One thing is certain in the stock markets lately: their inherent uncertainty is taking charge, and high volatility is here to stay. For months, investors and economists have worried about the recessionary effects of the Federal Reserve’s anti-inflationary interest rate hikes – but the recent bank crisis has added another layer of concern to an already tumultuous situation.

Now, we’re dealing with the fallout from that crisis, and inflation and interest rates both remain high. It’s a textbook case for going long on defensive stocks.

That’s the view of Deep Mehta, a vice president at Goldman Sachs. Closing out the month of March, Mehta says: “Recent stress in the banking industry has resulted in renewed investor concerns around the economic growth outlook, and increased volatility in risk assets. While the price action stress has somewhat stabilized, potential for reduced credit availability is likely to pose a growth headwind as per GS economists. We believe this backdrop warrants selectively positioning in more defensive pockets of the market.”

It’s a mindset that naturally turns us toward dividend stocks. These are the traditional defensive investment plays, offering steady payouts to shareholders that guarantee an income stream whether markets go up or down.

Against this backdrop, Goldman Sachs analysts have given the thumbs-up to two dividend stocks yielding at least 8%. Opening up the TipRanks database, we examined the details behind these two to find out what else makes them compelling buys.

Altria Group, Inc. (MO)

Altria Group is one of the world’s largest cigarette makers, and owns the well-known Marlboro brand. While the company has built itself into one of the world’s major public firm through the tobacco industry, in recent years it has begun to diversify beyond just cigarettes and other tobacco products. While a diversified product line is usually beneficial, in Altria’s case it provides a cushion against changing social and political winds that no longer favor the core tobacco product lines.

Specifically, Altria has been making moves into the smokeless tobacco realm, and into the e-cigarette, or vaping, sector. To that end, the company announced early in March that it had entered a ‘definitive agreement’ with NJOY Holdings, with particular attention to gaining ownership of NJOY portfolio of e-vape products. Altria has reportedly agreed to pay up to $2.75 billion in cash at transaction closing, and up to an additional $500 million in cash pending regulatory outcomes on some part of NJOY’s products. Backing the deal, Altria notes that last year there were 9.5 million adult vape users in the US, and the market for vapes reached $7 billion in US sales.

In addition to shifting toward smokeless products, Altria has also made some major strategic investments, and holds a 10% stake in AB-Inbev, a major name in the brewing industry. Altria also holds 41% ownership of Cronos Group, a major operator in the Canadian cannabinoid market.

On the financial side, Altria last reported quarter – 4Q22 – showed mixed results. The company had net revenues of $6.1 billion, down 2.3% year-over-year, and an adjusted diluted EPS of $1.18, up 8.3% y/y. The revenue figure missed the forecast by $70 million, while the EPS was ahead of expectations by 1 cent.

In 4Q22 Altria reported the completion of its previously authorized $3.8 billion capital return program of share repurchases – and authorized an additional $1 billion in repurchases to continue the returns. The company also paid out $1.7 billion in dividends during Q4, part of the $6.6 billion paid out in the full-year 2022. For fiscal years 2018 through 2022, Altria has paid out over $30 billion in dividends, and repurchased more than $6 billion in stock shares.

The current dividend, scheduled for an April 28 payment, is set at 94 cents per common share. With an annualized rate of $3.76, the dividend yields an impressive 8.4%, more than 4x the average div yield found on the S&P 500. Altria has kept up reliable dividend payments since 1989.

Goldman analyst Bonnie Herzog takes an unequivocally bullish position on Altria, writing of the stock: “We continue to recommend MO’s stock as we have strong conviction that it will be able to comfortably deliver on its MSD EPS growth target for FY23 and MSD CAGR through FY28. Furthermore, we believe MO is among the best positioned in uncertain/recessionary markets, and we see limited downside risk given MO’s strong underlying FCF, lack of FX exposure, attractive and expanding gross margins, attractive valuation, and a strong balance sheet with a focus on shareholder returns and a very attractive dividend yield…”

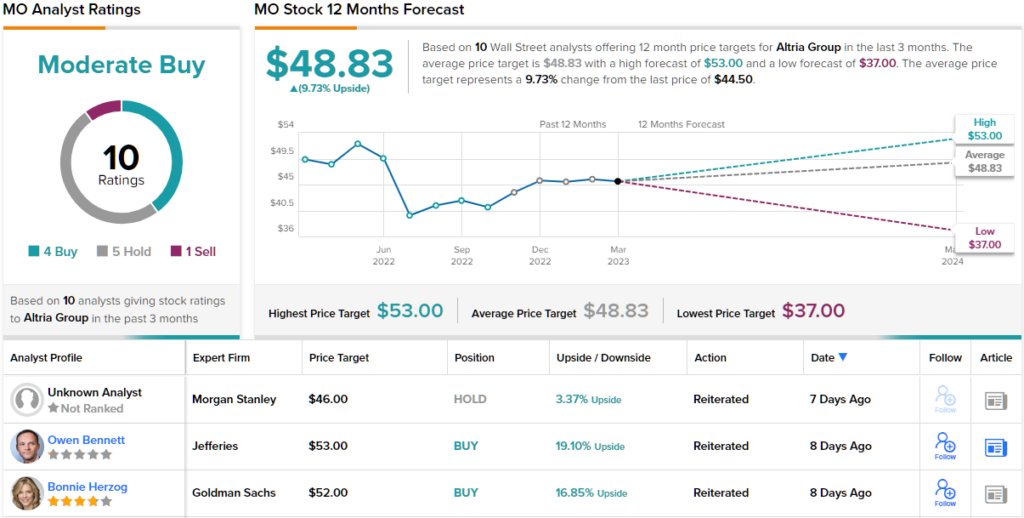

Along with this upbeat stance, Herzog gives MO shares a Buy rating and a $52 price target that implies a one-year potential gain of ~17%. (To watch Herzog’s track record, click here)

