Earlier this month, the S&P 500 officially entered a bear market; its current year-to-date loss stands at 21%, and the NASDAQ, which has fallen faster and farther, stands at a 30% ytd loss. The rapid reversal not only put the bulls back in the corral, but also erased all of last year’s stock market gains, leading most analysts to start meditating on the prospects of recession. Among the headwinds they’re considering are the highest rates of inflation in over 40 years and in response, a sharp turn by the Federal Reserve toward higher interest rates.

But at least one strategist professes not to worry. Oppenheimer’s John Stoltzfus has staked out a leading place among the bulls, and has for some time now been calling for long-term positive projections. The measure of Stoltzfus’ bullishness? He’s predicting that the S&P 500 hit 5,330 by year’s end. Meeting that mark would mean a jump of some 40% or more from current levels.

Stoltzfus outlines his reasoning on the market’s possible trajectory, saying, “We don’t think there’s going to be a recession, we do think we might skirt it. It’s not an easy time, but we think this Fed is very capable of dealing with it because of experience dealing with the Great Financial Crisis… We’re not out of the woods yet, but we think we’re walking in the right direction and we think the light at the end of the tunnel is not the headlamp of a locomotive but rather it’s sunlight.”

The stock analysts at Oppenheimer have taken these views in stride, and picked out two stocks that they see as potential winners – with potential gains that could vastly outperform even Stoltzfus’ prediction. These picks are penny stocks, the low-cost equities that can be picked up at an ultra-low cost of entry, below $5 per share. At that price, even small changes – just pennies – will rapidly turn into major percentage changes, and the analysts are predicting 300% or better upside on these shares. Using TipRanks’ database, we found out what exactly makes both so compelling even with the risk involved with these plays.

Trevi Therapeutics (TRVI)

The first stock we’ll look at is Trevi Therapeutics, a clinical-stage biopharmaceutical company conducting in-depth investigative trials of nalbuphine ER (branded as Haduvio), for the treatment of chronic neurologically mediated conditions. Specifically, Trevi is studying Haduvio’s effects on chronic skin itches associated with underlying conditions such as prurigo nodularis (PN), as well as chronic coughing caused by idiopathic pulmonary fibrosis (IPF). In short, Trevi is looking to treat some of the quality-of-life symptoms connected with severe, chronic conditions that themselves are treatment-resistant.

The company’s sole drug candidate, Haduvio, is described as an extended release tablet form of nalbuphine, a dual-action opioid derivative, and it is a proprietary product. Clinical data on Haduvio presented in recent months has been generally positive. Trevi achieved a favorable statistically significant efficacy result from the interim analysis in the phase 2 trial (CANAL) of Haduvio in chronic cough associated with IPF, with treated patients demonstrating a 77.3% reduction in cough frequency compared to 25.7% with placebo. The next expected update will be the phase 2b/3 study of Haduvio in severe pruritus associated with PN (PRISM), which is due by the end of June.

Finally, even though Trevi is still pre-revenue, it does have a solid cash foundation. The company has completed a private stock placement in April of this year, which brought in $55 million in gross proceeds.

