There are plenty of reasons for caution in the markets right now. The big point is inflation, which is stubbornly high and continuing to rise. In response, the Federal Reserve has begun to raise interest rates and tighten up on monetary policy – but this raised the possibility of recession, a fear that just go a boost from the 1Q22 GDP numbers, which contracted at an annualized rate of 1.4% for the quarter. This is a dramatic change from the blistering near-7% growth reported in 4Q21, and back up fears that the combination of inflation and a Fed policy switch is starting to stifle economic activity.

On top of all that, we’re also looking at renewed, and even harsher, lockdown policies in China, which bodes ill for that country’s manufacturing and export sectors – and slowdown in China’s exports will have a heavy impact on US consumption.

And if all that weren’t enough, there’s the Russia-Ukraine war. The economic and trade sanctions imposed on Russia by the Western nations are still reverberating in the world’s financial sectors, impacting banks and commodity markets.

In response, investors are making the obvious move: getting into defensive stocks.

Equity strategist Michael Wilson, in a look at the markets from investment bank Morgan Stanley, writes of this defensive mindset: “With defensives the latest big outperformer, they are now expensive, leaving very few places to hide. This suggests the S&P 500 will finally catch up to the average stock and enter a bear market.”

Wilson is not the only market watcher showing a serious interest in defensive stocks. Wall Street is clearly paying attention to them, and it’s no wonder why: some are showing yields of 8% or better, and even with interest rates rising, a dividend of that magnitude is a clear outperformer. Using the TipRanks database, we’ve picked out two of these high-yield dividend payers, which also boast Strong Buy consensus ratings from the Street. Let’s take a closer look.

TPG RE Finance Trust (TRTX)

We’ll kick it off with TPG, a real estate investment trust (REIT) company. These companies are perennial dividend champions, in part due to tax regulations that require them to return a high percentage of profits directly to shareholders – and dividends are a logical vehicle for that return. TPG has a reliable dividend history going back to 2017; in that time, the company has not missed a quarterly payment, and has even added special dividends at times.

Finishing last year, TPG was managing a $5.4 billion real estate asset portfolio; of that total, 71% was made up of commercial office space and multifamily dwelling units. The company’s business is focused on the Eastern and Western US markets, which together account for 63% of the portfolio’s geography.

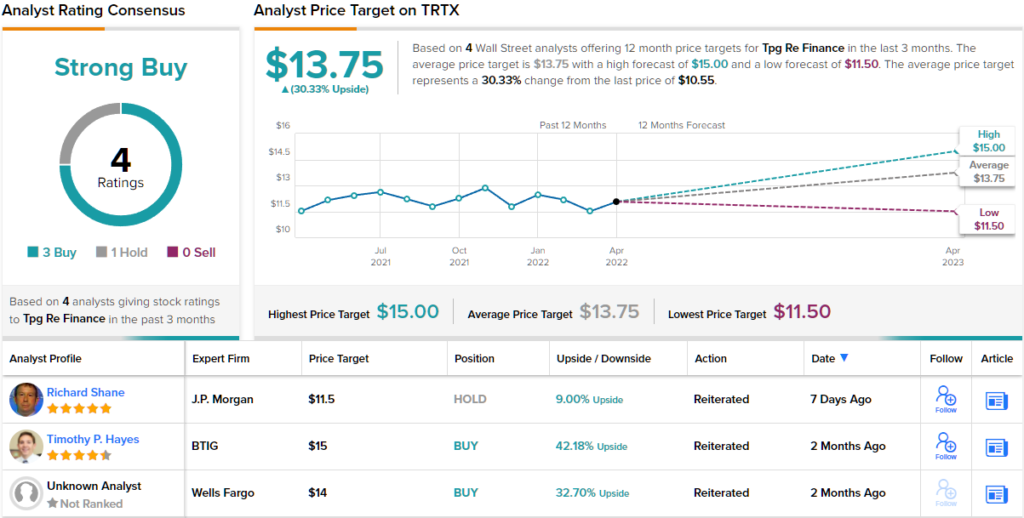

The company will report its 1Q22 financial results this Tuesday, May 3, but we can get a good feel for its current situation by looking back at the Q4 results. The company generated a bottom line, in GAAP terms, of 51 cents per diluted share, a sum more than adequate to support the dividend payment, set at 24 cents per common share with a 7-cent special dividend added on. The regular payment, annualizing to 96 cents per common share, gives a yield of 8.7%.

5-star analyst Donald Fandett, of Wells Fargo, is bullish on TPG and writes: “Proceeds from asset sales and other factors should drive some modest dividend upside going forward… TRTX should [also] benefit over time as rates rise, particularly as loans originated with high libor floors roll off or get repaid… TRTX shares trade at a discount to the peers who are north of 1xBV, a gap we expect to close over time. And the company has a new CEO… who was the Head of US commercial real estate debt at Goldman Sachs.”

Overall, Fandett believes this is a stock worth holding on to. The analyst rates TRTX shares a Buy, and his $14 price target suggests a solid upside potential of ~33%. (To watch Fandett’s track record, click here)

The recent analyst reviews on this stock break down 3 to 1 in favor of Buy over Hold, giving a Strong Buy consensus rating. Shares are priced at $10.57 and the $13.75 average target implies ~30% upside from the current level. (See TRTX stock forecast on TipRanks)

PennyMac Mortgage (PMT)

Next up is PennyMac Mortgage, another REIT, operating in the mortgage investment trust sub-sector of the business. Rather than making direct investments in real property, PennyMac invests in mortgage-backed securities and direct loans to buyers.

While the real estate market was hot last year, PennyMac underperformed. In 4Q21, the last quarter reported, PennyMac showed investment income of $49.5 million, a top line that was down from $196 million in the year-ago quarter. The company registered a net loss of 28 cents per share in the quarter.

Despite these lackluster results, PennyMac kept up its dividend. The most recent declaration, for 47 cents per common share, was paid on April 15. With an annualized rate of $1.88, the common share dividend gives a robust yield of 12%. With average dividends among S&P companies running at ~2%, and Treasury bonds still yielding less than 3% despite recent increases, the attraction of PennyMac’s dividend is clear.

PennyMac stock is covered by BTIG analyst Eric Hagen, who notes the headwinds in the mortgage market and still comes down on an optimistic note.

“Levered mortgage investors face the risk of earnings compression connected to aggressive Fed policy, but beneath the overhang, we can still identify select catalysts which are largely disconnected to the level and direction of interest rates and mortgage spreads… We want to remain long the common stock here. PMT also has preferred stock yielding [12]%, with lower spread risk and funding sensitivity as a result of sitting higher in the capital structure.”

These comments back up Hagen’s Buy rating on PMT stock, and his $18.50 price target implies a one-year upside of ~20%. (To watch Hagen’s track record, click here)

The rest of the Street supports Hagen’s thesis. There are 5 analyst reviews here, including 4 Buys and 1 Hold, giving the stock a Strong Buy consensus rating. PMT is selling for $15.37 and has an average price target of $18.80, for ~22% upside potential. (See PMT stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.