2Q20 has been one of the trickiest quarters on record. Unprecedented coronavirus-induced headwinds have forced companies to adjust to an ever-shifting economic landscape. However, ahead of Wednesday July 29’s fiscal 3Q20 results, Deutsche Bank analyst Ross Seymore anticipates a decent showing from semiconductor heavyweight Qualcomm (QCOM).

“We anticipate a solid fiscal 3Q report from Qualcomm as a combination of recovery in China handset sales, early stages of recovery in other regions, and WFH tailwinds were sufficient to meet (or potentially slightly exceed) the company’s cautious guide which reflected a 30% reduction in handset shipments vs. prior expectations,” the 5-star analyst said.

Seymore expects the chipmaker to report revenue of $4.80 billion, roughly in-line with the consensus estimate of $4.81 billion and at the mid-point of Qualcomm’s guidance of between $4.4 to $5.2 billion.

A quarter-over-quarter decline of 40 basis points should result in PF (pro forma) gross margins of 57.2%, which along with PF opex (operating expenses) of $1.71 billion, should lead to PF EPS of $0.70 (the same as consensus and again meeting the mid-point of Qualcomm’s guidance of between $0.60 and $0.80).

Looking ahead, Seymore notes there are plenty of catalysts to look forward to.

With the 5G cycle kicking into gear, Qualcomm’s leading position in modems and “large design win ramps” including deals with Samsung, Apple and Chinese businesses position it for success. Add opportunities in 5G RF front end and a valuation “below its large-cap peers” into the mix, and you have a winning combination.

Summing up, Seymore said “With QCOM set to benefit in C2H20 from QCT share gains and seasonal uplift in QTL revs both driven in large part by Apple’s launch of new iPhones, we believe the mid/longer term tailwinds for QCOM remain strong as the company should be a significant beneficiary of 5G handset ramps from both a unit and content perspective (5G modems + RF, WiFi 6/6E).”

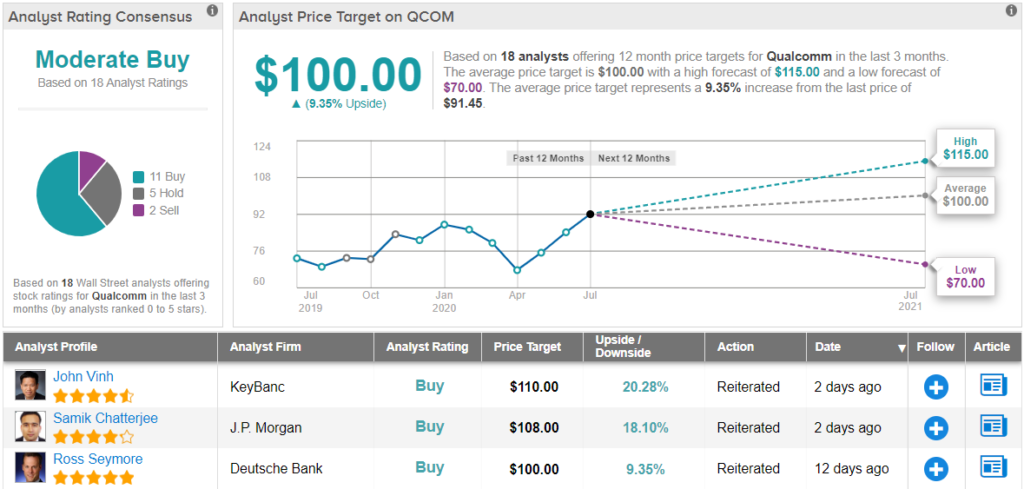

So, what’s the verdict? Seymore keeps a Buy recommendation and a $100 price target on Qualcomm, implying potential upside of 9%. (To watch Seymore’s track record, click here)

Overall, the Street’s outlook mirrors the Deutsche Bank analyst’s. Based on 11 Buys, 5 Holds and 2 Sells, Qualcomm has a Moderate Buy consensus rating. At $100, the average price target is identical to Seymore’s. (See Qualcomm stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.