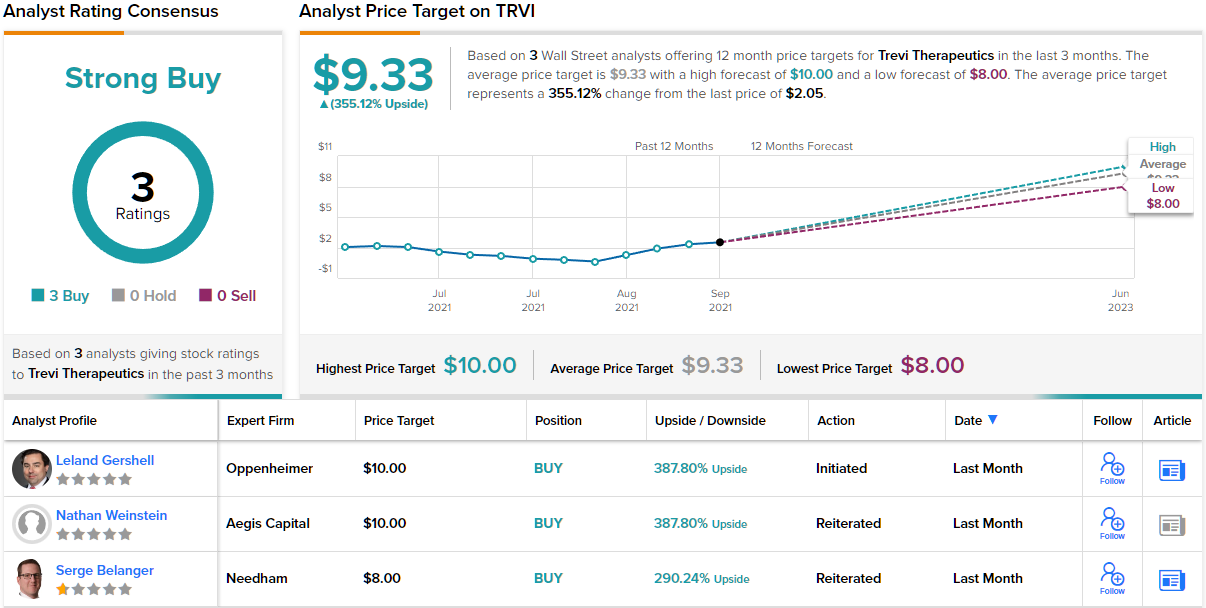

With shares changing hands for $2.05 apiece, Oppenheimer analyst Leland Gershell sees an attractive entry point for investors.

“Following recent positive interim Phase 2 data, we are keen on the prospects of oral candidate Haduvio to address chronic cough associated with idiopathic pulmonary fibrosis —a highly disabling and distressing feature which lacks effective therapy. We also have enthusiasm for Haduvio’s prospects to treat severe chronic itch, an oft-recalcitrant manifestation of a variety of conditions—including prurigo nodularis… We believe Haduvio has $750M+ revenue potential across both opportunities in the US alone… With TRVI trading at an enterprise value of just ~$75M and ample cash resources following a recent financing, we believe continued development progress with Haduvio will support stock outperformance,” Gershell opined.

To this end, Gershell rates TRVI an Outperform (i.e. Buy), and sets a $10 price target to imply a robust 388% upside in the next 12 months. (To watch Gershell’s track record, click here)

All in all, with 3 Buy ratings and no Holds or Sells assigned in the last three months, the word on the Street is that TRVI is a Strong Buy. The $9.33 average price target puts the upside potential at 340%. (See TRVI stock forecast on TipRanks)

Provention Bio (PRVB)

Provention is another clinical-stage biopharma researcher. This one takes an interesting stance on the treatment of autoimmune disorders, aiming to diagnose, catch, and ‘intercept’ these conditions before they can develop into lifelong, chronic illnesses. This necessarily entails work with pediatric patients, as many autoimmune conditions develop in infancy or early childhood. As autoimmune conditions are typically long-term, and frequently have high unmet medical needs, the total addressable market here is substantial.

Provention has an active drug pipeline, with four clinical trial programs, one pre-clinical program, and one drug scheduled for an FDA regulatory decision this coming August. All in all, it’s an impressive lineup, with plenty of catalysts to look forward to in the next 18 months.

The company’s three leading research tracks involve potential treatments for Type 1 diabetes (T1D), the most severe form of the condition, lupus, and celiac disease. Each of these, while not usually terminal, involved long-term quality of life issues. Provention’s leading program, teplizumab, is under investigation as a treatment for diabetes, and the company’s Biologics License Application for the drug was resubmitted for approval last year; the PDUFA date is set for this coming August 17.

