Competitive gaming, or esports, is a fast-growing subset of the online video gaming industry. Video game popularity, for a long time, was driven by its niche appeal – gamer communities developed, and it seems that every game genre has its own fandom. Fantasy leagues adapted well to online gaming, and the networked systems saw the introduction of massive multi-player role playing games.

Like many online services, there’s a sense that esports came into its own during the recent pandemic crisis. With so many people kept home, esports gave an outlet for both social connections and competitiveness. Esports once was a subset of sporting fans; now it is a vibrant industry that integrates video games into popular culture.

Some numbers will show the extent of the expansion. According to Insider Intelligence, Esports audiences are projected to grow at a 9% compound annual growth rate through 2023, expanding to 646 million. Globally, general awareness of the phenomenon – its overall reach – hit 2 billion in 2020, or nearly 1 in 4 people worldwide. And esports is particularly popular in China, the world’s largest single online market, with 530 million viewers last year.

From a marketing perspective, the key point is that 62% of esports players are between the ages of 16 and 34 (according to GlobalWebIndex) – a key demographic for marketers and advertisers. Strength in this age group underpins the industry’s global value of $947 million last year, and the projections by Newzoo for global esports revenues of $1.08 billion this year.

Such a fast growing sector will usually be packed with solid investment opportunities – and a look at them through the TipRanks platform shows that several leading esports provider companies have plenty to offer investors. These are companies with Buy ratings, and strong upside potential projected for the next year. Here are the details, along with commentary from Wall Street’s analysts.

Huya, Inc. (HUYA)

We’ll start with the Chinese market, where Huya is a major force in the interactive video game segment. The company’s live-streaming platform supports a range of interactive online services, including esports, but also anime, music, reality TV, talent shows, and even outdoor activity programming. Huya boasts that its platform is the #1 live streaming game offering in China.

The company’s numbers back up that boast. Huya saw its total number of playing users grow by 17.6% in 4Q20, compared to the year before. The Monthly Average Users (MAU) was also up, by 18.8% year-over-year, to 178.5 million. And the mobile app for Huya Live saw an even stronger yoy growth in MAU, expanding by 29.1% to reach 79.5 million.

Growth in the user base has translated into growth in revenues, and in Q4 Huya recorded the third consecutive sequential quarterly revenue gain. The top line hit 2.99 billion yuan or more than US$450 million, growing 21.2% year-over-year. The company’s net income rose 58.6% yoy, to reach 253.2 million yuan, or more than US$38 million.

Huya’s gains reflect both the company’s strong product offerings, and its position as a major – and accessible – form of entertainment during the anti-COVID lockdown policies.

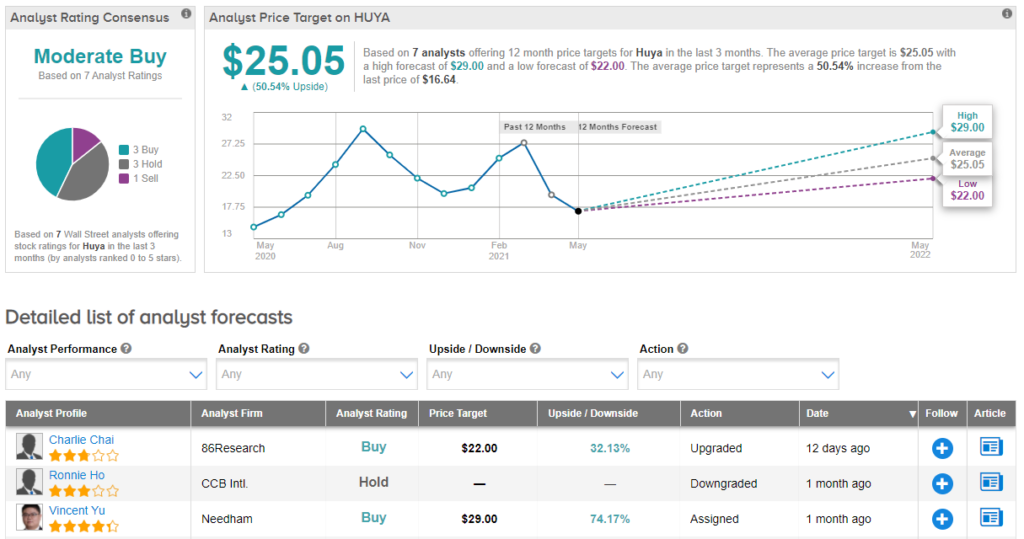

5-star analyst Vincent Yu, of Needham, sees audience growth as a key factor for Huya’s positive forward prospects, and writes, “We believe that the potential end-game size for game-centric live-streaming could be as high as 300 million, assuming a 50% penetration rate among gamers, representing +85% upside from Huya’s 4Q20 MAU…. Huya is expanding its reach to more casual gamers. Additionally, per mgt., the initial impact of video platforms’ entries into game-centric live-streaming, which has been a headwind for Huya in 2020, has largely subsided. Therefore, we believe that Huya will capture market share in an expanding TAM. We are increasing our MAU target by year-end 2021 to 198 million from 193 million.”

Yu gives Huya shares a Buy rating and a $29 price target that implies room for 72% upside in the year ahead. (To watch Yu’s track record, click here.)

This stock has picked up coverage from 7 of Wall Street’s analysts, and their reviews are somewhat mixed, yet the bulls remain in charge. The recommendations include 3 Buys, 3 Holds, and 1 Sell, for an analyst consensus rating of Moderate Buy. The shares are priced at $16.84, and the $25.05 average target suggests an upside of 48% on the one-year time-frame. (See Huya’s stock analysis at TipRanks.)

Esports Entertainment Group (GMBL)

Sports and gambling have a long history, and Esports Entertainment Group takes that online. The company is both an esports and an online gambling provider, connecting sports bettors through online gaming. The company also has traditional sports partnerships with major league teams – from the NFL, NHL, NBA, and FIFA – giving fans new options to connect with their favorite sports.

The Esports Entertainment Group (EEG) has built its business on two important facts: first, that competitive video gaming has a global audience in the hundreds of millions, and second, that wagering on such games, alone or in combination with live sports, reached well over $20 billion last year.

The company is actively expanding its footprint on sports and gambling, and in recent months signed multi-year partnerships with the NFL’s Denver Broncos and Baltimore Ravens as the teams’ exclusive esports tournaments provider. Tournaments will be provided using the Esports Gaming League platform, and the company will have rights to player imagery and a variety of team-related digital media.

In March, Esports Entertainment expanded its footprint in Latin America through two new business partnerships, with Infamous Gaming and Movistar Liga Pro Gaming league. The moves give EEG an additional entry point to the world’s third largest esports regional market. The industry in Latin America is growing at approximately 17% annually.

And, back in February, the company announced both the closing of a public stock offering and its financial results for Q2 of fiscal 2021. In the stock offering, Esports Entertainment put 2 million shares on the market at $15 each, raising $30 million in new capital. In the financial results, Esports Entertainment declared $2.4 million quarterly revenue and raised its fiscal 2021 top-line guidance to $18 million. Revenue guidance for fiscal 2022 is $70 million.

Initiating coverage of GMBL shares at the end of April, H.C. Wainwright’s 5-star analyst Scott Buck wrote, “[The] company currently operates in both esports and online wagering verticals with the goal of providing a platform in which participants can play, watch, and bet on their favorite esports events. The focus on esports is a differentiator and in our view positions the business for substantial growth while being somewhat insulated from the more competitive traditional online sports wagering sites. As the business begins to deliver on its revenue guidance and profitability improves from benefits of scale, we expect new investors to gravitate towards GMBL shares.”

Buck set a $20 price target, implying a 68% upside for the coming year, and a Buy rating on the stock. (To watch Buck’s track record, click here.)

