The unfortunate buzzword for 2022: inflation. Wherever you go, it has been hard to avoid this hot topic, as inflation has soared to heights not seen in decades, with the central bank eventually declaring it will do all that’s required to tame it.

The combination of high inflation, attendant rate hikes and fears of a recession have also spooked the markets which have been on a downtrend for most of the year.

With the August inflation reports due this week (CPI on Tuesday & PPI on Wednesday), the markets will be keen to find out the results.

The good news is that according to Raymond James CIO Larry Adam, the investment firm’s scouting report is “projecting signs of improvement.” Why? “There is a full line-up of indicators reflecting easing inflationary pressures—even a few from the stickier areas of inflation.”

Amongst these are the ongoing normalization of the money supply, the strong dollar which has “drastically cheapened the cost of imported goods,” a pullback in shipping costs and an improving supply chain. Not to mention, petrol prices have been falling for 86 consecutive days, amounting to the longest streak of declines since 2015.

Against this backdrop, Raymond James analysts have been seeking out opportunities for investors while inflation is set to ease. They have homed in on two names which they project are ready to push ahead.

According to the TipRanks platform, they are also Buy-rated by the analyst consensus and set to generate some handsome gains over the coning months. Let’s see what makes them appealing investment choices right now.

V2X (VVX)

The first stock we’ll look at is from a newly formed company; V2X is the result of a merger of equals between public entity Vectrus and privately-held Vertex, which took place in July. The newly formed company offers comprehensive mission support services and solutions for defense and national security customers worldwide, including logistics, training, facility operation, aerospace MRO, and technology services. Combined, the pair have 120 years of ongoing mission support while numbering 14,000 employees.

The new combination has yet to report quarterly earnings, but we can look at Vectrus’s latest results and outlook to find out the impact the merger will have.

In Q2, the company generated revenue of $498 million, amounting to a 6% year-over-year increase and a 9% sequential uptick. Adjusted EBITDA came in at $24.7 million (5.0% margin), rising by $6.5 million quarter-over-quarter and by 100 basis points.

Those figures, however, are going to get a lot bigger in the year’s latter half when the results will factor in the merger. H2 revenues are expected in the range between $1.9 billion-$1.94 billion, adjusted EBITDA in the $140 million-$150 million range and operating cash flow between $130 million-$150 million (operating cash flow in Q2 was $46 million).

It is the potential of the merger which excites Raymond James’ Brian Gesuale the most, who believes the combination of Vectrus and Vertex “far exceeds the quality of the two enterprises from a standalone basis.”

“We won’t over-indulge the clichéd 1+1 = 3 but would be remiss to not point this out given the institutional investor memory likely defaults at Vertex/L3 or Vectrus/Exelis as standalone entities,” the 5-star analyst went on to say. “V2X is broader from customer and concentration standpoint, faster growing, more diversified, and has a higher margin profile than Vectrus. Importantly, shares are still trading like its traditional Vectrus and at a massive discount to peers. As investors become acquainted with the new entity and as management executes, the multiple could expand ~2-turns on an EV/EBITDA basis and still remain a double-digit discount to most peers.”

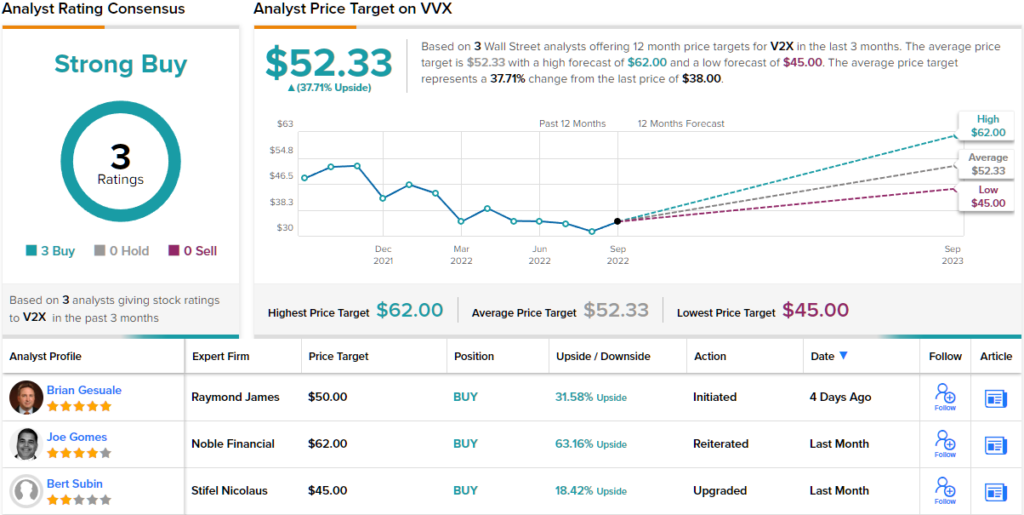

Get on board appears to be Gesuale’s message, who rates the stock a Strong Buy while his $50 price target makes room for one-year gains of ~32%. (To watch Gesuale’s track record, click here)

Only two other analysts have been tracking this company’s progress, but both are also positive, providing VVX with a Strong Buy consensus rating. Going by the $52.33 average target, the shares are expected to yield returns of ~38% over the 12-month timeframe. (See V2X stock forecast on TipRanks)

Allegiant Travel Company (ALGT)

Let’s now pivot toward the airline industry, to North America’s fourteenth-largest commercial airline, the ultra-low-cost Allegiant.

The airline industry is currently in the throes of recovery following the disastrous implications of the pandemic. Although global airline traffic is still around three-quarters that of 2019 levels, the latest IATA data for July showed a significant comeback from 2021 levels and the improvement is expected to continue into 2023.

This has been reflected in Allegiant’s preliminary passenger traffic results for July, which showed the airline flew a total of 1.94 million passengers during the month compared to the 1.75 million in pre-covid July 2019. Preliminary traffic, or revenue passenger miles, increased by 15.4% from July 2019 to 1.71 billion.

These results come in the wake of Q2’s display, in which Allegiant delivered its highest quarterly revenue ever. At $629.8 million, the figure amounted to a 28% increase over 2Q19’s display. Additionally, total revenue per available seat mile grew by more than 15% vs. 2Q19 although rising fuel prices and operational issues impacted the bottom-line; Adj. EPS of $0.62 not only missed the adj. EPS of $1 anticipated by Wall Street but also contracted significantly from the $3.46 delivered in the same period a year ago.

On another note, recently, the company has expanded into the resort industry. Sunseeker Resort Charlotte Harbor, Allegiant’s first Florida vacation rental property, is scheduled to debut in May 2023, and more than 1,100 room nights have already been reserved.

With many of the previous concerns abating, Raymond James analyst Savanthi Syth thinks it’s time to reassess this company’s prospects.

“In early-January, we downgraded ALGT from Strong Buy to Market Perform due to ‘mounting risks on the horizon’, particularly idiosyncratic risks related to operations (i.e., high cancellation rates), pilot cost pressure, Sunseeker capex/cost escalation, and the introduction of a second fleet type,” the analyst explained. “There are encouraging signs that operational execution has improved with cancellation rates moderating from ~7% in 1Q22 and ~4% in 2Q22 to ~1% QTD (vs. the industry average of 4%/2%/1%). Moreover, the Sunseeker capex increase has already played out and we believe the share price better reflects risks around the second fleet type.”

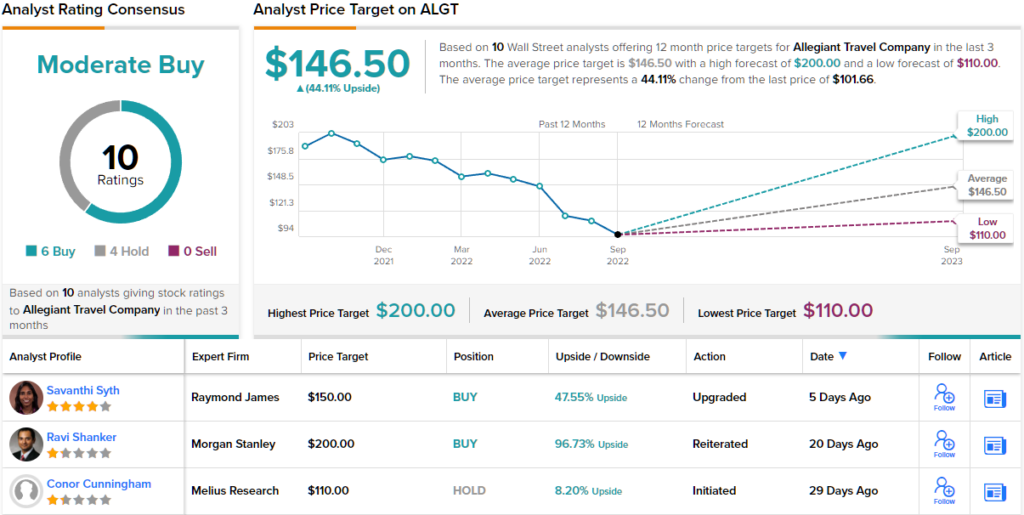

The “compelling risk reward” causes Syth to upgrade her rating from Market Perform (i.e., Hold) to Outperform (i.e., Buy) while her $150 price target suggests shares will climb ~48% higher in the year ahead. (To watch Syth’s track record, click here)

And what about the rest of the Street? The ratings show 6 to 4 in favor of Buys over Holds, making the consensus view a Moderate Buy. The forecast calls for one-year gains of 44%, given the average price target clocks in at $146.50. (See Allegiant stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.