Corporate insiders give us one of the clearer signals available in the stock markets. The insiders are company officers, with ‘inside’ positions that give them greater access to company plans and resources, the very facts that will impact stock prices.

Governmental regulators require insiders to publish their trades in a timely manner, as a way of avoiding their having an undue advantage, and retail investors can use tools like the Insiders’ Hot Stocks to follow these trades.

We’ve gotten the process started, using the tool to pull up the latest data on three stocks that insiders have been scooping up. The buys are notable for their magnitude – these insiders are laying out six figures or more on their own firms’ shares, and that’s not a move taken lightly. All three are also considered Moderate or Strong Buys by the consensus of the Wall Street analysts, and are projected to pick up steam in the months ahead.

Applied Blockchain (APLD)

Applied Blockchain, as its name suggests, is heavily involved in the bitcoin mining segment; in fact, the company builds and operates the next-gen data centers that power the North American bitcoin mining industry.

In the first half of this year, Applied Blockchain has made some important moves to increase its footprint in the industry. In January, the company announced a partnership with Antpool Capital Asset, a provider of blockchain mining solutions, that will allow the two signatories to pool resources in the development of 1.5 gigawatts worth of new datacenter hosting capacity by the end of 2023. And in May of this year, Applied Blockchain held the formal opening ceremonies of its 100 megawatt facility in Jamestown, North Dakota. The facility is currently operating at 83 megawatts capacity, and is scheduled to fill out the remainder of its capabilities by the end of this calendar year.

Blockchain data centers, bitcoin mining, and their power requirements don’t come cheap, and Applied Blockchain raised capital in April of this year through its IPO. The company originally filed for a $60 million public offering; in the event, which saw the APLD ticker debut on the NASDAQ on April 13, the company put 8 million shares on the market for $5 each, raising $40 million in gross proceeds and realizing $36.1 million after deducting the underwriters’ costs.

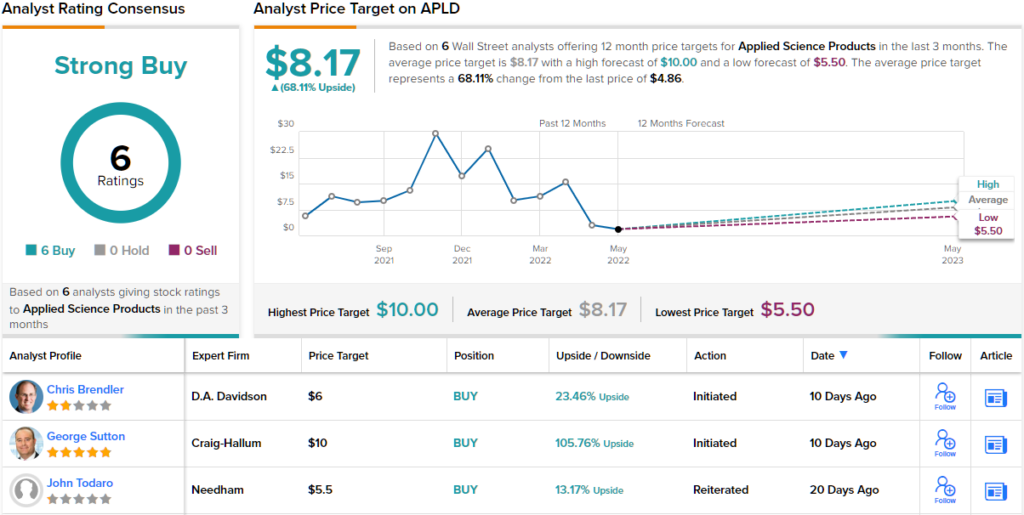

In the last two weeks of May, Applied Blockchain saw a series of major insider buys from company CEO and Chairman Wes Cummins. Cummins’ purchases totaled over 770K shares, and he paid out more than $2.43 million on the buys.

