Does high risk mean high reward? Not necessarily, so say the pros on Wall Street. Specifically citing penny stocks, or stocks that trade for less than $5 per share, analysts advise caution as these names might still be in the early innings, or it could be that they face an uphill battle that is just too steep.

Luring investors with their bargain price tags, these stocks might be up against overpowering headwinds or have weak fundamentals.

However, analysts argue there are early-stage companies that reflect promising opportunities, with the low share prices meaning you get significantly more bang for your buck. What’s more, even what seems like minor share price appreciation can result in massive percentage gains.

The bottom line? Not all risk is created equal. To this end, the pros recommend doing some due diligence before making an investment decision.

With this in mind, we turned to investment firm Oppenheimer for some inspiration. The firm’s analysts have pinpointed two compelling penny stocks, noting that each could climb over 300% higher in the year ahead. Running the tickers through TipRanks’ database, it’s clear the rest of the Street is in agreement, with each earning a “Strong Buy” consensus rating.

Gamida Cell (GMDA)

The first potentially high-yielding penny stock we’ll look at is Gamida Cell, a clinical-stage biopharma researcher with a focus on cell therapy treatments for severe blood disorders and blood cancers. The company features a proprietary research platform using nicotinamide to expand on various natural cell types, especially natural killer (NK) cells while maintaining their potency. Moving from this platform, the company has developed omidubicel, a new drug under investigation as a treatment for hematological malignancies.

Omidubicel has completed Phase 3 testing in that area – blood cancers – and the company has progressed to the Biologics License Application to the FDA. The next regulatory step is review from the agency, with a PDUFA date of January 30, 2023. According to the company, ‘If approved, omidubicel will be the first allogeneic advanced stem cell therapy donor source for patients with blood cancers in need of a stem cell transplant.’ Gamida also has a Phase 1/2 study ongoing, investigating omidubicel as a treatment for severe aplastic anemia.

Also on the clinical track is Gamida’s second drug candidate, GDA-201. The drug is being evaluated in the treatment of non-Hodgkin Lymphoma. A clinical hold from last fall was removed earlier this year, and Gamida is proceeding with Phase 1/2 clinical trials.

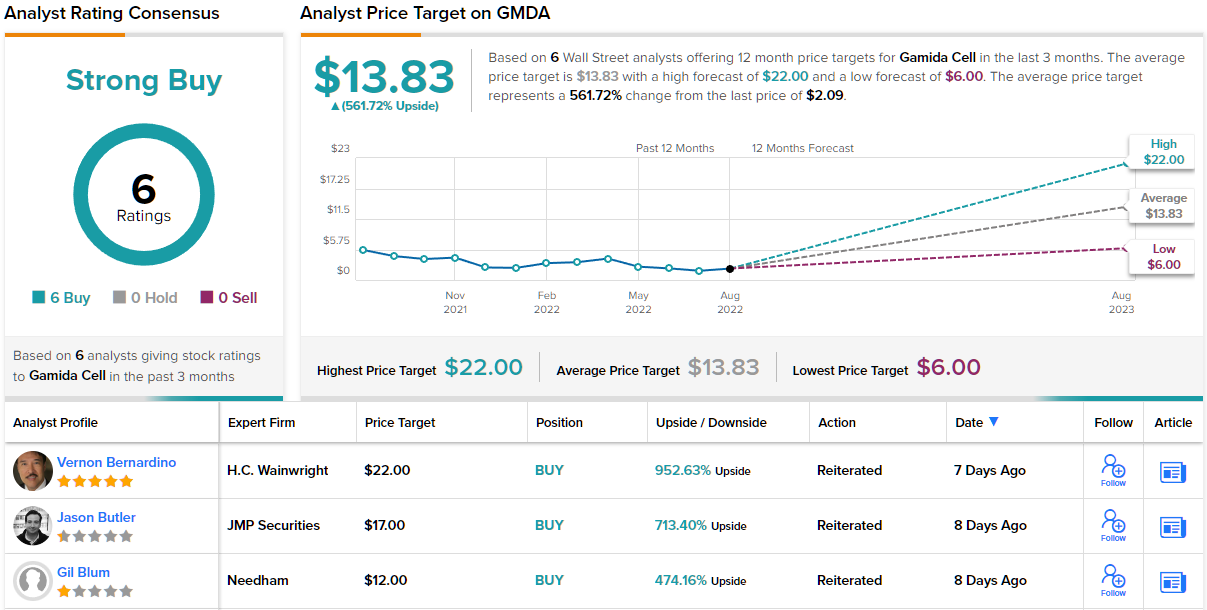

Based on the potential of the company’s drug candidates, and its $2.09 share price, Oppenheimer analyst Mark Breidenbach thinks that now is the time to get in on the action.

Breidenbach sees the likely FDA approval of omidubicel as the main catalyst for this stock, writing: “We remain confident in omidubicel’s regulatory approval based on its strong Phase 3 data… Relative to unmanipulated cord blood, omidubicel demonstrated faster neutrophil engraftment and platelet recovery— translating to significant reductions in serious infections and hospitalization time. We believe omidubicel could represent an attractive new option due to its reliable procurement speed (~30 days) and near-universal HLA compatibility… In preparation for the potential launch, Gamida has engaged with >45 high-volume US transplant centers and has begun to proactively educate payers to help ensure coverage shortly after approval.”

