What to make of the markets today? After steep drops in January, February has seen increased volatility, with sharp swings up and down. That, combined with geopolitical tensions, stubbornly high inflation, and a Federal Reserve that is looking to raise rates more aggressively have made the markets – already tough to predict – more uncertain than ever.

In times like these, investors could use some clear guide toward the stocks that are primed for gains, but finding one is the trick. Investors will use a range of signals, signs, and clues to find the right stocks for difficult times. One of the best such signals – the insider trades. Insiders, corporate officers who are responsible not just to run their companies but also bring in the profits, don’t trade their own stock lightly. Rather, their trades are informed by the inside view they get of their companies’ prospects.

And that makes some recent insider trades particularly intriguing, from an investors’ standpoint. In recent days – just last week – we’ve seen two multi-million insider buys, on a couple of fascinating stocks. These trades, each well over $10 million, are an order of magnitude or more larger than the typical insider move, and are sure to attract investor attention.

We’ve used the Insiders’ Hot Stocks tool at TipRanks to pull up details on these stocks; we’ll take a look at them along with commentary from the Street, to find out what makes them so compelling.

EverQuote, Inc. (EVER)

We’ll start with EverQuote, the online insurance marketplace whose platform connects buyers and agents for insurance products of all types, from auto coverage to home and renter policies to life insurance. The platform allows insurance agents to both policies and prices, and allows buyers to search through the insurance markets, seeking specific products and price ranges. EverQuote takes its own share once a policy is purchased, when it received a fee from the policy issuer.

EverQuote saw higher sales in 2021 than 2020, with $418.5 million at the top line compared to $346.9 million; every quarter in 2021 saw a year-over-year gain. In Q4, the most recent reported, the company had $102 million in total revenue, up 5% yoy and beating the analyst estimates by 6%. The company’s net loss was 29 cents per share, slightly better than the 30 cent EPS loss predicted. At the same time, the loss was much deeper than in previous quarters, and compared unfavorably to the 13 cents EPS loss reported in the year-ago quarter.

In some metrics of note, DTCA revenue (which includes health, life, auto, and home verticals) saw 281% yoy growth. The company’s general non-auto insurance verticals were up 50%. And in a metric showing the strength of the company’s traffic generation operations, quote requests on the website were up 24.5% yoy.

In a move that demonstrates deep faith in the company, EverQuote’s co-founder and Board chairman David Blundin made a $15 million investment in the company. The investment came as a stock purchase by Recognition Capital, a business entity wholly owned by Blundin, and involved the purchase of 1,004,016 shares in EverQuote at $14.94 per share. The buy swung insider sentiment on EverQuote strongly positive.

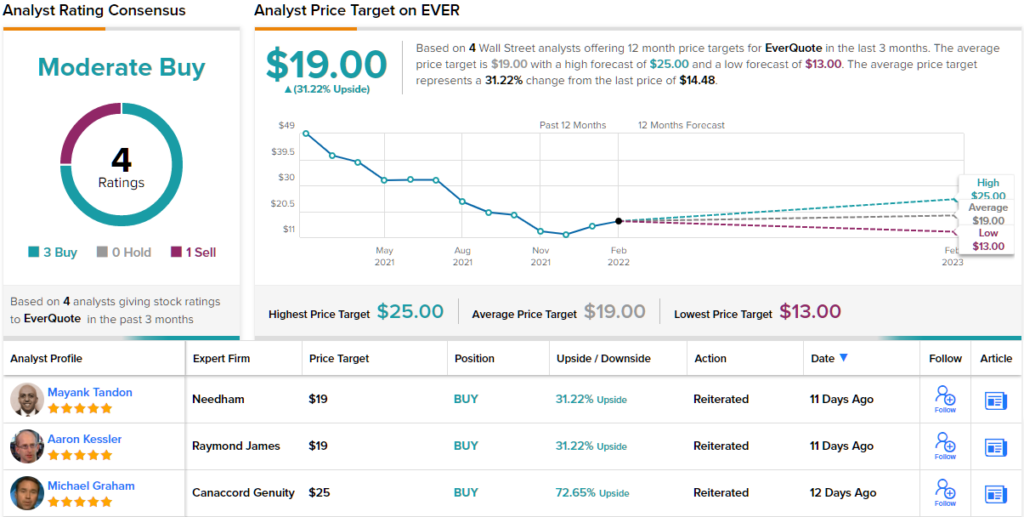

Blundin is not the only one willing to go out on a limb for EverQuote. Canaccord analyst Michael Graham, rated 5 stars by TipRanks, is also bullish here. Graham notes the headwinds in the company’s auto business, but adds, “Beyond Auto, there are several positive developments, including strong growth in Other verticals and a very robust Q4 Open Enrollment Period for the company’s DTCA Health offering. EVER stock has retreated significantly into value territory, reflecting Auto headwinds and broader tech sector pressure. While it may take the business working through a couple more modest quarters in its core Auto segment before we see renewed investor interest, we think the shares offer a good value proposition at current levels.”

These comments underlie Graham’s Buy rating, and his $25 price target implies an upside of ~71% for the coming year. (To watch Graham’s track record, click here)

Overall, EVER’s Moderate Buy analyst consensus rating is based on 4 reviews, including 3 Buys and 1 Sell. EVER shares have an average price target of $19, suggesting a one-year upside of ~31% from current levels. (See EVER stock forecast on TipRanks)

Alteryx (AYX)

And now we’ll turn to the software sector, where Alteryx, a California-based company, offers a range of data analytics and machine learning products designed to ease decision making and streamline ops for the customer base. The company’s software makes data analytics, a highly technical field, accessible to the average database user. Alteryx boasts over 7,000 customers globally, and more than 200,000 community members.

This February, Alteryx saw a couple of major announcements. On Feb 7, the company made public that it had completed the acquisition of San Fran’s Trifacta, cloud-based analytics firm. The move will bring an integrated end-to-end, low code/no code analytics automation platform into Alteryx’s product lineup for enterprise customers and moves Alteryx closer to becoming a cloud platform. Alteryx paid $400 million to make the acquisition.

And, on Feb 15, Alteryx announced its 4Q21 earnings results. Top-line revenue, at $173.8 million, was up 8% year-over-year. EPS did better, coming in at 17 cents, more than triple the 5-cent forecast, although it lost ground from the year-ago quarter. Even more important for investors, however, was the strong gain in annual recurring revenue (ARR). This key metric was up 30% yoy, and reached $638 million. The stock jumped 11% after the quarterly release.

On the insider front, Jeff Horing of the Board of Directors purchased more than 911,000 shares in AYX. The buy was made in three tranches, from Feb 22 to Feb 24, and the purchase price totaled some $49.96 million. Horing now controls $61.23 million worth of Alteryx shares.

5-star analyst Joel Fishbein, of Truist, is also upbeat on Alteryx and its stock. He writes of the company: “Despite a few moving parts due to the Trifacta acquisition and changes in accounting policy, we saw the increase in outlook and change in management’s tone as indicative of an inflection point in the business transition. Though there is still work left to do on both the product and GTM, we came away incrementally optimistic on the business and increase our estimates.”

To this end, Fishbein gives AYX shares a Buy rating, along with a $90 price target that indicates potential for ~46% upside gain in the next 12 months. (To watch Fishbein’s track record, click here)

Overall, AYX has a Moderate Buy rating from the Wall Street analyst consensus, based on 8 Buys and 4 Holds set in recent weeks. The stock is selling for $61.70, and the average price target of $80.36 implies an upside potential of ~30%. (See AYX stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.