In less than a week, fintech SoFi Technologies (SOFI) is expected to report its Q1 earnings. And would you like to know beforehand what should investors expect SoFi will say?

Then you’re in luck. Turns out, Mizuho Securities analyst Dan Dolev has some thoughts on that score.

Writing in a pre-earnings note, Dolev starts out by noting that SoFi has guided investors to expect that it will report sales of $1.47 billion over the course of this year.

Working off that number, most analysts estimate that SoFi will report losses of $0.47 per share this year — just like it lost money last year, and just like it’s expected to lose money next year as well. But as Dolev explains, “SoFi is complicated,” and it’s possible that the company will actually report numbers better than either it, or the other analysts, have predicted. For his part, Dolev predicts a slight sales beat at SoFi this year — sales of $1.482 billion.

How does he figure that? “SOFI generates about 50-55% of its lending revenue from gains on loan sales (GoS),” says Dolev, which make up about 35% to 40% of the company’s total revenue in a year. Now, some investors fear that as interest rates rise, such SoFi’s GoS margins will deteriorate. If you’re an investor, why buy a loan that’s paying 3% interest, for example, if new loans might soon be generating interest rates of 4% or more?

But in Dolev’s view, SoFi could lose as much as $177 million in GoS revenue, and still be okay for the year, because it has hedged its position against interest rate hikes. As the analyst notes, this already “proved effective in 2021 as interest rates rose for the first time in years.” Moreover, that level of lost revenue would only happen if the Fed raises interest rates 10 times, at a quarter point per hike. Any fewer, and SoFi would lose less revenue and its hedges would therefore become a net addition.

At the same time, Dolev sees rising interest rates potentially benefitting SoFi on the banking side (SoFi won approval its banking charter in January) as the company reaps higher net interest income on its loans. This income could be perhaps as much as $110 million to $115 million, rather than the $70 million to $75 million estimate incorporated in the company’s guidance. It’s this potential for higher interest income which explains why Dolev tweaked his estimate for adjusted net revenue this year to $1.482 billion.

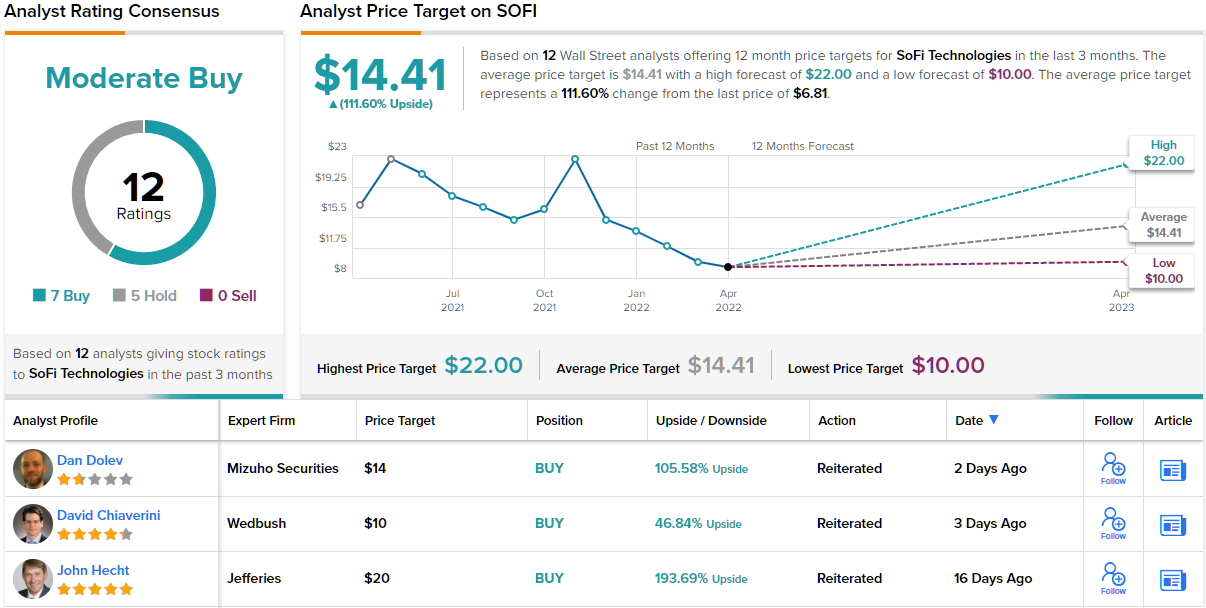

In short, rising interest rates aren’t as big a threat to SoFi hitting its numbers this year, as some investors may fear. For this reason, Dolev says he’s standing pat on his price target of $14 for SoFi stock, and his Buy recommendation on the stock. If he’s right, investors stand to pocket ~106% gain over the next 12 months. (To watch Dolev’s track record, click here)

Looking at the consensus breakdown, 7 Buys and 5 Holds have been published in the last three months. Therefore, SOFI gets a Moderate Buy consensus rating. Based on the $14.41 average price target, shares are poised to rise ~112%. (See SOFI stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.