Those hoping for the fourth quarter to herald a stock market comeback have been disappointed so far. A late-year rally has yet to properly materialize with the market still factoring further turmoil as the fight against inflation continues and the specter of a recession remains.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

However, while the prospect of a recession looms, Morgan Stanley’s Investment Management Managing Director Andrew Slimmon points out that many stocks already appear to be taking for granted the likelihood of a recession.

“I can’t imagine that the tightening that the Fed’s done and will continue to do will not affect the stock market at some point… But the key point, and maybe this is where stock picking can add a lot of alpha, is there are so many stocks down 40%, 50%, 60% that they’re already reflecting a recession,” Slimmon said.

Slimmon does not see “tremendous downside” for most stocks from here, so maybe it’s time to look at some of these downtrodden names.

Morgan Stanley analysts have homed in on two such stocks which are down at least 40% this year, but which they believe are primed for a turnaround. We’ve used the TipRanks database to get a feel for the rest of the Street’s take on these names. Let’s take a closer look.

Smartsheet Inc. (SMAR)

Online workplace collaboration is big business these days with many companies offering software services to bring about a more convenient working environment. One such name catering to these needs is Smartsheet. The company is a leader in the competitive Project Portfolio Management (PPM) software segment. The company offers a platform which is used for assigning tasks, following a project’s progress, managing calendars and the sharing of documents with the product’s ease of use making for more effective workflow management.

A glance at the growing revenue haul indicates that companies using the service agree; sales have been steadily increasing over the past couple of years, a trend which continued in the financial results for the second fiscal quarter (July quarter). Revenue increased by 41.7% year-over-year to $186.7 million, beating the consensus estimate by $6.14 million. The company posted a beat on the bottom-line too, with adj. EPS of -$0.10 faring much better than the -$0.20 anticipated by the analysts.

Even so, the company’s stock price has fallen dramatically, by 56% year-to-date. For Morgan Stanley’s Josh Baer, however, investors should take note of this stock’s “underpriced secular growth.”

“Smartsheet is a high quality asset in the collaboration software space, with the most robust Enterprise features and the broadest product portfolio equipped to handle the widest array of use cases compared to workplace collaboration peers,” Baer said. “We see Smartsheet going after a large $21B total addressable market as its platform addresses a growing number of use cases. With >100K customers of all sizes, Smartsheet has seen viral adoption within its customer base, as highlighted by a best-in-class 120%+ net retention rate. Given the company’s low market penetration and a strong competitive moat, we see sustainable >20% rev CAGR over the next 10 years.”

Accordingly, Baer rates SMAR shares an Overweight (i.e., Buy) while his $54 price target suggests the shares are undervalued to the tune of 70%. (To watch Baer’s track record, click here)

Most agree with Baer’s thesis; SMAR’s Strong Buy consensus rating is based on 15 Buys vs. 3 Holds. At $45.24, the average target implies one-year share appreciation of 42%. (See SMAR stock forecast on TipRanks)

Ford (F)

The next beaten-down name we’ll look at needs no introduction, but let’s do it anyway. Auto giant Ford is a household name and one of the world’s most recognizable brands. Millions have ownership of a Ford, be it a truck, car, SUV and more recently EVs (electric vehicles).

Indeed, it’s all been change in the auto industry with the rise of the electric vehicle and Ford is wary of being left behind. The company is increasingly leaning into the EV opportunity and currently offers the Ford F-150 Lightning pickup, the Mustang Mach-E crossover and the e-Transit van. More EVs are anticipated to be added in the years ahead with the company pledging to invest up to $50 billion by 2026 on its electrification endeavors.

As part of its reorganization plan, Ford is also splitting the business into three segments of commercial, electric, and internal-combustion offerings.

However, these plans cannot paper over the problems currently faced by an industry rocked by supply chain woes, a shortage of parts and higher inflation-related supplier costs.

While Ford delivered beats on both the top-and bottom-line when it reported Q2 earnings in July, in a recent update the company said Q3 EBIT will come in the $1.4 billion to $1.7 billion range, far below consensus at $3 billion.

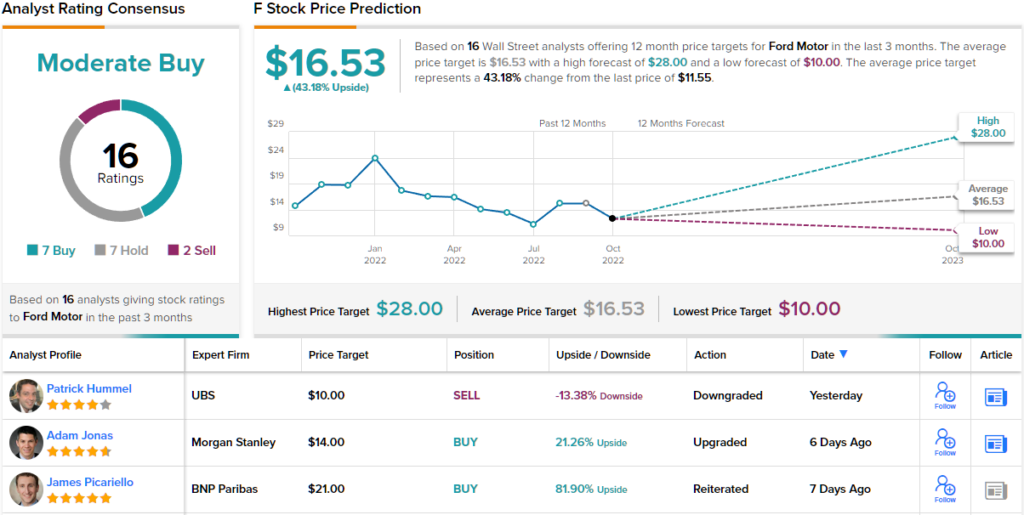

As Morgan Stanley’s Adam Jonas notes, “3Q profits warning coupled with macro concerns have resulted in a decline in buy-side expectations and sharp pull-back in shares.” On a year-to-date basis, the stock is down 43%.

However, Jonas believes current share price makes Ford attractive on valuation basis, and lays out why: “We estimate Ford cash flows through FY30 may far exceed 100% of the company’s current enterprise value. Our preference for Ford is very much tied to our confidence in management’s strategy to re-architect the business portfolio following its sweeping re-organization.”

To this end, Jonas rates Ford shares an Overweight (i.e. Buy) backed by a $14 price target, signifying potential for 12-month returns of 21%. (To watch Jonas’s track record, click here)

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. 7 Buys and Holds, each, and 2 Sells add up to a Moderate Buy consensus rating. The average target is an upbeat one; at $16.53, the figure suggests shares will climb 43% over the coming months. (See Ford stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.