One thing investors are not lacking for after 2022’s market rout: beaten-down stocks going for cheap compared to levels seen at the start of the year. The problem is how can investors sift through the stock debris to pick out the names which will dust themselves down and push ahead again?

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

As with anything, there are multiple ways to run a stock through the litmus test, but one tried-and-true method is to watch out for the moves the insiders make. These corporate officers know the inner workings of the companies they serve like no one else and when those running the ship load up on shares, it sends a signal they must believe they are undervalued. To keep the playing field level, they must make their purchases (or sells for that matter) public and investors can track the transactions.

The TipRanks Insiders’ Hot Stocks tool provides just such information and we’ve dug up the details on two names which fit a specific profile; down by significant amounts this year but which those in the know have been getting the wallet out for recently, signifying the possibility a bottom might be in sight. Even better, Street analysts also see the pair as good bets; both are rated as Strong Buys by the analyst consensus and projected to deliver strong gains over the coming months. Let see what all the fuss is about.

Insmed Incorporated (INSM)

We’ll start in the biotech sector with Insmed, a company concentrating on the development of treatments for rare diseases.

All biotechs hope to get a drug across the finish line and out to the public and this is a feat already achieved by Insmed. The company’s Arikayce received the FDA’s nod of approval in 2018 and is indicated to treat refractory nontuberculous mycobacteria (NTM) lung disease caused by Mycobacterium avium complex (MAC) infection.

In the recently released Q3 report, Arikayce’s sales increased by 45% year-over-year to reach $67.7 million. This keeps the company on track to meet its 2022 target of at least 30% sales growth.

In contrast to many biotech company, then, Insmed has a reliable revenue generator and that can help with the progress of the pipeline. Drugs currently being developed include brensocatib, which is earmarked as a treatment for patients with bronchiectasis, with enrollment currently taking place for the Phase 3 ASPEN study. Enrollment should be completed in 1Q23, with a topline data readout anticipated in 2Q24.

Brensocatib is also being tested in a Phase 2 pharmacokinetic/pharmacodynamic trial in cystic fibrosis (CF) patients, including both those who are and are not currently taking background CF transmembrane conductance regulator (CFTR) modulator medications. This study is completely enrolled and there should be topline data released for both groups of patients by the end of 2022.

The company is also enrolling for two Phase 2 studies of treprostinil palmitil inhalation powder (TPIP), while there is also a post-marketing confirmatory, frontline clinical trial program of Arikayce in progress (the ARISE and ENCORE trials). Data from the former trial should be put forth throughout 2023.

Despite the sound pipeline, INSM shares are down 34% for the year. Yet, two insiders evidently think the time is right to pounce. This week, director Melvin Sharoky bought 30,000 shares now worth 527,700, while director Leo Lee purchased 45,000 shares worth $791,550.

Stifel’s analyst Stephen Willey is also impressed with INSM’s execution, writing: “Operationally, we believe continued growth of the U.S. Arikayce business remains encouraging – particularly in the context of continued COVID/Fx headwinds in Japan. Clinically, we believe YE22 results from the P2 trial evaluating brensocatib in CF and preliminary 1H23 PRO data from ARISE could prove interesting (NSP inhibition) and important (ENCORE visibility) events, respectively.”

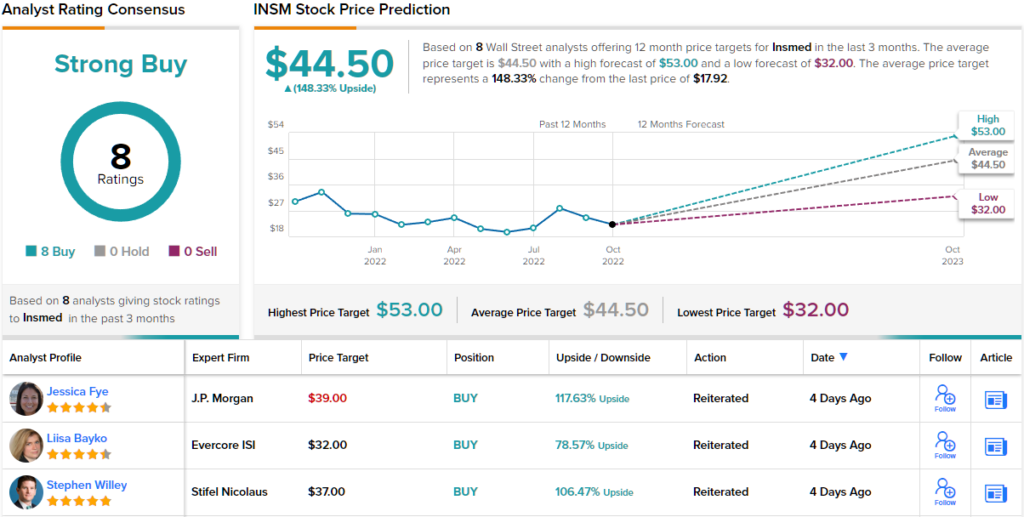

Willey’s confidence is conveyed with a Buy rating and $37 price target, suggesting shares have room for robust growth of 106% in the year ahead. (To watch Willey’s track record, click here)

Willey’s bullish thesis gets the full backing of his colleagues. The stock gets a full house of Buys – 8, in total – which all coalesce to a Strong Buy consensus rating. The average target is even more bullish than Willey will allow; at $44.50, the figure represents upside of ~148% from current levels. (See Insmed stock forecast on TipRanks)

Taysha Gene Therapies (TSHA)

For one biotech to another. Taysha Gene Therapies’ modus operandi is to develop and bring to market a variety of gene therapies to treat monogenic central nervous system (CNS) diseases – both common and rare.

At the forefront of its AAV (adeno-associated virus) gene therapy pipeline, is the most advanced clinical asset, TSHA-120, indicated to treat giant axonal neuropathy (GAN), a rare inherited genetic condition that impacts both the central and peripheral nervous systems.

TSHA-120 has received orphan drug and rare pediatric disease designations from the FDA and data from the phase 1/2 clinical trial showed that individuals with giant axonal neuropathy (GAN) who took the treatment reclaimed sensory nerve amplitudes (SNAPs) whilst also displaying clinical improvement. The company anticipates meeting with the FDA on December 13th for an end-of-Phase 2 Type B meeting in which the regulatory path forward for the drug will be discussed.

The pipeline also boasts TSHA-102, the first-and-only gene therapy being developed to treat Rett syndrome, rare genetic condition that affects the development of the brain. TSHA-102 has obtained orphan drug and rare pediatric disease designations from the FDA and data from the Phase 1/2 study is expected in 1H23.

Drug development is a costly venture and biotechs need money to progress its pipeline. Here, the company had a positive development recently. In October, Taysha announced that Astellas is making a $50 million strategic investment in the company, which gives it a ~15% stake along with the option to secure exclusive licenses for TSHA-102 for Rett syndrome and TSHA-120 for giant axonal neuropathy (GAN).

It’s not the only investment made in recent times. This week, director Paul B Manning loaded up – by buying 1.5 million shares, for a total of $3 million. The purchase comes at a time of a massive pullback for the stock, which is now down 83% on a year-to-date basis.

Looking at Astellas’ investment, and given its track record, Baird analyst Jack Allen thinks it signals some serious intent.

“While we note this deal may ultimately result in Taysha ceding control of its two lead programs, we are quite encouraged by the interest being expressed by Astellas and note that Astellas’ clear interest in the gene therapy space could potentially lead to a takeout offer in the near/medium-term should TSHA-120 and TSHA-102 produce positive updates in 1H23,” Allen opined.

To this end, Allen rates the shares an Outperform (i.e., Buy) while his $21 price target makes room for a whooping 977% in the year ahead. (To watch Allen’s track record, click here)

Think that is some outlandish forecast? Well, other analysts are hardly less enthusiastic. The Street’s average target stands at $20.67, which could generate returns of 960% over the coming months. The ratings are no less effusive; with a unanimous set of 10 Buys, the stock receives a Strong Buy consensus rating. (See TSHA stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.