Everyone is hoping the market might be bottoming and by the recent actions of Bank of America clients, some evidently think the lows must be in sight.

Last week, BofA customers splashed out $6.1 billion on US stocks, in what amounted to the third largest inflow since 2008.

While the bank has stated it is not as confident the bottom is quite so close, it’s not hard to see why investors feel the time is right to lean into equities. The widespread losses have left scores of beaten-down stocks looking quite cheap, so it might be time to get the stock picking rod out and go for some bottom fishing.

With this in mind, we dived into the TipRanks database and pulled out three such names that have taken it on the head in 2022. All are down by more than 40% this year, but that quirk aside, they also share another characteristic; all 3 are rated as Strong Buys by the analyst consensus and are projected to pick up steam in the months ahead. Let’s see why the Street’s experts think these names make good investment choices right now.

Sprinklr, Inc. (CXM)

If we’re on the subject of beaten-down names, then a good place to start would be in the tech sector, a corner of the market that has been particularly hard-hit this year. Sprinklr is a SaaS company specializing in customer experience management solutions. The company’s AI-powered platform, Unified-CXM, helps its clients monitor and interact with customers with the aim of delivering better experiences. Some of the world’s biggest brands are clients, including Microsoft, Adobe and Oracle, amongst others.

Sprinklr is relatively new to the public markets, having held its IPO in June 2021, in a downsized offering for which the company raised $266 million. The shares were priced at $16 each but have had a rough time so far. In 2022 alone, the shares are down by 44%.

That said, the share losses have come against an expanding top-line, with revenues steadily growing in each subsequent quarter. In the latest report, for FQ2, revenue increased by 26.9% year-over-year to reach $150.6 million, edging ahead of the consensus estimate by $3.15 million. There have also been consistent beats on the bottom-line; adj. EPS of -$0.03 beat the -$0.06 expected by the analysts.

Assessing this company’s prospects, JMP analyst Patrick Walravens come down squarely in the bull-camp.

“Overall, we see Sprinklr as an attractive opportunity for long-term capital appreciation for a number of reasons, including: 1) Sprinklr’s AI-powered platform that is designed to listen to and manage customer experience data at massive scale across 36 channels (including TikTok) and has lots of high-value, vertical use cases; 2) the company is pursuing a large market opportunity, which is estimated to be ~$60B; 3) we like the leadership of CEO Ragy Thomas and CFO Manish Sarin, who joined in January and is helping focus the company on profitable growth; 4) we think in a tough macroeconomic environment, Sprinklr is benefiting from a trend to consolidation of solutions,” Walravens wrote.

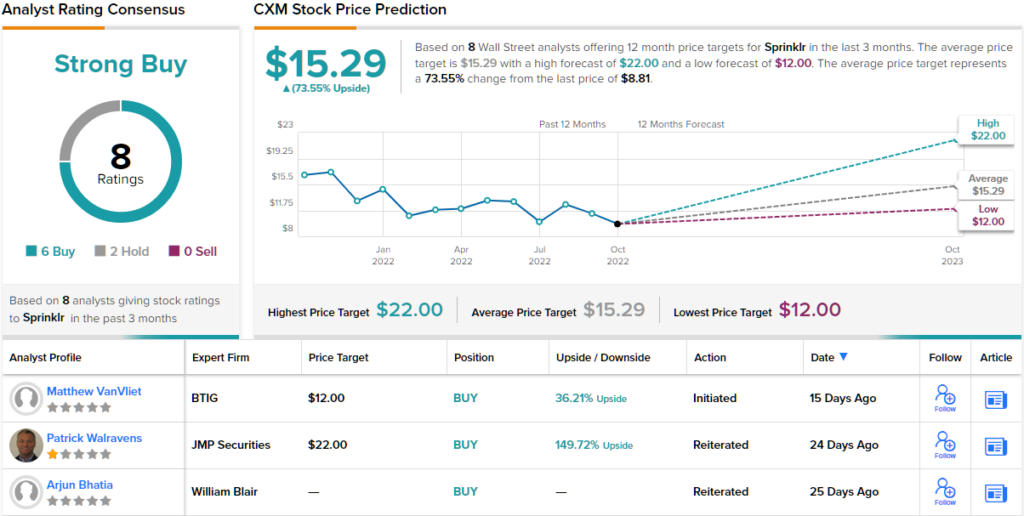

As such, Walravens rates CXM stock an Outperform (i.e. Buy) while his $22 price target makes room for 12-month gains of a strong 150%. (To watch Walravens’ track record, click here)

Overall, most agree this stock is one to own; the ratings split 6 to 2 in favor of Buys over Holds, providing this name with a Strong Buy consensus rating. At $15.29, the average target implies shares will climb ~74% higher over the one-year timeframe. (See CXM stock forecast on TipRanks)

NanoString Technologies (NSTG)

The next beaten-down stock we’ll look at is NanoString, a specialist in the field of spatial biology. That is, the study of molecules in a two-dimensional or three-dimensional context.

