Shares of San Francisco-based genetic testing and data company Invitae Corporation (NVTA) exploded higher after reporting earnings Tuesday night. After 6.5 trading hours on Wednesday, Invitae stock had nearly tripled in value before traders began cashing in some gains. In fact, on Thursday the stock has returned over half of yesterday’s gains, trading 47% lower.

While investors were initially thrilled by the news, Morgan Stanley analyst Tejas Savant observed there were actually “no surprises” in Invitae’s report, given that most of what the company announced had already been pre-announced three weeks ago, when Invitae paired the revelation that its CEO was stepping down with an earnings warning.

Is this something that should worry investors?

Just like Invitae said back in July, Q2 2022 revenues ended up growing 18% year over year, to $136.6 million, with testing volumes growing 20%. Gross profit margins came in at just 19.2% — down nearly half from the 35.4% margins enjoyed in Q2 2021. Cash burn in the quarter was slower than last quarter, but still an unhealthy $147 million.

And of course, Invitae lost money for the quarter: $2.5 billion in net losses, or $10.87 per share — quite a lot for a stock that started the day costing only $2.29 per share.

So, what can possibly explain the share price jump?

Well, there’s the fact that most of Invitae’s loss was a non-cash loss, due to “a complete write-down of goodwill of $2.3 billion, which was a result of a significant, sustained decline in the stock price and related market capitalization and a lower than expected financial performance.” That’s a true one-time event that’s not likely to be repeated anytime soon (one hopes). And even Savant admits that Invitae has taken some “positive steps towards recovery.”

The company served 11% more patients in Q2 than in Q1, for example. It also collected 15% more revenue per patient served in Q2 than in Q1, while cutting its operating costs as a percentage of revenue.

That being said, guidance today is the same as it was three weeks ago. Management is standing pat on its July prediction of $505 million to $520 million in fiscal 2022 sales, down from its previous prediction of $640 million. Gross margins are likely to recover to no more than 42% or 43% for the year. And cash burn for the year could be as high as $650 million.

Granted, cash burn is scheduled to decline by more than half in 2023, to a range of between $225 million and $275 million, and sales growth could resume in 2023 in somewhere between the 15% to 25% range. For the time being, those prospects are enough to convince Savant to stick with an “equal-weight” (i.e. Neutral) rating on Invitae stock. That being said, he still thinks the shares are worth no more than $4 apiece. (To watch Savant’s track record, click here)

With Invitae having shot up to twice that price already on Wednesday, one shouldn’t be at all surprised to see today’s 47% crash.

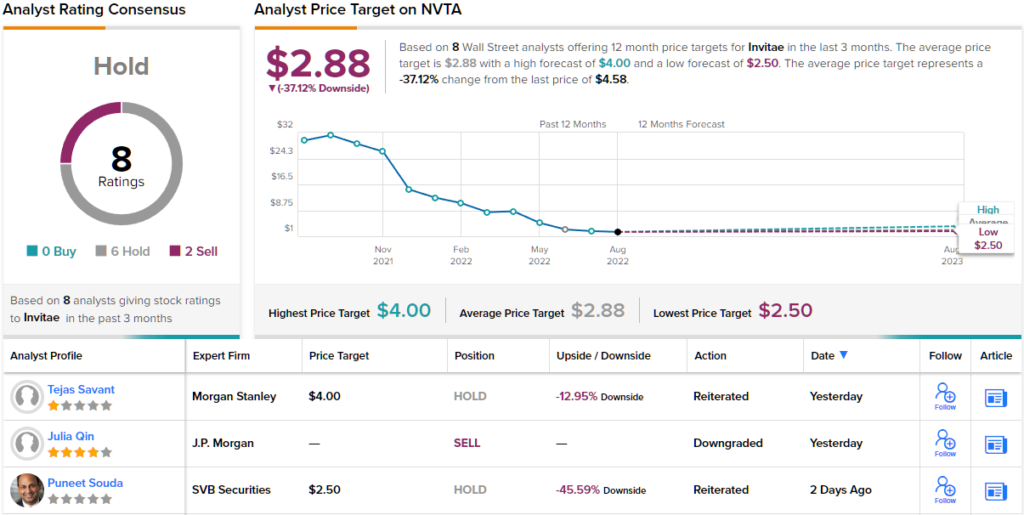

Overall, Wall Street appears to agree with Savant that caution is required here. The analyst consensus on this stock is a Hold, based on 8 ratings that include 6 Holds and 2 Sells. At $2.88, the average price target implies a 37% downside from the current share price of $4.59. (See NVTA stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.