Recently, 4 Wall Street analysts have rated GMBL as a Buy, giving the stock a unanimous Strong Buy consensus rating. The shares are priced at $11.98, and their $22.50 average target suggests robust 88% growth this year. (See Esports Entertainment’s stock analysis at TipRanks.)

Super League Gaming (SLGG)

Last up, Super League Gaming, is both a content platform and an amateur esports provider, creating competitive leagues in the context of digital communities. The company got its start in 2015, and currently offers access to the world’s largest Minecraft server host community, Minehut. Super League’s gaming and content offerings include a dozen top video game titles.

During 2020, the company’s viewership grew by more than 1,500%, reaching 2 billion views of live-stream and on-demand programming. Capitalizing on this growth, Super League in April announced four new business partnerships with over-the-top content distributors. These partnerships will increase the monetization potential of the company’s video content.

In March of this year, Super League raised capital through a sale of stock, putting over 1.5 million shares on the market at $9 each. Gross proceeds, before deducting expenses, reached $13.6 million. The capital raised was marked for sales and marketing activities, along with product development.

In the most recent quarterly report, for the final quarter and full year of 2020, the company reported 90% annual revenue growth, from $1.1 million in 2019 to $2.1 million. The top line growth was supported by expansion of the audience; views and impressions expanded dramatically, hitting 2.03 billion in 2020 from just 120 million 2019. Registered users rose from 1 million to 2.9 million year-over-year. Viewers’ total engagement hours also rose sharply, from 2019’s 15 million to 72 million.

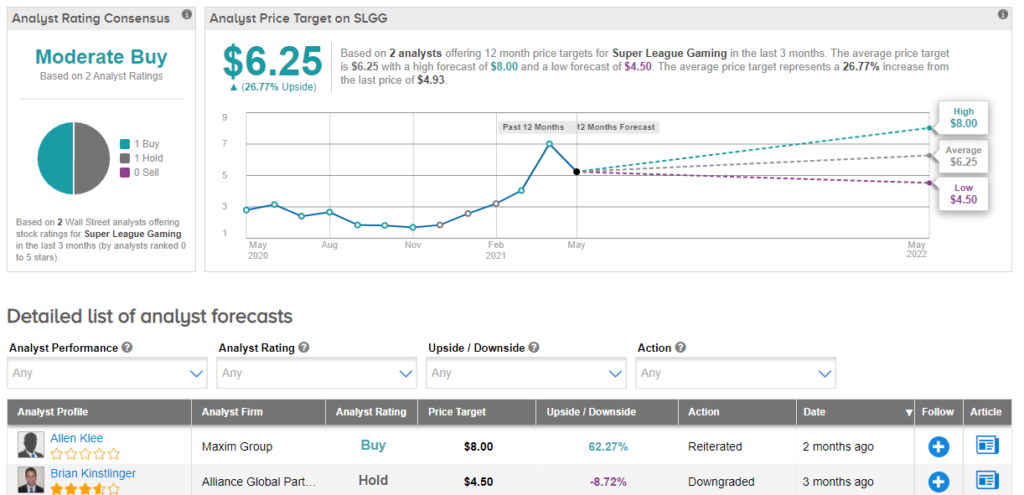

Allen Klee, of Maxim Group, notes that Super League ‘is in the early stage of monetizing its large audience.’ He notes also the size of the company’s potential userbase – and profits: “There is a gaming audience of over 400M on YouTube and Twitch, which is larger than Netflix, Hulu, HBO, and ESPN combined…. There are 2.6B gamers globally according to NewZoo, from which Super League has targeted the competitive amateur players. In terms of potential TAM, if just 10% of gamers participated in an amateur eSports league at $5 per month, it would represent a $15B+ opportunity.”

Klee rates SLGG as a Buy, and his $8 price target indicates a 61% upside potential. (To watch Klee’s track record, click here.)

Overall, SLGG shares have a Moderate Buy consensus rating, based on an even split between the Buys and the Holds. The stock’s average price target of $6.25 suggests an upside of 26% from the current trading price of $4.95. (See Super League’s stock analysis at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.