Starbucks Corporation (SBUX), the iconic Seattle-based coffee company with more than 34,300 stores across the globe, has seen its shares decline by around 23% year-to-date, following the overall market correction and the ongoing war in Ukraine.

In my view, the recent pullback presents a solid opportunity for dividend growth investors who were previously reluctant to invest in the stock due to its relatively rich valuation. With the company’s financials and dividend growth prospects remaining strong and the dividend yield currently hovering close to 2.1%, Starbucks shares are looking rather attractive again.

I am bullish on Starbucks.

Q1 2022 Results

Starbucks reported very strong Q1 2022 results, with revenues growing 19% year-over-year to $8.1 billion. The company also posted EPS GAAP of $0.69, up 30% year-over-year. Non-GAAP (adjusted) EPS, which excludes restructuring and impairment costs, also came in strong, at $0.72, 18% higher year-over-year.

Q1-2022 revenues were 15.7% higher than its Q1 2020 revenues, suggesting that the company has not just recovered from the pandemic but even further grown throughout the past two years.

With Starbucks expanding its operations, economies of scale are gradually kicking in, leading to developing gross and EBIT margins. Last-12-month gross and EBIT margins currently stand at 22.7% and 16.2%. These figures compare to 21.3% and 5.83% in the prior-year period.

As Starbucks continues to grow its global footprint, it should be achieving successive cost efficiencies and operating synergies, potentially further expanding its margins.

Valuation, Dividend Growth

Starbucks’s EPS guidance for FY 2022 includes non-GAAP EPS growth between 8% and 10%. Accordingly, FY 2022 EPS should land close to $3.50. This implies a P/E of 25.6 at the stock’s current price levels, which is one of the more reasonable multiples the stock has traded at over the past several years.

Additionally, in the company’s earnings call, management guided for double-digit EPS growth post-2023, which is very encouraging to hear, and firmly justifies the current valuation, in my view.

Concrete EPS growth in the medium term should also permit management to sustain Starbucks’ strong dividend growth momentum.

The company’ three-year DPS CAGR currently stands at 10.8%. The latest hike back in September was by 8.9% to an annualized rate of $1.96. This suggests a payout ratio close to 56% on this year’s expected earnings.

In my view, this is a relatively comfortable ratio, leaving ample room for future DPS hikes, especially considering management’s EPS growth guidance post-2023.

The current yield close to 2.1% may not be not too rich. However, considering Starbucks’ EPS and DPS growth prospects, it makes for a sufficient tangible capital return.

Wall Street’s Take

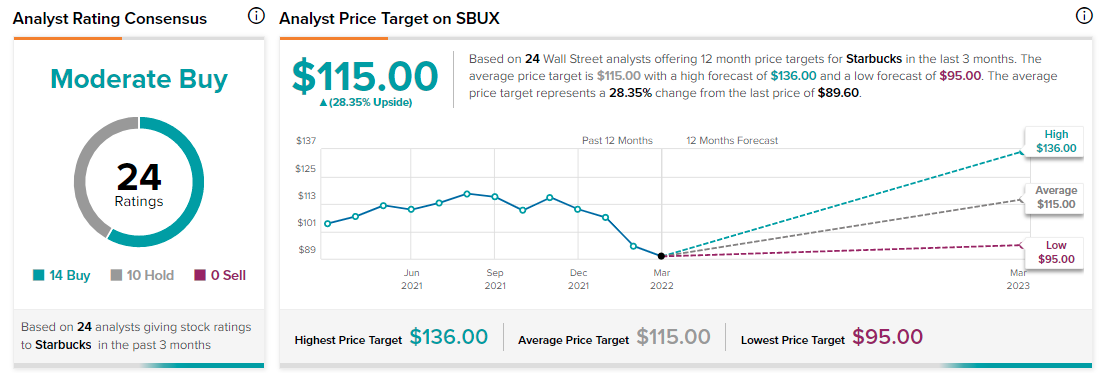

Turning to Wall Street, Starbucks has a Moderate Buy consensus rating based on 14 Buys and 10 Holds assigned in the past three months. At $115, the average Starbucks price target implies 28.4% upside potential over the next 12 months.

Conclusion

Starbucks is currently trading at the same levels it did around three years ago. Since then, however, the company has made robust advancements, while its latest results were quite encouraging.

Following the stock’s decline, Starbucks stock appears attractively priced based on this year’s projected EPS and management’s growth prospects post-2023. Hence, I remain bullish on the stock.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure