A few years ago, telehealth services were in a nascent stage, but in 2022, the industry is vibrant and growing, thanks largely to the pandemic. In this piece, we used TipRanks’ Comparison Tool to evaluate two telehealth stocks — TDOC and DOCS. Doximity (NYSE: DOCS) is highly profitable, while Teladoc (NYSE: TDOC) has never been profitable on a GAAP basis. As a result, a bullish view seems appropriate for Doximity in light of this year’s sell-off, while Teladoc seems more deserving of a bearish-to-neutral view.

Rapid Growth in the Telehealth Industry

During the COVID-19 pandemic, telehealth took center stage in the healthcare sector, enabling patients to continue seeing their doctors without running the risk of spreading the virus. However, like many other trends that exploded during the pandemic, telehealth continues to display robust growth.

According to the Department of Health and Human Services, the number of medical appointments for Medicare patients done via telehealth services skyrocketed from 840,000 in 2019 to 52.7 million in 2020.

Depending on the source, the telehealth industry was worth $144.4 billion in 2020 or $62.4 billion in 2021, although both sources suggest a compound annual growth rate in excess of 30% through 2028. Either way, telehealth looks primed for rapid growth in the coming years.

Of course, a key question now is where telehealth will settle after the spike in usage driven by need during the pandemic. McKinsey boldly estimated during the pandemic that up to $250 billion worth of healthcare in the U.S. could be shifted to telehealth services.

Today, McKinsey states that two-thirds of the office visits and outpatient care it had forecasted would be shifted online are now being delivered via telehealth. The firm also reports that telehealth usage has stabilized at 38x higher than before the pandemic, or between 13% and 17% of all medical appointments across all specialties. With relatively few companies in the space, it would seem that the market is now up for grabs.

Teladoc (TDOC)

Teladoc is perhaps the best-known name in the telehealth space, but unfortunately, the company has never been profitable. As a result, a bearish view may be appropriate in the near term and a neutral view in the long term for investors insistent on a wait-and-see approach in case the company ever becomes profitable.

Teladoc shares are down more than 70% year-to-date, including 10% over the last five trading sessions. The company reported a net loss of $3.1 billion for the June 2022 quarter, a significant increase from the $133.8 million in net losses recorded in the year-ago quarter.

The increase was largely due to a $3 billion non-cash goodwill impairment charge recorded in the quarter, which management said on the earnings call was due to the company’s plummeting stock price, among other factors.

Digging deeper into Teladoc’s earnings numbers reveals some causes for concern. The company said its revenue rose 18% year-over-year to $592.4 million in the June 2022 quarter. Its average revenue per paid member in the U.S. rose to $2.60 from $2.31 in the year-ago quarter. With 56.6 million paid members, it’s worth asking why Teladoc isn’t bringing in more revenue.

Additionally, Teladoc’s adjusted EBITDA is plunging, falling 30% year-over-year to $46.7 million in the second quarter. With management often changing its guidance and then failing to meet that reduced guidance, Wall Street has punished the company repeatedly.

Speaking of punishment, the Street has been uninterested in funding unprofitable tech companies this year, another reason why things just don’t look good for Teladoc stock right now. At some point, this company may finally demonstrate that its business model and strategy work, but we’re not there yet.

What is the Price Target for TDOC stock?

Teladoc has a Hold consensus rating based on five Buys, 17 Holds, and one Sell rating assigned over the last three months. At $37.89, the average Teladoc price target implies upside potential of 42.3%.

Doximity (DOCS)

Doximity has been punished this year as well, although not as severely as Teladoc, and for good reason. Doximity shares are off 40% year-to-date, including about 10% over the last month. The company’s strong business model and operating metrics make a bullish opinion seem appropriate right now, particularly in light of the sell-off in its shares.

Unlike Teladoc, Doximity has been profitable for years, recording operating margins of 33% for 2021 and 30.5% for the last 12 months. The company is also growing, having reported $90.6 million in revenue for the most recently completed quarter, a 25% year-over-year increase.

Adjusted EBITDA rose 8% to $33.5 million for an adjusted EBITDA margin of 37%, which declined from 43% a year ago. Unfortunately, Doximity management also slashed their revenue guidance for the year to between $424 million and $432 million from between $454 million and $458 million. The lower guidance suggests a significant slowdown in growth, and the Street wasn’t happy about it.

On their latest earnings call, Doximity management explained why they slashed their guidance, tying it to a slowdown in their “historically stable upsell rate” among their pharmaceutical clients. They said macroeconomic headwinds are pressuring pharmaceutical companies, but they see these issues as only temporary.

Despite this slowdown, Doximity appears to have a bright future, and this year’s steep sell-off could present an attractive entry point for investors. The company’s P/E has plummeted to around 43x, down from its peak of around 291x in September 2021.

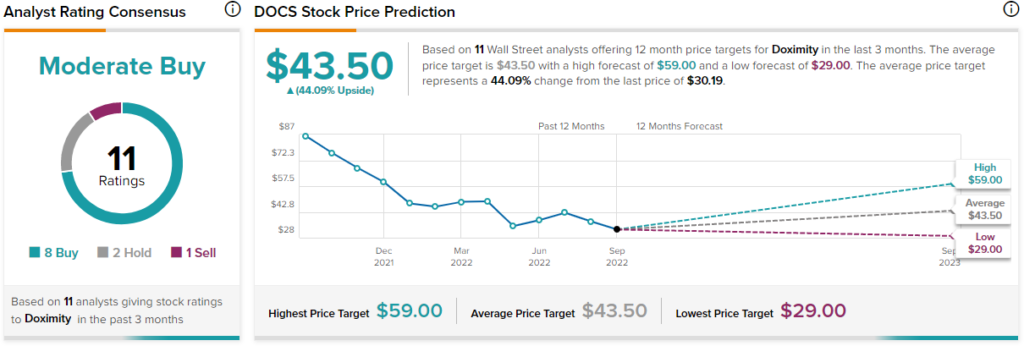

What is the Price Target for DOCS Stock?

Doximity has a Moderate Buy consensus rating based on eight Buy ratings, two Hold ratings, and one Sell rating over the last three months. At $43.50, the average Doximity price target implies upside potential of 44.1%.

Conclusion: Bullish on DOCS, Bearish on TDOC

A review of Doximity’s and Teladoc’s fundamentals reveals why a bullish view is appropriate for Doximity and why a bearish near-term view is warranted for Teladoc. Wall Street is quite unhappy with money-losing companies right now, but the sell-off in Doximity shares could present an attractive entry point.

It’s important to note that Doximity differs from Teladoc in that it’s like a LinkedIn for doctors — with a telehealth platform added on. On the other hand, Teladoc is primarily a telehealth platform. As a social network for doctors, Doximity has a stronger business model than Teladoc.

We know from Meta Platforms’ (NASDAQ: META) massive revenue growth over the years that social networking can be a highly-profitable business. Additionally, Doximity is offering adjacent services like telehealth that serve to diversify its revenue streams.

Given the robust growth of telehealth services, the industry is a good one to be in — despite Teladoc’s repeated failures to generate profits. As a result, Teladoc’s fundamentals may look healthy eventually, but at this point, there just isn’t much to like.