Visa’s (NYSE:V) shares are riding high on what I believe are three major reasons, which continue to support the stock and make it a worthwhile investment for the rest of 2023. Even though the stock has recorded notable gains lately, I believe that its momentum is set to persist.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

What are these three reasons/catalysts?

Firstly, the rise in nominal global spending, driven by inflation, has resulted in increased demand for Visa’s payment processing services. Secondly, the company’s commitment to returning value to its shareholders has been gaining momentum, with accelerating returns seen in recent years. Lastly, Visa’s stock appears to be trading at an attractive valuation, making it an appealing investment opportunity for investors looking for long-term growth potential. Thus, I am bullish on the stock.

Let’s examine these three reasons individually.

Reason #1: Rising Spending Drives Growth in Revenues, Profits

These days, it’s common to come across warnings in financial news about the possibility of a drop in consumer spending in the event of an economic recession. However, it’s worth noting that, despite any potential decrease in purchasing power, consumer spending (at least in the U.S.) has been consistently reaching new record levels. This is due, in part, to high inflation levels, which result in a rapid increase in the nominal amount of spending.

This is excellent news for Visa. Despite charging the same percentage in each transaction, the company’s revenues are significantly boosted by higher nominal prices. As an example, even my daily espresso now costs about 20% more compared to two years ago, resulting in a 20% increase in fees for Visa every time I swipe my card.

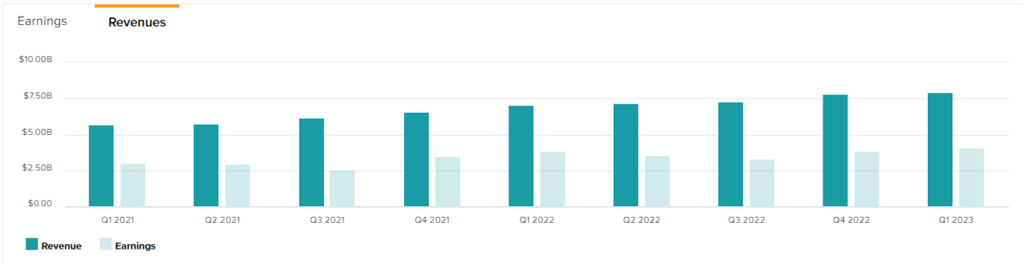

This inflation-driven revenue growth was evident in Visa’s Fiscal 2022 results, which saw an impressive 19% growth in revenue (or 23% in constant currency) thanks to higher nominal consumer spending. This growth continued in Fiscal Q1 2023, with the company posting record quarterly net revenues of $7.94 billion, a 12.4% increase, confirming Visa’s persistent trend of inflation-backed growth.

But here’s where Visa’s frictionless, lean business model shines, allowing the company to grow its profits at an even swifter pace. Specifically, not only does the company benefit from inflation, but due to its business model incorporating essentially no costs (gross margins are virtually 100%), inflation has no negative effect on the company’s profitability.

In fact, the combination of higher revenues against relatively stable costs allows its already tremendous margins to expand further, driving impressive net income growth. Last year, for instance, Visa’s net income rose by 21.5% (higher than revenue growth), with its net income margins landing at a jaw-dropping 51%.

Over the past eight quarters, inflation has steadily decreased, with February’s inflation rate clocking in at around 6%. Despite this decline, it still exceeds historical norms, which bodes well for Visa’s financial performance in the foreseeable future. In fact, even if we assume a gradual improvement in inflation, Visa’s financials are still expected to reap the benefits of this positive trend for several quarters to come.

Reason #2: Accelerating Capital Return Growth

The second catalyst that should keep investor interest in Visa quite strong is the company’s accelerating capital return growth. As we previously discussed, the company’s financials have been recently growing at an above-average pace, allowing Visa’s management to leverage this opportunity to generously reward shareholders with accelerated dividend hikes and buybacks.

Regarding the dividend, back in October, Visa announced its 15th consecutive annual dividend increase, which was by 20% to a quarterly rate of $0.45. This hike marked a significant acceleration compared to the 17.2% and 6.7% increases in 2021 and 2020, respectively.

Furthermore, Visa seized upon its heightened profitability to drastically ramp up its share buyback efforts. In Fiscal 2022, the company completed the repurchase of $11.7 billion in stock. To put this in perspective, Visa’s buyback activity had previously fluctuated between $7 billion and $9 billion over the course of the preceding six years.

Looking ahead, it appears that the accelerated buyback program will remain a potent catalyst in driving the stock higher. The impressive fiscal Q1-2023 repurchase figure, which reached $3.23 billion, suggests an annualized buyback rate of around $12.9 billion that has sparked anticipation for another record-breaking year of repurchases.

Reason #3: A Reasonable Valuation

The third catalyst that should positively contribute to Visa’s investment case moving forward is the fact that shares are now trading at a much more reasonable valuation relative to their past levels.

Despite experiencing a surge in recent times, the current trading levels of Visa’s shares have not surpassed those seen around two years ago. Nevertheless, during this period, Visa’s earnings have experienced significant growth. As a consequence, the stock is now trading at a much more rational valuation.

Consensus EPS estimates for Fiscal 2023 average $8.48, suggesting Visa is currently trading at a forward P/E of 26.6. At first glance, this is an elevated multiple, given the levels where interest rates are hovering. Still, taking into account Visa’s qualities, favorable operating environment, massive margins, and the fact that Wall Street expects the stock’s EPS to grow at a compound annual growth rate in the mid-teens in the coming years, this valuation appears reasonable.

Visa’s boosted buyback program serves as evidence that the company perceives its stock to be undervalued in relation to its projected profitability growth as well.

Is Visa Stock a Buy, According to Analysts?

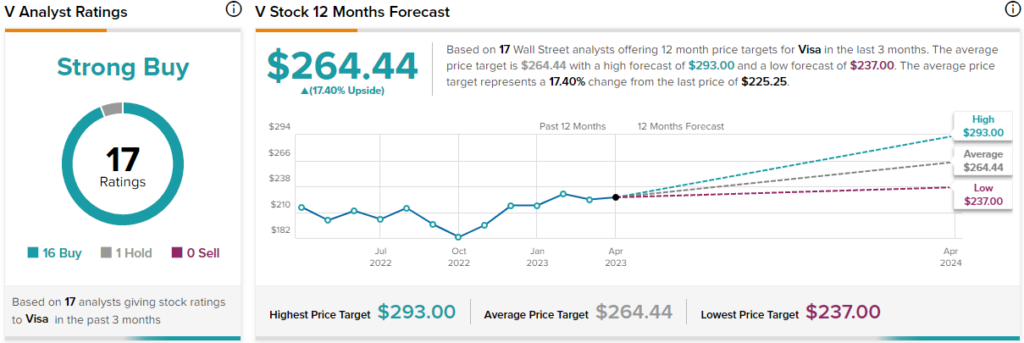

Turning to Wall Street, Visa has a Strong Buy consensus rating based on 16 Buys and one Hold assigned in the past three months. At $264.44, the average Visa stock forecast suggests 17.4% upside potential.

The Takeaway

In my view, Visa appears well-positioned to continue its momentum for the remainder of 2023 and beyond. With three key factors propelling the company forward — increased spending, a faster pace of capital returns, and a justifiable valuation — Visa could be an appealing investment choice for those seeking to buy a high-caliber company and hold it for the long haul.