Waste Management (WM) is a recession-resilient company that has rewarded long-term shareholders through an increasing stock price and dividend per share.

The stock is near all-time highs, and is currently up 33.7% year-to-date. The company provides waste management environmental services to residential, commercial, industrial, and municipal customers in North America.

As of December 31, 2020, WM owned or operated 263 solid waste landfills, five secure hazardous waste landfills, 103 materials recovery facilities (MRFs), and 348 transfer stations.

We are neutral on Waste Management. (See Waste Management stock charts on TipRanks)

Industry Analysis

The North American waste management market size is expected to reach $229.3 billion by 2027, from $208 billion in 2019.

Urbanization and industrialization are expected to create large amounts of waste, which increases the demand for intelligent waste systems. Since waste management is a growing and recession-resilient industry, it is an attractive theme to invest into and is generally less volatile.

This is good news for risk-averse investors, as Waste Management stock’s beta is 0.82, meaning it is less volatile than the S&P 500.

Another bonus when it comes to investing in this industry is that these kinds of companies often experience “natural monopolies.” Natural monopolies typically exist due to high barriers to entry. This is why you probably always see the same company coming to collect your garbage every week.

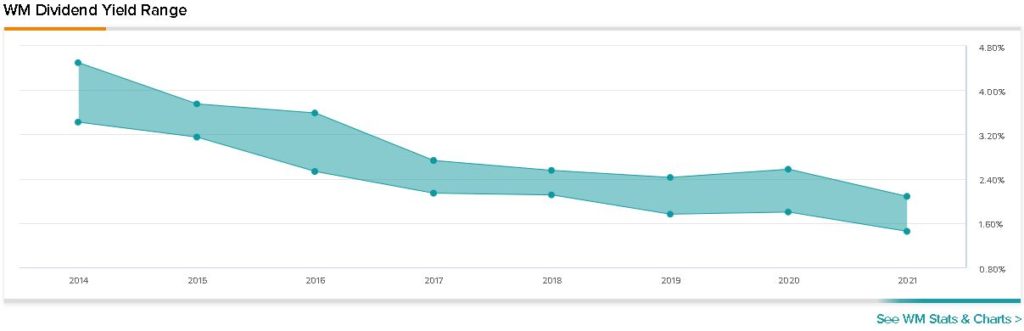

Steady, Unspectacular Dividends

WM’s current dividend yield is about 1.5%, which is not high by any means. The dividend is steadily growing though. Five years ago, its quarterly dividend was $0.41 per share, and now it is $0.575 per share, a 7% CAGR. It is also safe, since WM’s payout ratio is 60.15%.

This dividend growth rate is low when combined with the low 1.5% dividend yield. If its dividend was to continue growing at 7% a year for the next 10 years, it would bring your yield on cost to 3% 10 years from now, which is still low.

Therefore, WM isn’t the best value for a dividend investment. The yield has been steadily going down over the years as the stock keeps rising.

What Else?

There are lots of things to like about WM. As stated earlier, high barriers to entry allow companies like WM to enjoy competitive advantages.

These competitive advantages are proven in the numbers as well. For example, WM’s gross profit margins have steadily grown from 36.2% in 2011 to 39% now, indicating that competition is not eating into its profits.

This stability comes at an expensive price, however. The company’s trailing 12-month EV/FCF multiple is currently 31.4x. If the company can continue growing in the next few years around the 10% range, then it may be justified to hold the stock.

Its current valuation doesn’t leave much room for outperforming the market though.

Wall Street’s Take

Turning to Wall Street, Waste Management has a Hold consensus rating, based on three Buys, four Holds and two Sells assigned in the past three months. The average WM price target of $153.44 suggests very little movement in share price over the next 12 months.

Final Thoughts

Waste Management is a good company that has treated shareholders well over the long run, and will probably continue doing so going forward.

However, there are likely better opportunities elsewhere.

Disclosure: At the time of publication, Stock Bros Research did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.