Inflation, supply chain issues, and soaring commodity prices are plaguing companies across seemingly every major industry, and the electric vehicle (EV) sector is no exception. Last week, inflation in the U.S. soared to a 40-year high, not to mention the rising prices of oil and gas accelerating already concerning trends of rising costs.

According to a U.S. Department of Labor press release last week, over the past year, the U.S. Consumer Price Index (CPI) rose to 7.9% before seasonal adjustment. According to this press release, “Increases in the indexes for gasoline, shelter, and food were the largest contributors to the seasonally adjusted all items increase.”

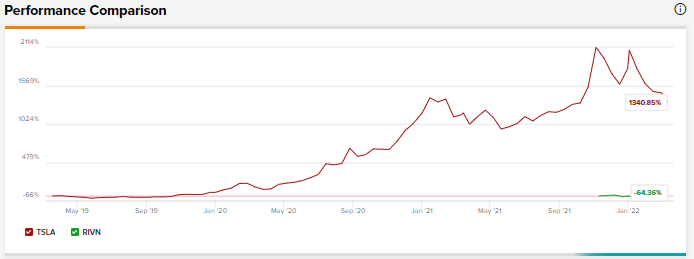

Using the TipRanks stock comparison tool, we compared two EV companies, Rivian and Tesla, which are directly up against these challenges.

Rivian (NASDAQ: RIVN)

Shares of Rivian have tanked about 18.5% in the past five days as investors were disappointed with the electric automotive company’s Q4 results – Rivian’s first quarter following its initial public offering (IPO) late last year.

In Q4, RIVN reported revenues of $54 million upon the delivery of 909 vehicles, falling short of the consensus estimate of $61.2 million.

Inflation and supply chain issues negatively impacted RIVN’s gross profit which was a negative $383 million in Q4. Perhaps passing on inflationary costs to consumers, the company raised its prices for its R1 platform from a starting price range between $67,500 and $83,000 to between $67,500 and $95,000, representing a 14.5% hike in prices.

In its letter to shareholders, Rivian stated that the R1 platform at the new price range will include “both Quad and Dual-Motor configurations as well as a Standard battery pack.”

However, according to a Carbuzz report from March 2, the company had earlier raised the price of its dual-motor R1T and R1S to $78,975 and $84,000 for the R1T and the R1S, respectively, bowing to inflationary pressures. Earlier, Rivian was selling these models at a price of $67,500 for the R1T and $70,000 for the R1S.

According to Wedbush analyst Daniel Ives, this 20% price hike was rolled back in 48 hours as customers canceled their orders for the R1T and R1S.

So, is the Rivian story broken or salvageable as the company expects inflation and supply chain issues to drag down 2022 as well?

The company’s management attempted to answer this question on its Q4 earnings call. Rivian’s CFO Claire McDonough commented that while its plant in Normal, Illinois had an expected capacity to produce 150,000 units this year, the plant has been supply-constrained to produce only 25,000 vehicles.

McDonough added that “the supply chain environment is a key factor in regards to the margin rate that we expect to have. Inflation also has clearly been a factor here as well. Rivian is not alone in regards to the overall raw material input prices that are obviously impacting EVs across the board.”

As of March 8, the company had 83,000 preorders for R1 and its production outlook of 25,000 vehicles was “disappointing as the Street was modeling in the 40k range,” according to Ives.

While the top-rated analyst believes that Rivian has immense potential to “be a major EV stalwart over the next decade,” it needs to stop the excuses and start the delivery of its models.

Ives, while reiterating a Buy rating on the stock, expects RIVN “to fix this nightmare situation and emerge a stronger company into the second half of 2022 and 2023 and fulfill its potential with the valuation stabilizing as the company hits its key targets.”

Considering this bleak outlook in 2022, Ives more than halved his price target from $130 to $60 on the stock, though still implying an upside potential of 65.56% from 11:11am EST intraday trading prices on Monday.

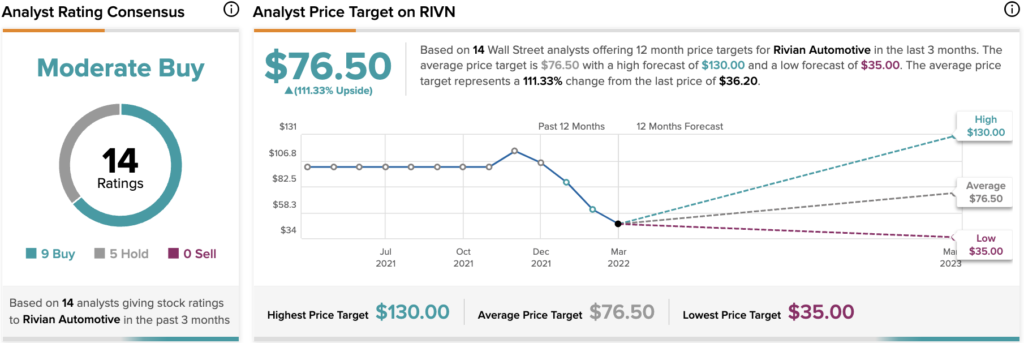

Other analysts, however, are cautiously optimistic about the stock with a Moderate Buy consensus rating based on nine Buys and five Holds. The average Rivian stock prediction is $76.50, which implies upside potential of approximately 111.33%.

Tesla (NASDAQ: TSLA)

Inflation is weighing on Elon Musk’s mind, too. In a series of tweets on Monday, the CEO of Tesla asked users about what the probable inflation rate over the next few years would be. Moreover, Musk warned that Tesla and SpaceX are “seeing significant recent inflation pressure in raw materials & logistics.”

Indeed, Tesla has also bowed down to these inflationary winds and raised the prices of its long-range Model 3 and Model Y by $1,000 each, according to a report by electrek. The report pointed out that TSLA has only raised the prices of its EV models with nickel in their batteries.

Nickel is proving to be a sore point for EV makers as its price surged to a record $100,000 per ton last week, finally stabilizing at about $48,000 per metric ton.

So, how will Tesla fare amid these challenges? Global Equities Research analyst Trip Chowdhry’s factory checks on March 12 indicated that in Q1, the company’s deliveries of its Model S Plaid were up 15% on a quarter-over-quarter basis. Moreover, it seemed that the deliveries of its Model X Plaid had also picked up.

The analyst pegged this delivery activity in Q1 as “monstrous” and remained bullish with a Buy rating and a price target of $1,500 on the stock. Chowdhry’s price target is not so far off from the Street’s highest price target of $1,580.

This same bullish stance was echoed by Wedbush analyst Daniel Ives. He was encouraged by Tesla’s approval from German authorities to begin production at its Giga Berlin factory earlier this month. Ives believes that it was extremely important for production to start at Giga Berlin in order to expand TSLA’s footprint in Europe. After all, the “logistics of producing cars in China at Giga Shanghai and delivering to customers throughout Europe was not a sustainable trend,” according to Ives.

Ives admitted that production remains tight for Tesla, and the demand for its vehicles has continued to outstrip supply. With production approval for Giga Berlin, and production already underway at Tesla’s new factory in Austin, Texas, the analyst believes that this ramp-up in production will “help solve the bottlenecks of production for Tesla globally.”

By the end of this year, the analyst anticipates that TSLA will have the capacity to produce approximately 2 million units annually. This is a considerable increase from Tesla’s approximately 1 million units in 2021.

Moreover, Ives expects that the semiconductor chip shortage will be “a moderating issue” and that supply chain constraints will ease this year for Tesla. He also brushed aside “logistical hurdles” as mere near-term headwinds and reiterated a Buy rating and a price target of $1,400 on the stock.

Other analysts, however, are cautiously optimistic about the stock with a Moderate Buy consensus rating based on 15 Buys, seven Holds, and six Sells. The average Tesla stock prediction is $1,068.40, which implies an upside potential of approximately 37.13% as of intraday trading prices at 11:33am EST Monday.

Bottom Line

While supply chain issues and inflation continue to be significant bumps in the road for both TSLA and RIVN, it seems TSLA is better positioned to ride over these obstacles. However, based on the average analyst upside potential over the next 12-months, Rivian could be considered to be the better Buy.

Download the TipRanks mobile app now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure.