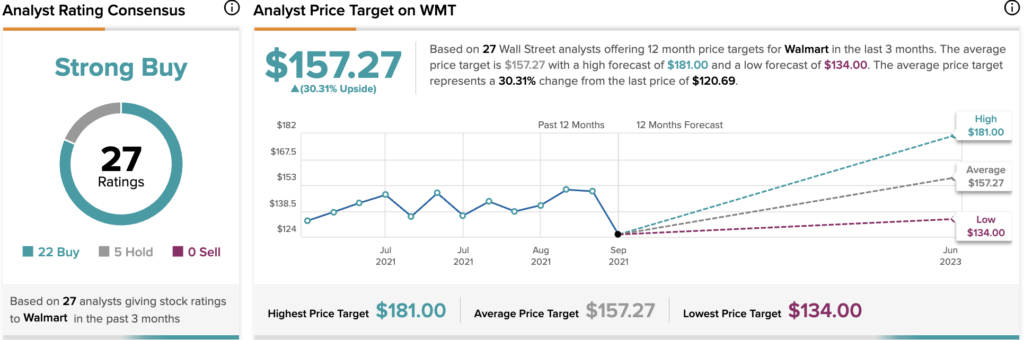

Turning to Wall Street, analysts are bullish, with the average Walmart price target of $157.27 implying 30.31% upside.

Amazon (AMZN)

Amazon is an e-commerce beast that lost more than 42% of its value from peak to trough. Undoubtedly, Amazon stock was expensive from a price-to-earnings (P/E) perspective. And it still is at over 52 times trailing earnings. The Fed’s raising of interest rates really has acted as a one-two punch to the gut of the e-commerce pioneer, as it blew up the growth trade while diminishing the economic outlook.

Despite the damage, Amazon remains a company that’s not about to slow down with its disruptive capabilities. Sure, recent quarters were underwhelming, with a per-share earnings loss of $0.38, well below the analyst consensus estimate of a $0.42 per-share gain. Overinvestment in capacity, inflationary pressures, and pandemic-induced supply woes were just some of the many factors to blame.

Indeed, Andy Jassy’s reign at Amazon has not been pretty. Whether or not the stock’s underperformance entices Jeff Bezos to make a return to the CEO seat remains a mystery. In any case, Amazon stock seems extremely oversold, with a modest 2.3 times sales multiple.

Amazon is investing heavily in its future and it’s ready to disturb new markets, even in a recession. At the end of the day, Amazon is a disruptor that’s to be feared. With its “Buy with Prime” service likely to take share in the logistics market, I remain incredibly upbeat on AMZN stock as it attempts to stage a comeback from one of its worst pullbacks in years.

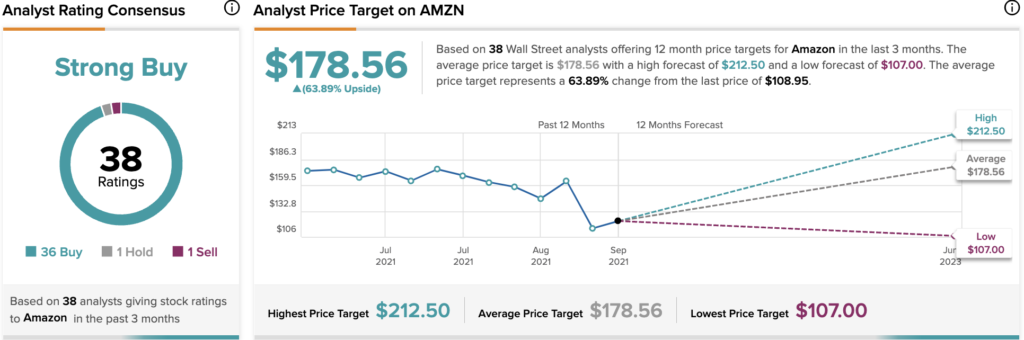

Wall Street remains extremely bullish, with the average Amazon price target of $178.56 implying 63.89% upside.

Costco (COST)

Costco is a big-box retail powerhouse that also took several jabs to the chin in the first half. The stock shed over 31% of its value before partially rebounding to $463 and change per share, off about 24% from its peak.

For its latest (third) quarter, it was the same story as most other retailers. Margin pressures, inflationary headwinds, but robust sales. Indeed, Costco is one of the best-manged firms out there, yet it was not able to avoid the blow of inflationary headwinds.

Like Walmart, Costco can offer consumers a deal they just cannot refuse, making the retailer an intriguing play as economic growth hits the consumer. With strong membership loyalty and unrivaled procurement leverage, Costco seems to be one of the best plays to weather the coming storm.

Though e-commerce isn’t Costco’s strong point, the firm could evolve to become a force to be reckoned with online, as Charlie Munger recently noted. In any case, Costco is best-in-breed, with the tools to get out of the recent market-wide downfall. The stock trades at 36.5 times trailing earnings and 0.9 times sales. Not at all cheap, but you’ve got to pay up for quality.

Wall Street is staying bullish, with the average Costco price target of $579.95 implying 26.09% upside.

Conclusion

Retail has been hit hard of late over the same slate of inflationary and pandemic pressures. Such margin-dragging headwinds will eventually subside, as COVID-19 abates while the Fed gets serious about fighting inflation. Once things normalize, it’s these three retail stocks that could make up for the lost time.

Currently, Wall Street is most bullish on Amazon – and it’s hard to disagree, given it’s still going full speed ahead on the innovation front.