In layman’s terms, the company develops advanced instruments which are used in labs for scientific and clinical research. The company offers 3 main products; the nCounter Analysis System, the GeoMx Digital Spatial Profiler (DSP) and the CosMx Spatial Molecular Imager (SMI) platform.

NanoString also recently unveiled its new AtoMx Spatial Informatics Portal (SIP), an integrated ecosystem with streamlined workflows which corresponds with its other platforms. The commercial launch is expected this fall.

2022 has been brutal for this stock, which is down by 76% year-to-date. The share losses have come alongside real world decline, as exhibited in the latest quarterly statement – for 2Q22. Revenue fell by 4.8% from the same period a year ago to $32.22 million while the losses widened too; EPS of -$0.85 dropped from the loss of -$0.60 in 2Q21. Additionally, the company lowered its outlook; total product and service revenue for the year is now expected in the range between $140 and $150 million, vs. the prior guidance of $150 to $160 million, while the company expects an adjusted EBITDA loss of $75 to $85 million, whereas beforehand NanoString called for a loss of $65 to $75 million.

While investors have voted with their thumbs down this year, Canaccord analyst Kyle Mikson remains fully behind this name.

“We remain bullish on NSTG’s spatial biology opportunity,” the analyst said. “We continue to believe that CosMx and GeoMx (combined with AtoMx) should be complementary going forward. Despite recent ‘self-inflicted’ commercial execution issues, we believe NanoString will be able to right-size its sales force to support its full CosMx launch in 2H22. We believe the shares are highly attractive at current levels.”

Mikson isn’t just predicting a strong future, he’s backing his stance with a Buy rating and a $30 price target that implies ~175% one-year upside potential. (To watch Mikson’s track record, click here)

4 other analysts join Mikson in the bull corner, and one skeptic can’t detract from the Strong Buy consensus rating. The forecast calls for 12-month gains of 152%, considering the average target clocks in at $275. (See NSTG stock forecast on TipRanks)

Maravai LifeSciences (MRVI)

From one life sciences company to another; Maravai develops and provides essential products utilized for the purpose of new drug development, diagnostics, human disease research and next-gen vaccines.

The last bit is important as Maravai’s products are being widely used in mRNA-based production and Maravai has enjoyed the prominence seen by mRNA technologies in Covid-19 vaccines.

The most frequently used Covid vaccination on a global scale is the Pfizer/BioNTech Covid vaccine, COMIRNATY, which uses Maravai’s CleanCap mRNA capping technology.

This achievement should bolster Maravai’s prospects for success in the 500+ mRNA vaccines and therapies being developed. It has also provided the company with a sales boost (65% of 2020 to 2022e sales are driven by COVID-vaccines).

That sales bump was still reflected in the company’s most recent earnings report – for 2Q22. Revenue rose by 11.5% year-over-year to $242.73 million, while beating the Street’s call by $9.51 million. EPS of $0.53 also came in well above the $0.38 consensus estimate.

That said, Maravai has been unable to withstand the bearish market forces and the shares have tumbled ~55% this year.

There are also questions regarding the future growth trajectory once the Covid tailwind completely subsides. However, this is not a concern for Credit Suisse’s 5-star analyst Dan Leonard, who points out the growing prevalence of mRNA technology.

“The COVID-19 pandemic accelerated the trajectory of mRNA technologies by multiple years, according to our diligence. The pipeline product candidates for Maravai’s raw materials are broad and deep. According to market research by L.E.K., mRNA/cell and gene therapy assets in development are expected to grow 4x from 2022 to 2027. The FDA expects more than 200 cell and gene therapy INDs per year and 10-20 approvals per year (from nine in total today) starting in 2025. Funding for cell and gene therapies companies totaled ~$20B in 2020,” Leonard explained.

“All in, we view it as an attractive market for suppliers, with Maravai most exposed in our coverage,” the analyst summed up.

Conveying his confidence, Leonard’s Outperform (i.e., Buy) rating is backed by a $34 price target, suggesting an 80% upside from current levels. (To watch Leonard’s track record, click here)

Like Kulkarni, other analysts also take a bullish approach. MRVI’s Strong Buy consensus rating breaks down into 6 Buys and zero Holds or Sells. Given the $35 average price target, the upside potential lands at ~85%. (See MRVI stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.