The rising global economic unpredictability emerging due to supply chain logjams, higher inflation, and an uptick in interest rates does not seem to have dampened the enthusiasm of U.S. consumers when it comes to spending.

So far, data from all three credit card giants including Visa, Mastercard, and American Express has echoed the same sentiment – that U.S. consumers are spending more. Data from American Express indicated that in Q1, consumers in the U.S. spent around 20% on travel and entertainment, adjusting for exchange rate fluctuations, when compared to the same time period in 2019.

Last week, we compared Visa and Mastercard just before the two companies were going to announce their Q1 earnings. This week, let us look at how the three major credit card companies, Visa, Mastercard, and American Express are likely to fare following their calendar Q1 earnings using the TipRanks stock comparison tool.

We will also look at what Wall Street analysts are saying about these stocks post their-Q1 earnings.

Visa (NYSE: V)

Shares of Visa are up 3.3% in the last five days as the global payments technology giant announced its fiscal Q2 earnings last week. The company delivered strong quarterly results even amid geopolitical uncertainty and its decision to suspend operations in Russia.

Visa generated net revenues of $7.2 billion, up 25% year-over-year, surpassing consensus estimates of $6.83 billion. Adjusted earnings came in at $1.79 per share, up 30% year-over-year and beating analysts’ estimates of $1.65 per share.

Alfred F. Kelly Jr., Chairman and CEO of Visa commented, “We had solid growth in most countries around the globe and across all elements of our business, with revenue growth of over 20% in consumer payments, new flows and value added services.”

When it came to Visa’s outlook for the rest of this year, it expects that suspension of its business in Russia could result in its H2 revenues this year declining by 4%. The company anticipates that the growth in its domestic payments volume will remain robust.

Regarding international payment volumes, there appears to be no impact even with the current uncertainties regarding high inflation, supply chain constraints, the conflict between Russia and Ukraine, and rising interest rates.

Robert W. Baird analyst David Koning remained bullish on the stock following the print, assigning a Buy rating with a price target of $290 on the stock. Koning’s price target implies an upside potential of 36.1% on the stock at levels seen before market open on Monday.

The analyst’s investment rationale for the stock includes a few key positives. Those being significant barriers to entry for Visa’s competitors given the company’s “well-established brand and extensive merchant-acceptance network,” and the rising shift towards card payments.

By Koning’s estimate, the market share for card payments in the U.S. has grown from 32% in 2001 to more than 50% in 2014, will and continue to increase further. The analyst is upbeat about Visa’s growth in international markets and believes that these markets “can generate double-digit growth over the next several years, driven by consumer spending and the shift to cards.”

Other positives for the stock include Visa’s “highly fixed” processing costs that create “very high incremental margins (85-90%+)” and a recovery in international travel that could see higher cross-border transaction fees as a proportion of Visa’s revenues.

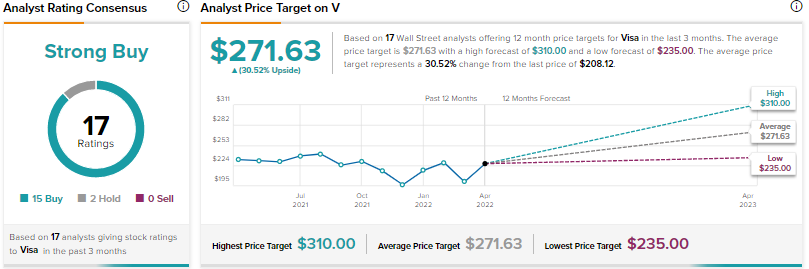

Other analysts on Wall Street are also optimistic about the stock with a Strong Buy consensus rating based on 15 Buys and two Holds. The average Visa stock forecast is $271.63, implying an upside potential of 30.5% from early morning trading levels on Monday.

Mastercard (NYSE: MA)

Mastercard also delivered robust Q1 earnings driven by cross-border volumes that grew 53% year-over-year on a local-currency basis. The credit card giant generated net revenues of $5.2 billion, up 28% year-over-year on a currency-neutral basis which outpaced consensus estimates of $4.91 billion.

Adjusted diluted earnings came in at $2.76 per share, surpassing analysts’ estimates of $2.17 per share by 59 cents.

Michael Miebach, Mastercard’s CEO, commented that while cross-border travel is above 2019 levels for the first time as of March and the company is seeing “strong traction in consumer and small business payments, Mastercard Installments and our work across the digital asset space.”

It was this recovery in cross-border travel that buoyed up Jefferies analyst Trevor Williams following the Q1 earnings. The analyst reiterated a Buy on the stock and raised the price target to $440 from $425, implying an upside potential of 21.1% to early morning trading levels on Monday.

In his report, the analyst added, “The travel recovery has carried momentum into April, consumer spending remains durable, and mgmt. deliberately did not pull its 3yr targets despite Russia dragging the revenue CAGR [Compounded Annual Growth Rate] by 2ppt.”

Wall Street analysts are also bullish about the stock with a Strong Buy consensus rating based on 15 Buys and only one Sell. The average Mastercard stock forecast is $435.06, implying an upside potential of 21.3% from early morning trading levels on Monday.

American Express (NYSE: AXP)

American Express is yet another card company that benefitted from higher spending by credit cardholders in Q1. The company’s earnings came in at $2.73 per share, down one cent year-over-year, beating analysts’ estimates of $2.48 per share. AXP generated net revenues of $11.74 billion, up 29% compared to the year-ago quarter, surpassing estimates of $10.64 billion.

Stephen J. Squeri, Chairman and CEO of American Express stated in the company’s Q1 press release that small to medium-sized businesses and Millennial and Gen Z card members saw strong expenditure, up by 30% and 56%, respectively.

Squeri added that Goods and Services spending, which comprises the largest category of spending on AXP’s network, “continued to accelerate in the quarter, growing 21 percent on an FX-adjusted basis over last year. Travel and Entertainment spending was up 121 percent on an FX-adjusted basis over a year ago and essentially reached pre-pandemic levels globally for the first time in March, driven by continued strength in consumer travel.”

However, AXP’s outlook for FY22 disappointed analysts as AXP anticipates earnings to be in the range of $9.25 and $9.65 per share versus analysts having estimated its EPS to be $9.71 per share. The company estimates revenues to grow in the range of 18% to 20%.

However, Citigroup analyst Arren Cyganovich remained sidelined on the stock with a Hold rating but raised the price target to $190 from $187. According to the analyst, AXP’s earnings beat was more due to lower tax rate and provisions than organic growth.

The rest of the analysts on Wall Street, however, are cautiously optimistic about the stock with a Moderate Buy consensus rating based on eight Buys and eight Holds. The average AXP stock forecast is $203.07, implying an upside potential of 18% from early morning trading levels on Monday.

A Dissenting Opinion

However, Piper Sandler analyst Christopher Donat has been the lone voice of dissent among the overall bullishness on the Street when it comes to Mastercard and Visa. The analyst downgraded Visa to a Hold and MA to a Sell, following their calendar Q1 results.

According to Donat, there is a possibility of Europe entering into a recession in 2023 and as he pointed out, “Europe is MA’s largest region and V’s second largest. We think that a more challenging revenue scenario in 2023 will put future pressure on earnings estimates and the P/E multiples for both companies.”

Excluding Donat, the overall sentiment of Wall Street analysts remains optimistic regarding these three companies.

Discover new investment ideas with data you can trust

Read full Disclaimer & Disclosure.