Our digital world is changing – 5G is on the way, and it will transform the way we use mobile networks. Higher speeds and lower latency will allow for more versatile web use and communication networking via smartphones and tablets, and as the new networks increase their reach, they’ll accelerate the trend towards smaller, more mobile devices.

The advantages of 5G won’t end with better handheld devices. Self-driving cars are becoming reality – and it’s because of the higher capacity networks, capable of handling the real-time data streaming that an automotive AI will require. And Internet of Things, which is already changing manufacturing, will truly come into its own due to 5G tech. We are on the cusp of a technological revolution, and with it comes a slew of investment opportunities.

Network providers, semiconductor chip makers, and software companies are among those that stand to benefit from 5G. We’ve used the TipRanks database to pinpoint three names poised to gain as 5G expands – and each is already taking steps to ensure that they do.

America Movil (AMX)

The largest telecom company in Latin America, and the fourth-largest in the world, America Movil boasts a $53.7 billion market cap even after the heavy share depreciation due to the coronavirus crisis in 1H20. The first half, especially the first quarter, saw sharp reductions in revenues and earnings, but the company’s niche is solid, and through its subsidiaries, the company controls the lion’s share of Latin America’s wireless service.

A look at the Mexican wifi spectrum will illustrate the point. AMX is the owner of Telcel, Mexico’s largest wireless telecom provider. In the past 12 months, Telcel received two major transfers of wireless spectrum rights, each totaling 50 MHz, in the critical frequencies for 5G networking. Through Telcel, AMX now controls at least 100 MHz in the 3.5 GHz bandwidth in the Mexican market – and more importantly, will not need to participate in bandwidth auctions to expand 5G services.

Scotiabank analyst Andres Coello, one of AMX’s biggest bulls, noted: “The amount paid by Telcel is a bargain when considering Mexico is a USMCA country with ~130 million people and is the second-richest nation in LatAm. In the US, a similar amount of spectrum in the same frequencies is estimated to be worth up to 15x more (US$1.3B). More importantly, the spectrum positions Telcel ahead of everyone else in 5G, but particularly against the wholesale network, which owns spectrum exclusively in the 700 MHz band. We estimate there are 11M homes in Mexico lacking access to fixed infrastructure. Similar 5G solutions as those launched by AMX in Austria could help the company monetize this opportunity while taking share from cable incumbents as download speeds reach up to 500 Mbps.”

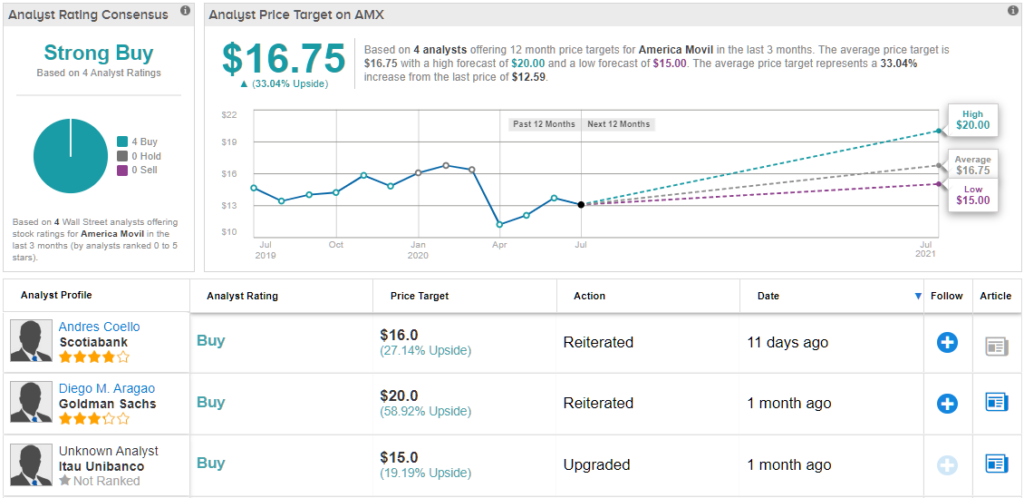

Keeping in mind AMX’s strong position for growth in the Mexican market, Coello gives the stock a Buy rating with a $16 price target. His target shows his confidence; it implies a 27% one-year upside potential for the stock. (To watch Coello’s track record, click here)

Coello’s bullish stance is in line with Wall Street’s collective wisdom. The analyst consensus rating on AMX is a Strong Buy, based on a unanimous 5 Buys set in recent weeks. The stock’s average price target is $16.75, indicating a 35% upside potential for the coming year. (See AMX stock analysis on TipRanks)

Digital Turbine, Inc. (APPS)

Digital Turbine’s apps make content discovery and delivery simple, allowing mobile operators to accurately target content – and revenue-generating ads – directly to the users. The company’s platform has a record of repeated success: 3 billion app preloads on 400 million devices in tens of thousands of advertising campaigns.

