What kind of stocks stir up controversy like no other? Penny stocks. These tickers trading for less than $5 per share have earned a reputation as some of the most divisive names on Wall Street, with these plays either met with open arms or given the cold shoulder.

On the positive side, the pennies offer the best cost of entry in the stock market. Anyone who truly believes the adage ‘buy low and sell high’ simply can’t ignore the pennies, because this is where you can buy low. And because the share price is so low, even a small appreciation will very quickly turn into a high-percentage gain on the original investment.

The first drawback should be obvious – the same basic math that magnifies gains here will also magnify losses. In addition, the low cost of penny stocks is often the result of some fundamental weakness in the company.

No matter which side you take, one thing is certain, due diligence is necessary before making any investment decisions. That’s where the experts come in, namely the analysts at Oppenheimer. These pros bring experience and in-depth knowledge to the table.

With this in mind, our focus turned to two penny stocks that have received a thumbs up from Oppenheimer analysts. Running the tickers through TipRanks’ database, both have been cheered by the rest of the Street as well, as they boast a “Strong Buy” analyst consensus. Not to mention massive upside potential is on the table.

Chromadex (CDXC)

Let’s talk about bioscience companies. Usually when you mention this subject, it quickly turns to biopharmaceuticals – and not without reason. But those aren’t the only operators in the bioscience realm. Chromadex is a bioscience research company focused on dietary supplements for healthy aging; specifically, the company is working to develop supplements and food ingredients based on nicotinamide adenine dinucleotide, or NAD, a resource found in all living cells. Research has shown that NAD is vital to numerous biological processes, and can be affected by overeating, over exposure to the sun, and overindulging in alcohol. Chromadex has a flagship product, TRU NIAGEN, that is designed to boost and replenish NAD levels.

Backing its chief product and research approach, Chromadex has 3 safety notifications from the FDA, 11 published human clinical studies, numerous owned patents, and more than 200 research collaborations. The company has adapted TRU NIAGEN into a line of products to meet a variety of consumer needs. Among these adaptations is NIAGEN, a dietary supplement based on nicotinamide riboside, NR, a member of the B3 vitamin family that is used by cells as a precursor to produce NAD.

Chromadex is expanding its product line, and also offers IMMULINA, a spirulina extract containing Braun-type lipoproteins known to have a beneficial effect on the human immune function. Two commonly used supplements, ginseng and echinacea, have these same immune-boosting proteins; IMMULINA offers them at much higher levels.

In recent weeks, Chromadex has released two news items that bode well for the company’s prospects. In early March, Chromadex announced ‘promising findings’ from a peer-reviews published clinical study of the effects of NR as a dietary supplement for Parkinson’s disease patients. The trial was a first-of-its-kind study, and was touted as a milestone in research in both NR and Parkinson’s.

A few weeks after that announcement, Chromadex made public the grant of its latest US continuation patent. This grant, of US patent number 11,272,117, reinforces the previously issued number 11,242,364, and adds to Chromadex’s patent portfolio on NR and related NAD precursor molecules. The company now has over 40 granted patents in this field.

