Retail stocks have been punished quite severely over the past few weeks. Nonetheless, in this piece, we used TipRanks’ Comparison Tool to have a closer look at three retail stocks that have “Strong Buy” ratings from Wall Street analysts — WMT, HD, and COST.

Undoubtedly, the Federal Reserve is willing to inflict “pain” on the economy as it looks to bring inflation back under control. Chairman Jerome Powell’s comments at Jackson Hole may have induced anxiety in overly-optimistic investors.

Even if rates stay static after inflation is brought back down, the Fed has one extra tool (rate cuts) in its arsenal if the economic picture turns out uglier than expected. In any case, a consumer-spending slowdown and a potential inventory glut seem to be the biggest potential concerns for retail stocks.

Though retail seems like dead money heading into the early innings of a recession, many upbeat analysts may be willing to give them the benefit of the doubt. A lot of recession risk already seems priced in going into September.

Walmart (WMT)

Walmart is an incredibly well-run retailer that’s struggled to hold its own amid inflationary headwinds. The company’s second quarter was technically a beat, with EPS (earnings per share) coming in at $1.77, above the $1.62 consensus. However, the sales mix revealed some troubling trends.

Necessities and food items performed well, while discretionary goods took a hit. Such mix trends are characteristics of an economic slowdown. Excess inventory also paved the way for discounting, acting as a drag on margins.

Undoubtedly, Walmart’s issues are not self-inflicted. Inventory gluts and a waning appetite for discretionary goods and services are expected as we enter the early part of the recession. Fortunately, Walmart has a capable enough management team to sail through the headwinds that should fade in due time.

On the plus side, management stated that it’s gaining share in the grocery market. With a company boasting a reputation for offering some of the best prices, such a trend is encouraging.

The real question is whether Walmart can hang onto its strengthening share in grocery once conditions (inflation and the economy) begin to normalize. If it can, Walmart could rise out of the coming recession stronger than it entered once discretionary demand comes back online.

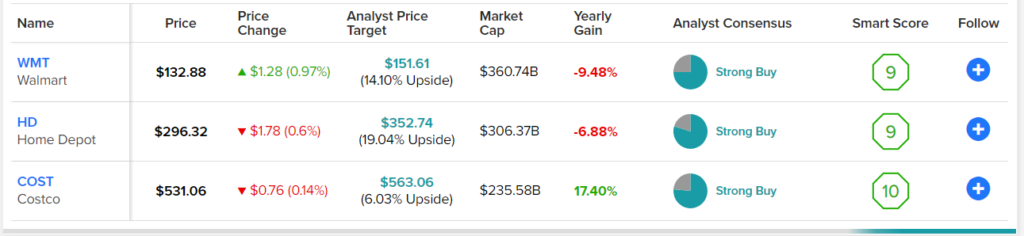

At 26.3x trailing earnings and 0.6x sales, shares of WMT seem richly valued. Still, Wall Street remains upbeat, with 21 Buys, seven Holds, and zero Sells. The average WMT stock price target of $151.61 implies 14.1% upside over the year ahead.

Home Depot (HD)

Home Depot is a home improvement retailer that lost more than 35% of its value from peak to trough. At $296 and change per share, the economically-sensitive retailer seems to be in a strange spot.

Over the long haul, the do-it-yourself (DIY) renovation trend is likely to stay strong. Millennials are starting to buy homes, which will likely accompany many home improvement projects over time. Further, the housing shortage is a strong incentive to spruce up aging houses to get a bit more bang on the market.

In the meantime, a recession or slowdown could cause many homeowners to delay big-ticket projects until there’s more clarity on the macro front. DIY projects do not come cheap, and many of them aren’t time-sensitive.

As demand falls in a recession, expect Home Depot to continue to bolster its distribution network. In due time, demand will return, and Home Depot will need to have the capacity to meet it.

Shares of Home Depot trade at a modest 18x trailing earnings and 2x sales. With a lot of recession risk already factored into the stock, don’t expect analysts to turn their back on the name anytime soon. At the end of the day, Home Depot is a kingpin with a wide moat in the home improvement space. Like Walmart, Home Depot is capable of coming out of a mild recession in a position of power.

Wall Street remains a big fan of HD shares, with 16 Buys and just four Holds. The consensus upside potential is currently set at 19%, with the average HD stock price prediction being $352.74. This number could swell as investors stand firm while shares retreat as a part of the broader market sell-off.

Costco (COST)

Last but not least, we have bulk-buy retailer Costco, which deserves a gold star for its performance through inflationary headwinds. Like Walmart, the Costco brand screams cost savings, and amid the onslaught of high inflation, Costco has found a way to improve its standing among value-conscious consumers.

Not even Costco can save the public from the blow of food and fuel inflation, but it’s been doing a great job of passing on some of the value to its customers. Simply put, Costco can provide deals that many of its rivals can’t match, and that’s a significant reason why store traffic has been heavy as of late.

Costco’s brand loyalty and membership stickiness were strong going into the pandemic. Now that inflation is surging, Costco has been able to take its favorable reputation to another level. Regarding procurement, Costco has a lot of leverage in its favor. It has the warehouse space, the customers, and the stellar management team that knows how to dodge and weave past transitory environmental challenges.

The business of retail remains fierce, especially as inventory gluts become more commonplace. With such high store traffic and huge facilities, I expect Costco is in better shape to make it through inventory markdowns. If anything, further discounting could enhance membership growth.

Costco members are already getting great deals. As the deals get that much greater, I view Costco as a firm that could take some serious share away from some of its smaller rivals.

Finally, Charlie Munger is a huge fan of management and views Costco as a potential digital threat once the firm opts to make a big splash in e-commerce. I’m inclined to agree, though the upside from such initiatives may be years away.

In any case, the stock looks pricy at 41.7x trailing earnings. You’ve got to pay up for quality, though. Wall Street seems to think Costco stock should command a higher premium multiple, with 13 Buys and four Holds. The average COST price forecast calls for a modest 6% in year-ahead upside, however.

Conclusion: Wall Street is Most Bullish on Home Depot Stock

The outlook for retail isn’t too rosy, with inventory markdowns and a potential recession in the cards. In any case, the following three retailers seem more than able to make it through what could be the last storm of headwinds before the next bull run. Of the three names on the list, Home Depot seems to have the most room to run, according to Wall Street.

Personally, I think Walmart is the best Buy of the group for its improving grocery business and its modest multiple relative to Costco.