Craig-Hallum’s 5-star analyst George Sutton is also a fan of Applied Blockchain. He writes, “We believe APLD represents an opportunity to invest in Bitcoin Network growth with fiat economics in a structure which will likely favor returning capital to shareholders in a REIT structure in the long-term.”

“Based on our estimates, 1.5 GW would translate to $830M in revenues and an EBITDA margin that should start in the low 30s and then steadily grow towards 40% as APLD continues to scale its operations. For each 100 MW of hosting, APLD should earn site level EBITDA of ~$12M, which should scale towards $20M over time, and a payback period of < 3 years,” Sutton added.

In line with these comments, Sutton rates APLD stock a Buy, and his $10 price target indicates potential for ~106% upside in the year ahead. (To watch Sutton’s track record, click here)

The unanimous Strong Buy consensus rating, based on 6 analyst reviews just since the IPO, shows that Wall Street has noticed this company – and agrees with the bulls. The stock is selling for $4.86, and its $8.17 average price target suggests a 12-month upside of 68%. (See APLD stock forecast on TipRanks)

Rivian Automotive (RIVN)

Next up is Rivian Automotive, a company that is working to turn the emerging electric vehicle (EV) industry upside down. Every new firm in a new sector wants to be the great innovator, but Rivian is approaching the EV issue from a different angle, one that has potential to make a real difference. The company is designing a flexible EV chassis, with the electric drive system built in. Fittings are pre-installed for various battery systems, to fit the needs of the end-vehicle, and the chassis can be modified to feature a wide range of body types and seating arrangements.

Rivian currently has three vehicle models in early production stages and available for pre-order: the electric delivery van (EDV) for the commercial market, and two consumer market vehicles, the RT1, an all-electric light pickup truck for work or recreational use, and the RS1 electric SUV. The latter two vehicles have both on- and off-road capability. As of May 9, the company had received approximately 90,000 pre-orders and produced some 5,000 vehicles. All of Rivian’s vehicles are designed with a high level of interchangeable parts, for greater efficiency and cost control on the factory floors.

Rivian also entered, at the end of last year, a partnership with Amazon. This agreement is supporting the development and initial production of the EDV – and Amazon has ordered 100,000 vehicles from Rivian.

During the first quarter of this year, Rivian posted a $1.59 billion net operating loss, along with $95 million in revenue. The revenue total came in well below the $130 million forecast. The company announced that it received 10,000 new vehicle orders in the latter part of the quarter, after a price increase in March, and that its ongoing production ramp-up is proceeding smoothly. The company is on track to build 25,000 vehicles this year.

