Last week Micron (MU) held its investor day and breaking tradition with previous years, the company provided a long-term financial outlook. The memory giant expects revenue growth in the high-single digits, EBITDA margins to reach low 50s% and FCF% of more than 10%.

The company forecast that by 2030 the memory and storage market will more than double from ~$161 billion in 2021 to $330 billion. This includes anticipated high teens growth for DRAM and growth in the high 20’s percent for NAND.

The anticipated revenue growth reflects a period in which industry profitability is on the rise, with GMs of 20% during 2006 to 2013 climbing to 40% between 2014 to 2021. This is also throughout cycles in which industry wafer fab equipment expenditure as a percentage of EBITDA has dropped from 57 percent in 2011 to 30 percent in 2021.

With the industry anticipating cycles to be less pronounced, the company said its longer-term strategy involves forward pricing agreements – the first fruit of which is a 3-year agreement with a top 10 customer worth ~$500 million per year. The guaranteed supply of such a deal should be of benefit to both the company and its customers.

“This LTA item,” says Rosneblatt analyst Hans Mosesmann, “will spark Street debate on how you actually enforce the agreement in a down cycle, and it wouldn’t be a big deal for years to come. However, the fact that they landed a big customer is intriguing, and we bet this customer sees a need to engage more strategically in a market that is likely to be supply constrained in our opinion.”

Meanwhile, Micron continues to return capital to shareholders; The company increased its quarterly dividend by 15% to 11.5 cents per share, and said it is continuing to repurchase shares aggressively, with $700 million planned for the present quarter, which runs until the end of May. Micron has around $5 billion left on its current stock repurchase authorization and anticipates keeping on buying at current levels.

Mosesmann praises the latest developments and remains the Street’s most prominent bull.

“Micron’s investor day was impressive and the first one in our over 20 years of coverage that the company aligned leadership in all areas including execution, extending leadership in DRAM and NAND, operations, and financial,” the 5-star analyst said. “We see the risk/reward at current level as very favorable for investors particularly given Micron’s replacement value of assets alone of $100 billion handily exceeding the company’s market cap of $74 billion.”

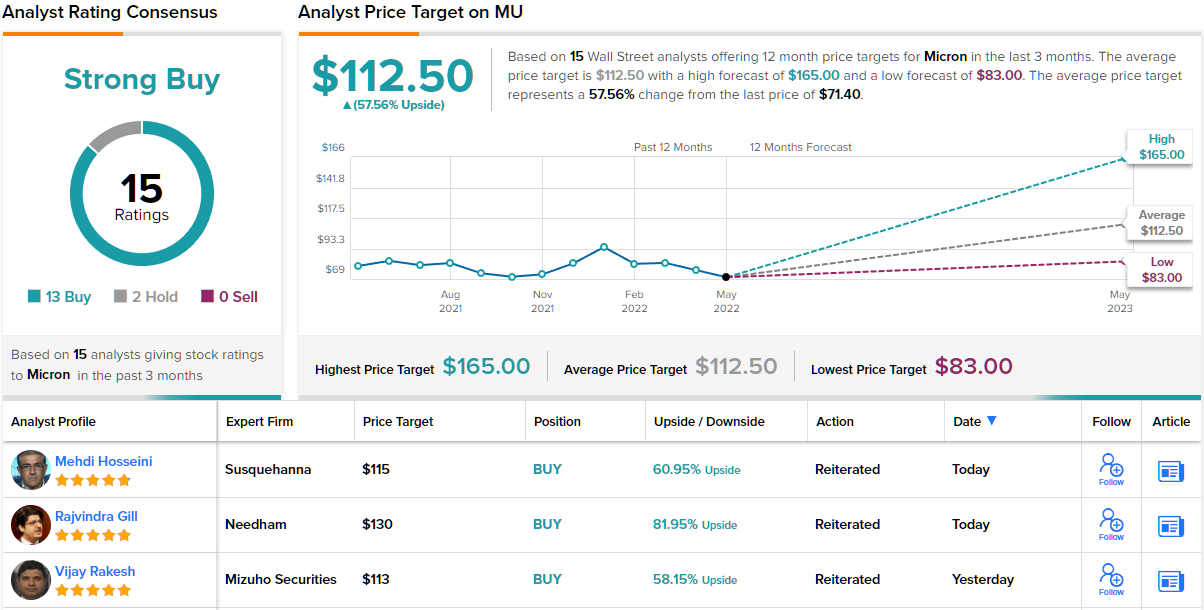

Accordingly, Mosesmann rates Micron shares a Buy along with a Street-high price target of $165. If correct, the analyst’s objective could deliver one-year returns of ~131%. (To watch Mosesmann’s track record, click here)

What do other analysts have to say? 13 Buys and just 2 Holds add up to a Strong Buy analyst consensus. Given the $112.50 average price target, shares could climb ~58% from current levels. (See Micron stock forecast on TipRanks)

To find good ideas for chip stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.