On the other upcoming catalysts, Provention still has the PROTECT Phase 3 trial, a study of teplizumab in newly diagnosed T1D patients, ongoing, and expects to release top-line data in 2H23. The PREVAIL-2 Phase 2a trial is studying drug candidate PRV-3279 as a treatment for lupus. This study was initiated in January of this year, and the company is on schedule to release top-line data in 1H24. And finally, the Phase 2b dose-finding placebo-controlled study of PRV-015, a potential treatment for celiac disease, is underway, with a target enrollment of 220 patients. Provention plans on releasing data before the end of next year.

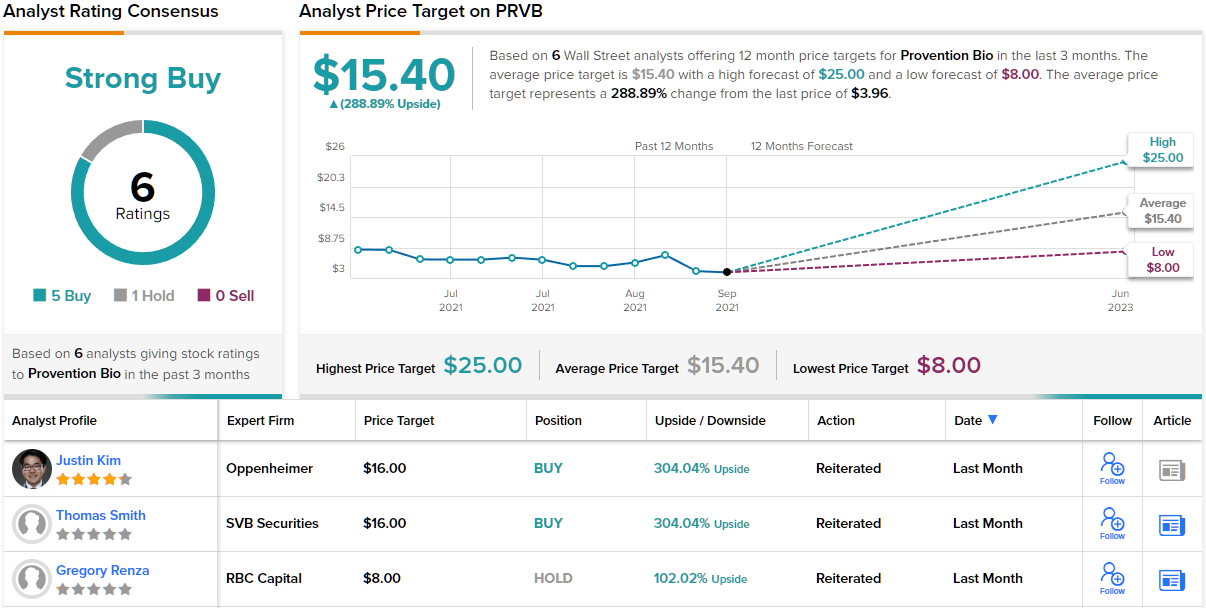

According to Oppenheimer analyst Justin Kim, the potential commercialization of teplizumab will be the main event for this company. He writes, “We hone on three key areas that could be instrumental to a successful launch: patient identification, physician receptiveness, and payor access. In our view, successful execution on these areas could drive a successful commercialization of the product across its initial targeted population of at-risk T1D patients.”

“With the PDUFA several months away, we believe shares could be approaching an inflective turning point… Despite the challenging path traversed prior to the upcoming August 17th’s PDUFA, we believe the magnitude of this catalyst for the shares could become widely in focus and warrant another look for the stock, given the overall evidence supporting the drug’s risk/benefit and potential for PK considerations to have been addressed with the agency,” the analyst added.

With that background, Kim’s Outperform (i.e. Buy) rating on the shares makes sense. His price target, set at $16, suggests a powerful 304% one-year upside potential for the stock. (To watch Kim’s track record, click here)

Overall, Provention has picked up 6 analyst reviews in recent months, and these break down 5 to 1 in favor Buys over Holds, for a Strong Buy consensus rating. The stock current selling price is $3.97, and its $15.40 average price target implies an upside of ~289% lying ahead. (See PRVB stock forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.