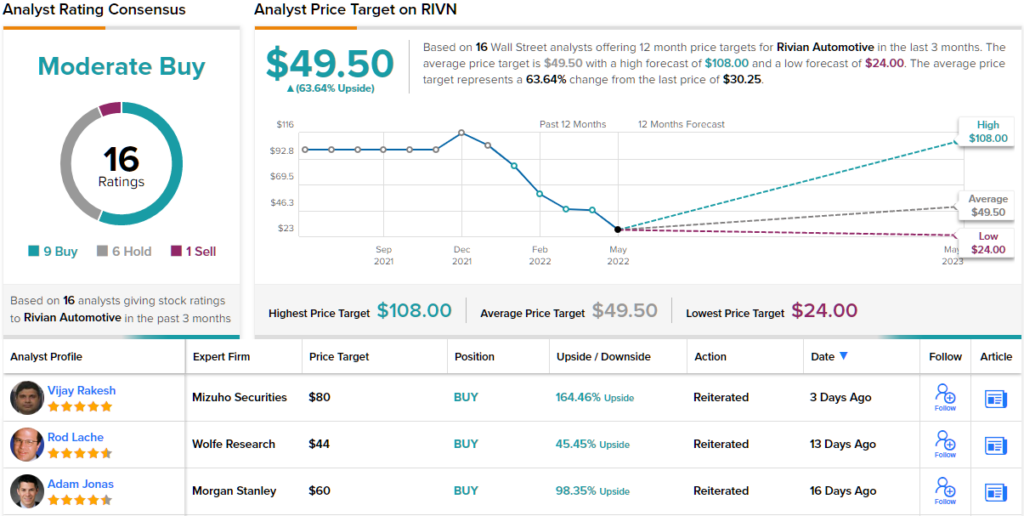

On the insider front, Jay Flatley of Rivian’s Board of Directors, has put his money where his mouth is, buying 40,000 shares for more than $1.17 million.

Morgan Stanley analyst Adam Jonas sees both positives and negatives in Rivian and sums them up for investors – while taking a long-term optimistic stance: “We sense a bit of a mismatch in growth vs. spending at Rivian that should be resolved through execution and improved transparency by year-end. The street still forecasts a company spending to be a highly vertically integrated Tesla competitor with 1 to 2mm units of capacity by end of decade. The forced-reality may be Rivian focusing on R1/EDV at Normal for the next few years before establishing a more functioning supply base from which it can unlock future opportunities.”

Jonas rates the stock an Overweight (i.e. Buy), and his $60 price target predicts a 98% upside for the year ahead. (To watch Jonas’ track record, click here)

Overall, there are 15 recent analyst reviews here, including 9 Buys and 6 Holds, for a Moderate Buy consensus rating. RIVN’s average price target of $49.50 suggests ~64% upside from the current share price of $30.25. (See RIVN stock forecast on TipRanks)

Last but not least is Casa Systems, a small-cap firm in the telecom sector. Casa is a designer and maker of advanced ultra-broadband solutions for the ongoing 5G rollout, providing hardware equipment for mobile, cable, fixed, and converged service providers. The company’s product line allows broadband network enterprise customers the agility and adaptability to deliver more efficient 5G service. Casa’s customer base includes such large names as SKtelecom, Taiwan Mobile, Yes, Verizon, and AT&T. The full list includes more than 475 firms across 70 countries.

Despite its strong position in the industry, Casa failed to impress with its 1Q22 financial results. The company reported top line revenue of $64.4 million, missing the forecast by a wide margin of 26%. Year-over-year, revenues were down 38%. EPS came in at a net per-share loss of 35 cents; this compared poorly to the 11-cent EPS profit in the year-ago quarter. Casa stated that it is suspending its 2022 full-year guidance, at least temporarily. The company attributed the decline in revenues and earnings to continuing supply chain difficulties.

On the positive side of the ledger, however, Casa also reported a positive cash flow of $18 million in the quarter, and increases in the work backlog and sales pipeline.

Looking at Casa’s insider trades, we find that over the past few weeks William Styslinger, a member of the Board, spent ~$580K buying 139,923 shares in the company.

Northland analyst Tim Savageaux, rated 5-stars at TipRanks, notes Casa’s recent difficulties but still comes out on the bullish side for the stock.

“Given the company’s scale we do believe a range of established and emerging competitors would find the company to be of strategic interest, and view this as lending support to valuation as the company undertakes this software transition and seeks to improve supply chain management and overall execution. Despite near term losses and uncertainty that have drove similarly situated peers historically toward the 1X revenue level or the $3.00 range, the company’s traction with VZ and engagement with other Tier 1 operators, as well as the strategic factor, likely supports a bottom at a higher level,” Savageaux explained.

Savageaux’s comments back up his Outperform (i.e. Buy) rating, while his $6 price target implies the stock has a 38% upside ahead of it. (To watch Savageaux’s track record, click here)

This small-cap telecom player features a 3 to 1 split in its analyst reviews, favoring the Buys over Holds and supporting a Strong Buy consensus rating. The stock is selling for $4.34 and has a $7.33 average target, suggesting ~69% upside from that level. (See CASA stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.