Cathie Wood’s ARK Innovation Fund (ARKK) boomed in the early days of the pandemic, only to go bust in a big way in 2022. Not all innovation stocks are created equally. Some are better equipped than others to recover. In this piece, we used TipRanks’ Comparison tool to look at three ARKK stocks that Wall Street analysts are bullish on over the year ahead. The three stocks are SQ, NTLA, and EXAS.

Year-to-date, shares of Wood’s flagship ARKK have sunk by around 50%. From peak to trough, shares lost more than 75% of their value. Though ARKK has begun to trend higher again, now trading at $50 and change per share (down around 68% from its peak), a bottom may be difficult to sustain, given the many laggards in the portfolio that could continue to drag their feet as a result of higher interest rates and decaying economic growth.

Undoubtedly, ARKK was a high-reward/high-reward type of trade, and it still seems to be. Though Wood has been busy buying the dip in some of her favorite constituents, I think investors may find it wiser to pick and choose individual ARKK names that do have a stage set for a remarkable relief rally.

Block (SQ)

Leading off the list, we have Jack Dorsey’s fintech firm Block, formerly known as Square. Dorsey renamed the company last year to shed more light on its blockchain ambitions. Undoubtedly, strategic pivots, company name changes, and a broadening of industry focus have been quite common for tech firms over the past two years.

With so much damage in the rear-view mirror (SQ shares lost nearly 80% of their value from peak to trough), many dip-buying Dorsey believers have been quick to snatch up the stock in recent weeks amid the broader market’s relief rally.

Recently, Block clocked in a decent quarterly earnings beat that investors didn’t take too kindly to. Although per-share earnings of $0.18 beat the consensus estimate of $0.17, it was hard to look past the slowed revenue growth. Excluding BNPL (Buy Now Pay Later) firm Afterpay, Block saw revenues grow just 24% year-over-year – pretty sluggish growth for a firm that’s averaged north of 70% sales growth over the last three years.

Cash App, Block’s mobile payment service, took a hit to the chin as a result of weakness in bitcoin. As the so-called “crypto winter” takes hold, bitcoin (BTC-USD) revenues could remain unimpressive for some time.

Further, the implications of Dorsey’s forward-thinking bitcoin and blockchain-related projects remain unclear. In any case, Cathie Wood is still a big fan of SQ stock over rivals due to Cash App’s greater relative focus on bitcoin.

Currently, Block stock has fallen to become the fourth-largest holding in the ARKK ETF. Even with crypto’s crash considered, it’s hard to imagine Cathie Wood throwing in the towel on the payments darling, especially while it’s trading at a mere 3.1 times sales.

Many Wall Street analysts also continue to recommend the name, with 28 Buys, seven Holds, and just one Sell assigned in the past three months. The average SQ price target of $113.58 suggests 32.8% upside over the year ahead, which is pretty solid for one of the most influential companies in the fintech space.

Intellia Therapeutics (NTLA)

Cathie Wood is a huge fan of innovation to be had in the biotech sector. She has a genomics-focused ETF but seems to like Intellia Therapeutics stock enough to include it as the ARKK ETF’s 10th largest holding.

Intellia is a genome-editing company that incorporates the intriguing CRISPR-Cas9 technology from CRISPR Therapeutics (CRSP). Undoubtedly, the genomics field is in the nascent stages. Still, Wood is all about emerging technologies, and Intellia stands out as one that holds incredible potential in treating rare diseases.

Recently, the company posted decent second-quarter numbers that missed the mark on the bottom line by the slightest of margins. Per-share earnings came in at -$1.33, just shy of the analyst consensus calling for -$1.28. Revenue came in at $14 million, up 25% quarter-over-quarter.

Indeed, Intellia is one of the most exciting high-growth companies out there. However, its revenue (just $14 million in the latest quarter) is still dwarfed by its market cap of just shy of $5 billion.

Though shares look to be turning a corner after shedding more than 75% from peak to trough, investors must be willing to look way into the future for NTLA stock to justify its valuation. The company’s pipeline is full of promise. However, it could take many years before the pipeline yields something that drives sales growth through the roof.

At writing, shares trade at a whopping 106.4 times sales. That’s an exorbitant price tag, to say the least, and it’s one that requires investors to have patience and faith in management and the company’s early-stage pipeline.

Despite the lofty valuation and profound uncertainties, Wall Street loves the stock, with a “Strong Buy” consensus rating. Of the 16 analysts covering the name, 13 have it as a Buy, with three Holds and zero Sells. The consensus price target of $108.79 implies 71.4% upside potential.

Exact Sciences (EXAS)

Exact Sciences is another pie-in-the-sky biotechnology company that’s full of potential. The firm is a cancer diagnostics company that offers a range of testing solutions to detect early-stage cancer. Cologuard, a colorectal cancer test, is perhaps the firm’s best-known product. The test accounts for nearly two-thirds of total sales and is an intriguing option for those reluctant to embrace more invasive forms of screening.

The company isn’t profitable and may not be for quite some time. The dependence on Cologuard for revenue also acts as a single source of failure. Though Exact has a front-row seat to a massive cancer diagnostics market, the company could remain relatively undiversified for quite some time. Further, hefty R&D expenses could eat into profitability for many years to come. In an era of rising interest rates, that’s not a good thing.

In any case, Cologuard is an incredibly promising innovation that’s more than capable of disrupting its market. The stock trades at a pretty comfortable 4.3 times sales, which is not all too bad for a firm that holds so much growth potential.

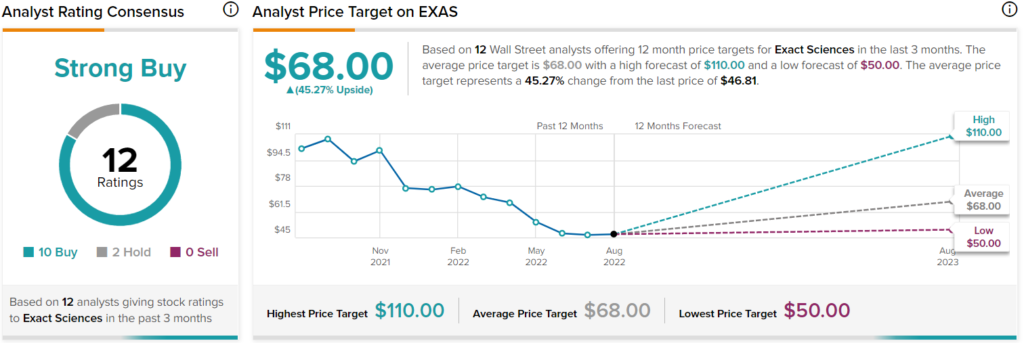

Checking in with Wall Street, analysts are overwhelmingly bullish, with 10 Buys, two Holds, and a Street-high price target of $110.00 that implies over 130% upside from current levels. That’s much higher than the consensus price target of $68, which calls for 45.3% upside potential in the year ahead.

Conclusion: Analysts Believe NTLA Stock is the Strongest Buy

Cathie Wood’s innovative tech stocks are not for the faint of heart. They’ve as innovative as they come, with huge upside potential but with considerable downside risks. Of the three ARKK stocks in this piece, Wall Street expects the most from NTLA stock.