Tech has been the name of the game for the past year but not all tech stalwarts have enjoyed the market spoils. Take fintech giant PayPal (PYPL), for instance. Over the past 12 months, the shares have shed 24% while the S&P 500 has recorded gains of 20%.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The drop has come as the company faces challenges in losing market share for its branded products, leading to a decline in both transaction percentage and transaction dollars.

That has left Truist analyst Andrew Jeffrey “frustrated,” although the analyst remains in PayPal’s corner, despite conceding that many investors might need more convincing to get on board again. “We are long-term bulls, based on attractive risk/reward, but acknowledge that PYPL could remain relatively range bound until branded volume and transaction $ stabilize,” the 5-star analyst explained. “That said, we still believe that PayPal still occupies an important position in the eCommerce ecosystem. This creates what we consider an asymmetric risk/ reward in which modest monetization and/or share gains could cause a disproportionate positive re-rating.”

For 2024 and 2025, Jeffrey anticipates modest yet noticeable growth in branded volume and transaction dollars. The forecast is tied to the company’s initiatives aimed at transitioning from Braintree PSP (payment service provider) volume to branded solutions. That said, Jeffrey does admit that this is a “tenuous forecast” that relies solely on discussions with the company and anecdotal evidence that a more assertive Braintree pricing model and early efforts to enhance value-added services around its PSP offering could create a “more favorable backdrop.” “We still need more evidence that this strategy is bearing fruit, and we recognize that Braintree price concessions could have their own adverse transaction % repercussions,” the analyst went on to add.

Nevertheless, Jeffrey states several reasons to back the PayPal case, including the view that eCommerce is a “structural tailwind,” and that even in the face of “competitive challenges,” PayPal’s two-sided network offers “at least” as much value to merchants as other wallets, like Apple Pay, and PSPs, like Stripe and Adyen. Moreover, the company generates plenty of FCF, and boasts a robust balance sheet. Lastly, absent “material incremental fundamental deterioration,” the stock’s “undemanding” valuation suggests an “attractive risk/reward.”

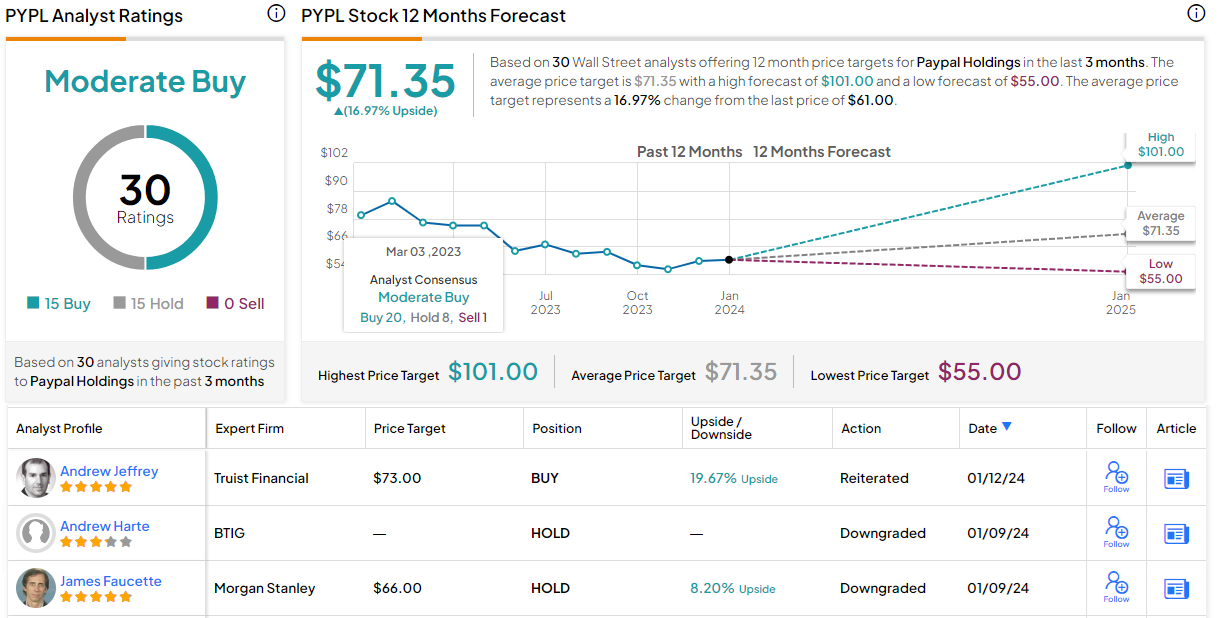

As such, Jeffrey maintained a Buy rating on the shares and raised the price target from $65 to $73, implying investors will pocket returns of 20% a year from now. (To watch Jeffrey’s track record, click here)

Views on PayPal’s prospects are split evenly on Wall Street with 15 Buys and Holds, each, resulting in a Moderate Buy consensus rating. At $71.35, the average target makes room for one-year returns of 17%. (See PayPal stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.