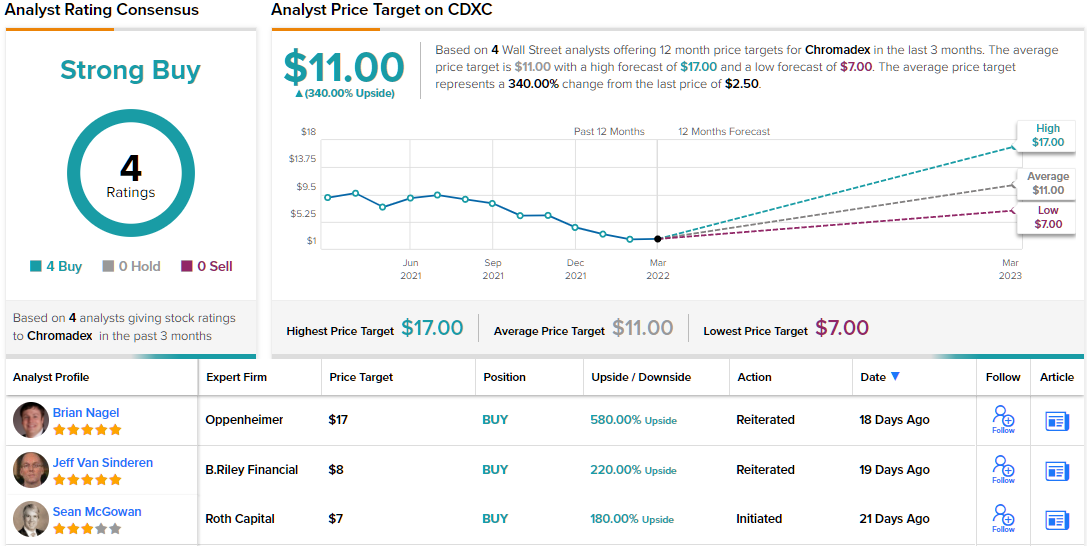

Currently going for $2.50 apiece, Oppenheimer believes CDXC’s long-term growth narrative is strong. Brian Nagel, one of the firm’s 5-star analyst, writes of this company: “As we examine closely recent trends at the company, we very much come away with a sense of ‘more of the same.’ In our view, Tru Niagen represents an extremely well-studied and truly revolutionary health supplement. We continue to applaud senior leadership of CDXC for pushing the science behind CDXC so effectively. For us, the significant ‘unlock’ for Tru Niagen and CDXC remains a much more aggressive marketing campaign, which leverages an increasingly well-built-out distribution infrastructure and much better introduces the supplement to target and more mass-market consumers.”

To this end, Nagel rates CDXC an Outperform (i.e. Buy), and his $17 price target suggests a massive upside of 580% in the year ahead. (To watch Nagel’s track record, click here)

Overall, this penny stock has a unanimous Strong Buy consensus rating, with 4 positive analyst reviews. Given the $11 average price target, shares could soar 340% from current levels. (See CDXC stock forecast on TipRanks)

BioVie (BIVI)

Now let’s move over to the biopharma research field, where BioVie is working on new drug therapies for a variety of conditions, including Alzheimer’s and the liver cirrhosis complication ascites. The company has two main drug candidates, NE3107 and BIV201, each with multiple indications.

On the clinical track, BioVie has several studies underway of particular notice to investors. First is a Phase 3 trial involving NE3107 as applied to the treatment of Alzheimer’s. NE3107 has shown to have anti-inflammatory effects, and this pivotal Phase 3 trial will evaluate the drug’s efficacy against the neuroinflammation that is symptomatic of the degenerative disease. Topline results are expected by this year’s end.

Also of interest for the potential of NE3107, the company announced in January that it begun treatment of the first patient in its Phase 2 study of the drug candidate in combination with carbidopa or levodopa. The trial, a double-blind, placebo-controlled, safety, tolerability, and pharmacokinetics study of NE3107 and its pro-motoric effects, is expected to show initial data by the middle of this year.

Finally, BioVie has a Phase 2b trial underway of BIV201 in the treatment of ascites, a fluid-retention symptom of liver cirrhosis. The company has a target enrollment of 30 patients, and expects to release topline results this year. A Phase 3 trial is in the planning stages, for a quick follow-up should results so warrant.

Analyst Jay Olson, in his note for Oppenheimer on this stock, writes, “We view the safety/tolerability profile of NE3107 as favorable with low potential for DDI and no immunosuppression, which supports use as chronic therapy for AD and PD… We forecast peak sales for NE3107 of ~$1.3B for AD and ~$0.4B for PD in 2031, and apply our respective 50% and 20% POS estimates… Our SOTP analysis values NE3107 in AD at $8/share and PD at $1/share. We view BIVI as undervalued ahead of key catalysts and consider other programs… as ‘free’ call options.”

In line with these upbeat comments, Olson rates the stock an Outperform (i.e. Buy). His price target, at $9, implies a strong 12-month upside of ~114%. (To watch Olson’s track record, click here)

While BIVI only has 3 recent analyst reviews, they are all positive – for a Strong Buy consensus rating. The stock has an average price target of $11.50, indicating a robust 173% one-year upside from the current trading price of $4.20. (See BIVI stock forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.