To this end, Breidenbach puts an Outperform (i.e. Buy) rating on Gamida shares, and his $15 price target suggests potential for a whopping 618% upside in the next 12 months. (To watch Breidenbach’s track record, click here)

That may be an extraordinarily high upside potential – but it’s no outlier for this stock. All 5 of the recent analyst reviews here are positive, for a Strong Buy consensus rating, and the $13.83 average price target indicates ~562% upside lies ahead for the stock. (See GMDA stock forecast on TipRanks)

Avalo Therapeutics (AVTX)

The second stock we’re looking at is Avalo Therapeutics, a biopharma firm with a focus on immunological conditions and rare diseases. The company is developing a line of drug candidates with novel mechanisms of action to offer substantial improvements over existing therapies.

Avalo currently has three open research programs undergoing clinical trials. These include AVTX-002, a ‘first-in-class, fully human anti-LIGHT monoclonal antibody’ under investigation for the treatment of inflammatory bowel disease (IBD), non-eosinophilic asthma (NEA), and acute respiratory distress syndrome (ARDS). Other drug candidates in development and trials include AVTX-803 and AVTX-801, which are both monosaccharide therapies for two congenital disorders of glycosylation (CDGs).

AVTX-803 is currently at the most advanced trial stage, with first patient dosed in the Phase 3 LADDER trial just last month. Data from this trial is expected for release in 1H23.

Also of interest in the clinical updates, the Phase 2 PEAK trial of AVTX-002, against NEA, started dosing patients in May of this year. As with LADDER, initial data is expected in the first half of next year.

To boost its cash position, this past July, the company transferred its AVTX-007 program to Apollo Therapeutics Group, granting Apollo a license for commercialization activities. Avalo received $15 million up-front payments, and stands to receive up to $74 million milestone payments going forward, followed by additional royalty payments based on net annual sales.

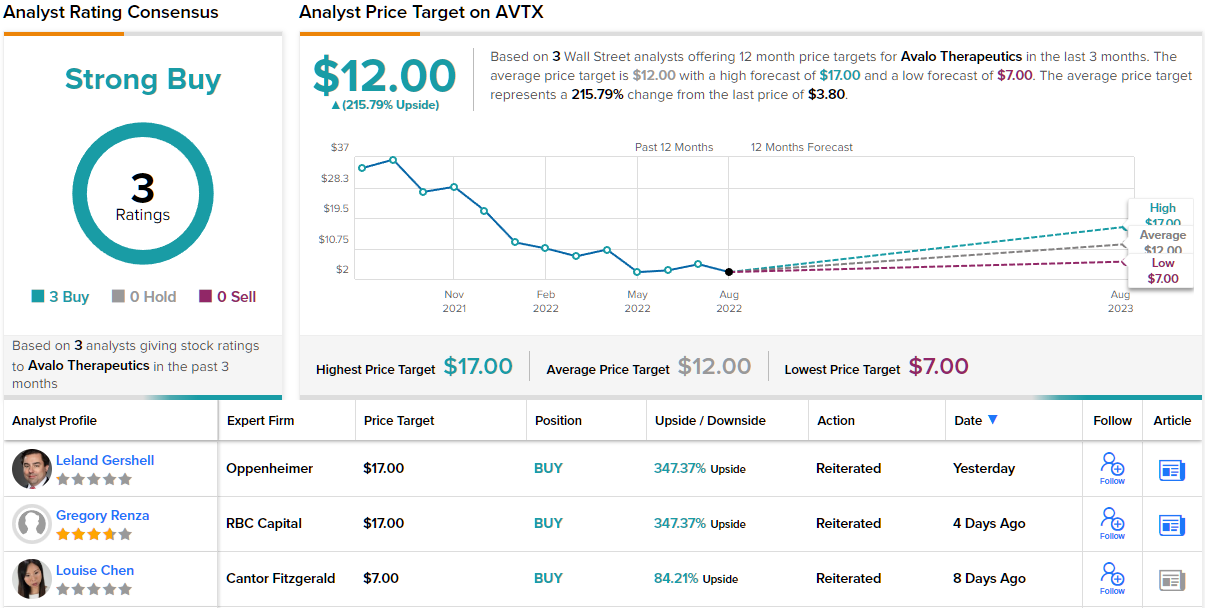

Analyst Leland Gershell, in his coverage for Oppenheimer, wrote: “We see AVTX-002’s opportunity to treat non-eosinophilic asthma (NEA, a significantly unmet subtype that affects ~50% of asthmatics) as the key driver of investor interest…We are encouraged by AVTX-002’s inflammatory activity following impressive observations in moderate-to-severe Crohn’s and in COVID-19 ARDS, and believe non-eosinophilic asthma (NEA) could provide a $1B-plus peak opportunity. Approval of AVTX-803 would be expected to generate a salable Priority Review Voucher worth ~$100M. AVTX’s ~$30M EV suggests shares hold significant upside potential as pipeline progress is registered.”

Gershell’s comments explain his bullish stance, and back up his Outperform (i.e. Buy) rating on the shares. He put a $17 price target on the stock, implying a one-year upside of 347%. (To watch Gershell’s track record, click here.)

Are other analysts in agreement? They are. 3 Buys and no Holds or Sells have been issued in the last three months. So, the message is clear: AVTX is a Strong Buy. Shares in AVTX are selling for $3.80 and the $12 average price target suggests a 12-month gain of ~216% is in store for the stock. (See AVTX stock forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.