With 5G promising faster connections and lower latency, users are going to become less patient when looking for content – and a platform that delivers the right content, without delay, is positioned to gain. That’s where Digital Turbine finds itself. Its platform connects apps and advertisers, and that is a benefit that cannot be measured in just dollars.

Analyst Anthony Stoss, of Craig-Hallum believes “APPS is a hidden 5G play positioned for double digit growth over the next several years… With the 5G cycle now in the starting phases we look for carriers and OEMs to begin to aggressively promote 5G devices… With smartphone units likely to grow year-over-year in 2021, we think APPS has the potential for significant growth and consider our current estimates conservative.”

In line with his view of the stock in the early phase of take-off, Stoss puts a Buy rating on APPS along with a $15 price target. This would suggest a 13% upside potential for APPS this year. (To watch Stoss’ track record, click here)

The analyst consensus rating on APPS is a Strong Buy, based on 6 reviews that include 5 Buys and 1 Hold. The stock’s recent appreciation has pushed it above the average price target; expect Wall Street analysts to adjust their views in coming weeks. The shares currently sell for $13.22. (See Digital Turbine stock analysis on TipRanks)

Qualcomm, Inc. (QCOM)

Qualcomm is heavily invested in 5G, and its chips are used in wireless modems, IoT, and AI applications that all require access to the new digital spectrum and networks. A strong line-up of 5G products underlay Qualcomm’s fiscal Q2 earnings and revenue beat, which in turn has helped support the rising share values. The stock has recovered from its depreciation during the February/March market crash, and is now trading above its February peak.

Michael Walkley, 5-star analyst with Canaccord, sees a bright future for Qualcomm. He writes: “With smartphone volumes starting to recover and expected to improve in 2H/C20, Qualcomm is well-positioned to benefit from the long-term 5G investment cycle… we believe Qualcomm will sustain its current licensing business and this high-margin business should benefit from 5G smartphone growth trends… We believe Qualcomm has a strong leadership position for 5G…”

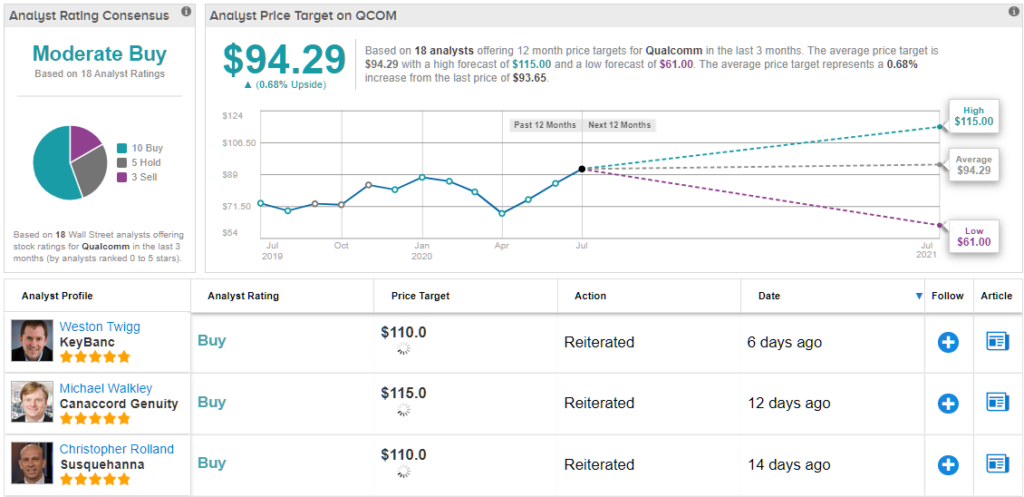

Walkley’s boosted price target of $115, up from $102, fully supports his Buy rating on the stock, suggesting it has a 24% upside potential for the coming 12 months. (To watch Walkley’s track record, click here)

Qualcomm’s recent share gains have pushed the trading price close to the average price target. The stock is selling for $93.69, while the average price target stands at $94.29. The stock has a Moderate Buy from the analyst consensus, based on 18 reviews, including 10 Buys, 5 Holds, and 3 Sells. (See Qualcomm stock analysis on TipRanks)

To find good ideas for 5G stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.