With its upbeat recent earnings performance, UnitedHealth (NYSE:UNH) is a promising bet in the healthcare sector, according to analysts. Its raised outlook, Baron Funds Q1 insights, and expansion in the home healthcare industry are likely to cushion the stock price.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Baron Funds Q1 Letter

Baron Funds, an investment management firm, released its “Baron Durable Advantage Fund” first-quarter 2023 investor letter. The fund accumulated 16% gains during the quarter vs. the S&P 500 benchmark generating a 7.5% return in the same period.

The letter highlighted the UnitedHealth Group, which has posted a 5.8% gain in the past 3 months, although on a year-to-date basis, it lost 4.9%. The fund believes that the shares have corrected during Q1, and investor sentiment was side-lined on worries related to Medicare audit program suggested changes, preliminary 2024 Medicare Advantage (MA) rates, and Medicaid recertification impact. The fund remains highly optimistic about UnitedHealth’s rapidly growing MA segment.

Moreover, the TipRanks Hedge Fund Confidence Signal stands at Very Positive for UnitedHealth. The signal is based on the activity of 60 hedge funds in the recent quarter.

UNH’s Upbeat Outlook at the Healthcare Conference

A Goldman Sachs report from the ongoing 44TH Annual Global Healthcare Conference reflects that UnitedHealth expects the upcoming quarter and full-year performance to be highly boosted by elevated care activity mainly due to larger Medicare outpatient volumes. The company now sees results to come in at the higher end of company-provided guidance aided by the higher level of procedure volumes continuing over the balance of the year.

UNH Lower in Early Trade Today. Why?

In pre-market trade today, UNH was down 5.6% after the company CFO, John Rex, at the Goldman Sachs Healthcare conference today said that due to rising demand for certain types of seniors’ surgeries, Q2 costs will be pushed higher. The pandemic forcefully delayed non-urgent procedures related to knees, back and hips for adults which have now surfaced on the demand front with consumers being more comfortable accessing the services.

UNH estimates the Q2 medical loss ratio, the percentage of spend on claims compared to the premiums it collects, to come in at the high end or marginally above its full-year outlook of 82.1% to 83.1%.

Separately, UnitedHealth’s all-cash $3.26 billion acquisition of Amedisys in early June falls in-line with what CFO stated in the recent conference on expansion into the home health and hospice care industry. Early this year, UNH also acquired home healthcare company, LHC Group in a $5.4 billion deal.

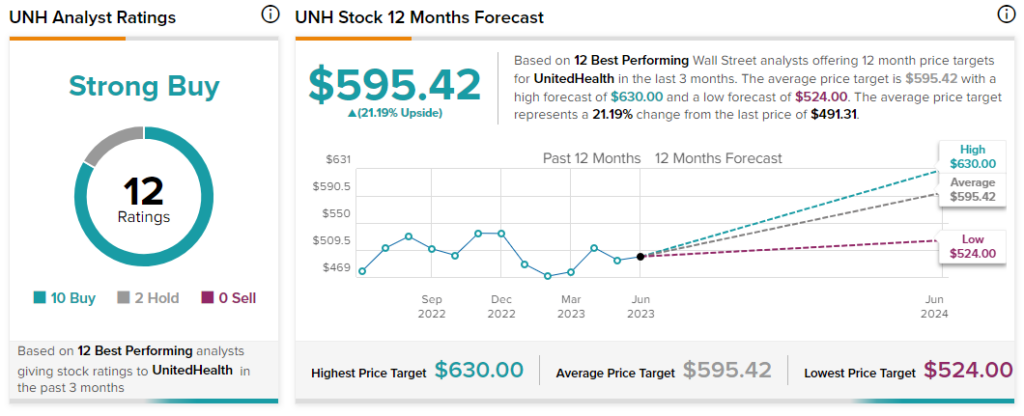

What do Analysts Say About UNH Stock?

Of the 12 Top Wall Street Analysts covering the stock, ten rate it a Buy while two assign it a Hold rating, taking the consensus rating to a Strong Buy. The average analyst price target stands at $595.42, marking a 21.2% upside potential.

Today, Barclays Analyst Steven Valiquette reaffirmed his Buy rating on the stock with a price target of $565 implying a 15% upside potential.