E-commerce stocks have taken several steps back over the past year as tech names from across the board took a violent tumble. As shares stabilize, I think now could be a good time to go shopping for value.

Undoubtedly, a rate-induced recession and a potential pullback in consumer spending seem to be on the way. While consumers have already reacted to high inflation and a weakening economy, it’s tough to tell just how much the battered e-commerce darlings stand to fall as consumers rein in spending.

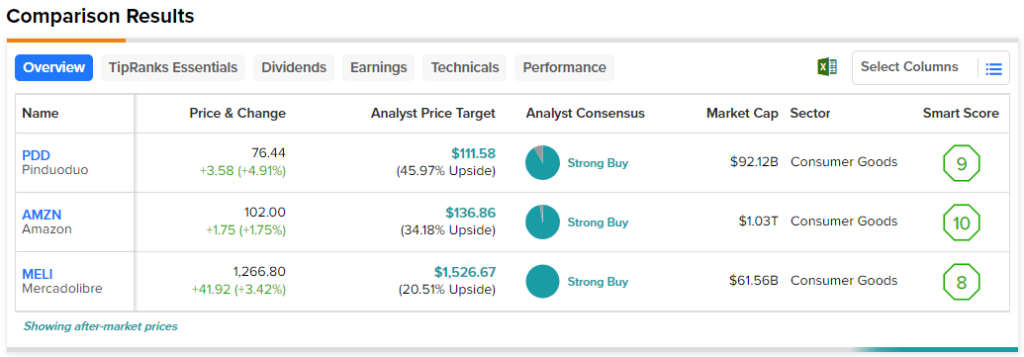

In any case, let’s use TipRanks’ Comparison Tool to get a glimpse of three Strong-Buy-rated e-commerce plays.

Amazon (NASDAQ:AMZN)

Amazon stock seems ready to move on after enduring a 55% peak-to-trough fall. An overinvestment in capacity, macro headwinds, and rocky leadership from CEO Andy Jassy may still be causes for concern. Regardless, I still view Amazon as one of the most innovative and disruptive companies out there. With layoffs and other cost cuts in the rearview, I think Amazon has a lot of things it can do to reignite investor enthusiasm again, even in the face of recession headwinds. I am bullish.

Management provided cautious guidance, which, I believe, lowers the bar drastically. With inflation and a recession in the cards, it’s firms like Amazon that tend to take a spill well before it has a chance to report truly hideous numbers. While Amazon has disappointed in past quarters, I don’t think we’ve seen something truly horrific from the firm yet. I think today’s depressed multiples suggest that such a quarter is being priced in.

As Amazon continues to build market share with innovative platforms (think the all-in-one Buy with Prime service, which “allows US-based Prime members to shop directly from participating online stores using the Prime shopping benefits they love and trust”), I’d look for Amazon to be one of the leaders once the market’s ready to focus on an economic recovery.

It’s hard to tell where Amazon goes from here. A recession hasn’t even hit yet. AWS and retail sales could easily continue to drag their feet. In any case, I find it hard to pass up the proven innovator while it’s trading at 2.0 times sales, 45% lower than its five-year average. That’s too low for a disruptive innovator.

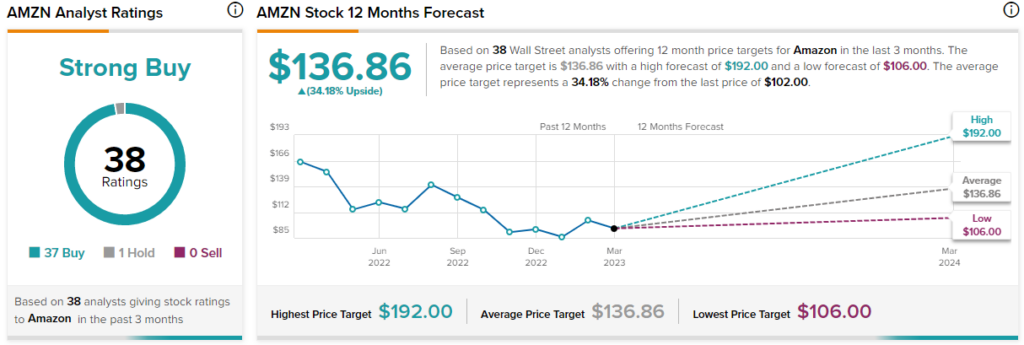

What is the Price Target for AMZN Stock?

Analysts expect big things from the e-commerce behemoth, which remains a Strong Buy with 37 Buys and just one Hold. The average AMZN stock price target of $136.86 implies 34.2% upside potential.

MercadoLibre (NASDAQ:MELI)

MercadoLibre is an e-commerce company that operates in Latin America. It’s essentially the Amazon for a number of countries in the Latin American region. Like Amazon, MercadoLibre’s reach goes well beyond just digital sales. The company has a financial business (payments and lending), a robust ad business, and a logistics division (Mercado Envios). With a long growth runway and a dominant presence in Latin America, I am bullish.

Undoubtedly, macroeconomic headwinds have weighed across all parts of the globe. Still, in its latest quarter (Q4), MercadoLibre posted some impressive results, with per-share earnings of $3.25, well ahead of the $2.42 estimate. Therefore, even as consumers felt the pinch of a slowing economy, the company managed to power enviable growth rates, thanks in part to its financial services and ads.

Indeed, there are still plenty of opportunities to transition consumers away from using cash. Therefore, as impressive as the $65 billion e-commerce firm is with its online marketplace, it’s the fintech business that could help jolt growth and pad margins.

Looking ahead, MercadoLibre still appears to have its foot on the pedal. The company is slated to invest $1.6 billion in Mexico this year into improving its e-commerce capabilities, financial services, and logistics. The money will also go toward marketing.

At 72.5 times forward earnings, MELI stock still looks expensive even though shares are off 37% from their highs. Nonetheless, the stock is a lot cheaper from a historical perspective. MercadoLibre has commanded price-to-earnings (P/E) multiples in the hundreds in the past. You have to pay up for growth. At these levels, I don’t think investors are paying up all too much, at least historically speaking. Analysts agree.

What is the Price Target for MELI Stock?

Wall Street loves MercadoLibre, with a Strong Buy rating based on nine unanimous Buy ratings. The average MELI stock price target of $1,526.67 entails a 20.5% gain from here.

PDD Holdings (NASDAQ:PDD)

PDD Holdings is a Chinese e-commerce company that took the hardest hit of the names in this piece. At its worst, shares crumbled nearly 89%. Shares eventually recovered but are now back in retreat mode, now down almost 30% from 52-week highs. Though the latest quarter was worrisome, I remain bullish.

Shares took a 14% hit when PDD revealed disappointing fourth-quarter results. The owner of Pinduoduo and Temu missed on revenue ($5.77 billion vs. $6.025 billion estimate) and posted a slight miss on per-share earnings ($1.21 vs. $1.22 estimate). Moving forward, PDD stock is likely to be a very choppy roller-coaster ride as the Chinese economic recovery continues dragging out.

At 22.9 times trailing price-to-earnings with solid growth ahead (analysts expect 28% revenue growth this year), PDD Holdings may very well be the best bargain of the batch. Still, there are added risks to investing in Chinese stocks. Most notably, delisting is a concern common in any U.S.-listed Chinese stock. Though it’s challenging to gauge said risks, I think those comfortable with bearing them could have a shot at an outsized reward.

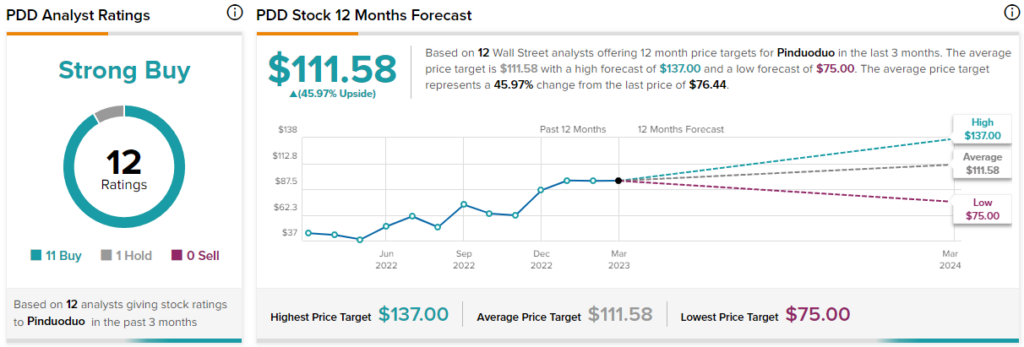

What is the Price Target for PDD Stock?

Analysts have a Strong Buy rating on PDD, with 11 Buys and one Hold. The average PDD stock price target of $111.58 implies 46% upside potential.

Conclusion

If the Fed can accomplish its mission (I think that’s a likely scenario) and orchestrate a soft landing for the economy, then the recession risk baked into e-commerce plays may be overblown. With recent regional bank failures, the Fed may not need to raise rates as much as initially expected, which could bode well for stocks.