Overall, Altria gets a Moderate Buy rating from the analyst consensus, based on 10 recent Wall Street reviews that break down to 4 Buys, 5 Holds, and 1 Sell. (See MO stock forecast)

Diamondback Energy (FANG)

The next Goldman pick we’re looking at is Texas-based Diamondback, an independent operator in the oil and natural gas industry, focused on exploring and exploiting unconventional oil and natural gas plays in the Permian Basin of West Texas. This is the geological formation that, in the past decade, put Texas back on the map as a major player in the global energy industry, and Diamondback has been successfully realizing strong profits from its operations there.

Diamondback is mainly working through horizontal exploitation, a method of tapping hydrocarbon reservoirs that are difficult of access. Within the larger Permian Basin, the company is working in the Wolfcamp, Spraberry, and Bone Spring formations.

In addition to profits, Diamondback has also built a reputation, in an industry known for high capital returns, for keeping up a high capital return through the dividend. For the past year, the company has regularly paid out both a base dividend and a variable dividend to all common shareholders. In the last declaration, Diamondback set the base payment at 80 cents per share, for a 7% increase in the $3.20 annualized payment. At that rate, the base dividend yields 2.4%. With it came a variable dividend declaration, of $2.15 per share, bringing the total dividend payment for 4Q22 to $2.95. The combined dividend, assuming continued high variable payments for the rest of the year, annualizes to $11.80 per share and yields an 8.8%.

These dividends are supported by the company’s generally sound financial performance. In Q4, Diamondback saw an average daily production of 226.1 thousand barrels of oil daily, which brought in net revenues of $2.03 billion and a non-GAAP EPS of $5.29. The revenue figure just missed the forecast, by $60 million, while the EPS figure was 2 cents ahead of expectations.

For Neil Mehta, one of Goldman’s 5-star analysts, this adds up to a sound investment. Mehta writes of Diamondback: “We remain Buy rated on FANG as we see a favorable setup for the company as it continues to strengthen its balance sheet though FCF generation… We see FANG generating 10%/12% FCF yield in 2023E/24E vs. large cap E&P peers… at 9%/9% and returning ~$1.5 bn in dividends and ~$0.8 bn in share repurchases representing total capital returns yield of ~9% in 2023E… We believe such factors can drive further outperformance in FANG shares relative to peers.”

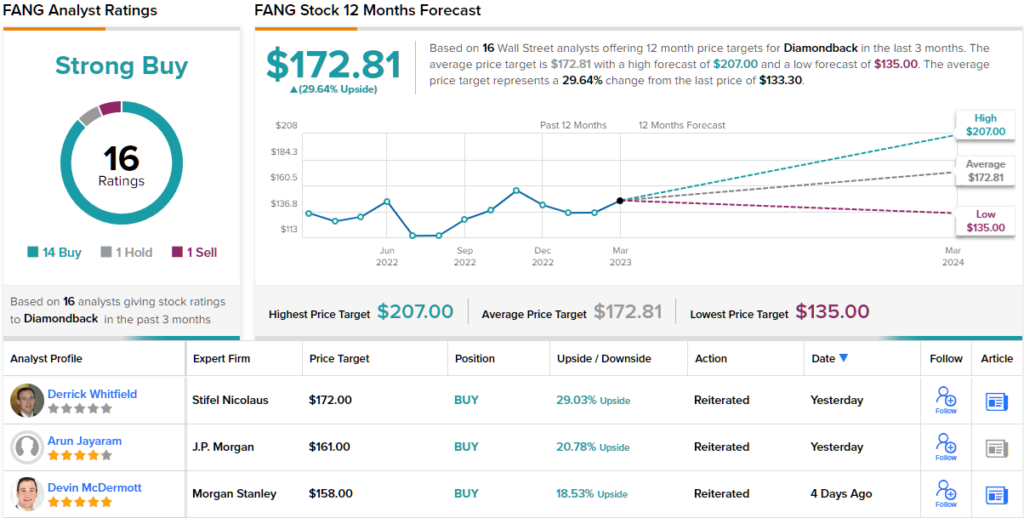

In addition to his Buy rating for the stock, Mehta gives FANG a $142 price target, suggesting a gain of ~7% on the one-year horizon. Based on the current dividend yield and the expected price appreciation, the stock has ~15% potential total return profile. (To watch Mehta’s track record, click here.)

Overall, Wall Street likes Diamondback Energy, as shown by the Strong Buy consensus rating. This is based on 16 reviews from the analysts, whose recommendations include 14 to Buy along with 1 Hold and 1 Sell. The stock’s $172.81 average price target is much more bullish than Mehta’s, implying a 29% one-year upside form the current trading price of $133.30. (See FANG stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.