Despite rising as much as 41% since bottoming out along with the rest of the market in mid-March, Micron (MU) shares are still in the red in 2020 – down by 9%. The performance is particularly galling when compared to the company’s peers in the semiconductor industry. The SOX (The PHLX Semiconductor Sector Index) – the sector’s overall indicator – is up by 19% year-to-date, highlighting Micron’s underperformance.

So, the negative sentiment could mean one of two things. Either Micron’s business is in bad shape and investors are lacking confidence in its ability to perform or that Micron presents an opportunity that is underappreciated by the market. The former, though, is unlikely, going by the company’s latest earnings results; Micron beat on both the top and bottom line.

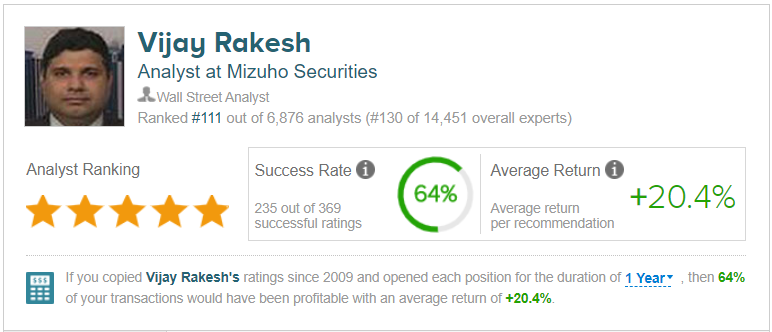

Mizuho analyst Vijay Rakesh belongs squarely in the latter camp. Following a conference call with Micron’s CFO, the 5-star analyst believes Micron is poised to benefit from several secular tailwinds.

The WFH trend should prove a boon to cloud based services. Despite some customers’ inventory builds and a cautious approach to bit supply, Micron’s cloud outlook remains strong as the company “continues to see strong cloud demand with WFH and sees good long-term trends.”

Additionally, the company believes 2021 should be a good year for memory with “5G handsets expected to grow by 100% year-over-year,” the launch of new gaming consoles, and “continued cloud migration.”

Rakesh said, “We believe MU remains well-positioned with handset and gaming driving 50-100% content growth in 2H20… With MU seeing a FebQ trough, we believe 2020E sets up well with improving top line and GMs as DRAM-NAND supply demand moves into balance, with potential undersupply into 2H20E and 5G/Data center as demand drivers. Also, the $10B buyback should be supportive for the stock.”

Accordingly, there is no change to Rakesh’s rating on MU, which remains a Buy. The price target also stays put – and at $63, implies possible upside of 29% over the next 12 months. (To watch Rakesh’s track record, click here)

Overall, Rakesh’s colleagues agree. Based on 18 Buys, 7 holds and 1 Sell, the chipmaker has a Moderate Buy consensus rating. The analysts expect a 33.5% premium will be added to the stock over the following months, as indicated by the $65,10 average price target. (See Micron stock analysis on TipRanks)

To find good ideas for tech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.