When it comes to the market’s wild swings, is the glass half empty or half full? Oppenheimer’s chief investment strategist John Stoltzfus is taking the latter view.

Despite the volatility that has ruled the market this year, Stoltzfus describes a situation that nevertheless still brings high potential for investors willing to shoulder the risk. He writes: “While conditions are likely to remain somewhat unstable near term we’d expect investable opportunities to surface whenever ‘babies are thrown out with the bath water.’”

Stoltzfus notes a market environment facing multiple headwinds, frequently shifting crosswise to each other, making it difficult for investors to locate and follow the main path. On the positive side, however, the strategist believes that the Federal Reserve will likely play a calming role, and not just to due to its anti-inflationary policy switch.

“Federal Reserve hike cycles are never easy to navigate but the Bernanke legacy created a highly sensitive and communicative Fed, which could prove helpful… A Fed that can pivot and ‘pump the brakes’ rather than ‘slam on the brakes’ is a good thing in our view,” Stoltzfus added.

Turning Stoltzfus’ outlook into tangible recommendations, Oppenheimer 5-star analysts are pounding the table on two stocks, with these pros seeing over 50% upside potential in store. Using TipRanks’ database, we learned that the rest of the Street is in agreement, as both boast a “Strong Buy” analyst consensus.

QualTek Services (QTEK)

The telecom world is roiling as 5G is rolling out. The new tech promises a series of advantages, including faster download speeds and lower latency, but it also offers plenty of challengers to providers. 5G will require new wired and wireless networks, new towers and hardware, new power linkages. This is where QualTek steps in. The company offers turnkey solutions to the infrastructure issues that the 5G rollout is facing, in networking, in telecom, and in renewable energy.

The company has been in the wireless solution infrastructure business since 2012, but it is new to the public markets. The QTEK ticker made its first appearance on the NASDAQ on February 16 of this year, through a business combination with the SPAC firm Roth CH Acquisition III. The merger has brought approximately $225 million in new capital to QualTek. However, since the ticker started trading, it has fallen 67%.

Just six weeks after the company entered the public stock markets, QualTek released its first earnings report as a public firm. At the top line, Q4 revenue came in at $147.1 million, up 11% year-over-year. The company ran a net loss in the quarter – but investors should note the work backlog, a key indicator of future business. As of the end of December, QualTek had a $2.1 billion order backlog, up 22% y/y. The backlog reflects the real need within QualTek’s customer base to get 5G infrastructure online.

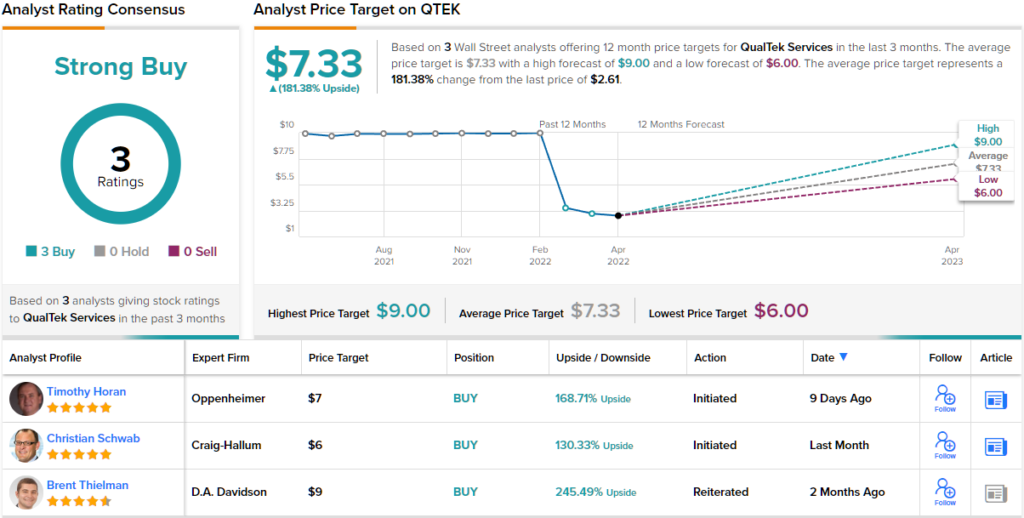

This stock has caught the eye of Timothy Horan, one of Oppenheimer’s 5-star analysts – and rated in the top 3% of all of Wall Street’s stock pros. Horan writes of QualTek: “While acknowledging that the stock is highly speculative and will likely continue to be volatile due to its low price, limited float, and excess leverage (currently 80% of firm value), our positive recommendation on QualTek sees a favorable risk/reward in the company’s attractive double-digit growth prospects coupled with a relatively undervalued stock that trades at a steep 35% FV/EBITDA discount to peers, making it a compelling play on the most significant network upgrade cycle since the first Dot.com bubble in the late 1990s.”

“We believe that with the stock down ~70% since February 14 de-SPAC and our conservative estimates providing downside flexibility, QTEK stock is a spring-loaded hidden jewel,” Horan added.

These bullish comments support Horan’s Outperform (i.e. Buy) rating, and his $7 price target indicates room for ~169% growth over the year ahead. (To watch Horan’s track record, click here)

Overall, QTEK has picked up 3 analyst reviews since the SPAC merger. They all agree that it’s a Buy, making the consensus view on the Street a unanimous Strong Buy. The shares are selling for $2.60 and have a $7.33 average price target, for an upside potential of 181%. (See QTEK stock forecast on TipRanks)

Zeta Global Holdings (ZETA)

For the second stock on our list, we’ll look at Zeta Global Holdings, a marketing tech firm offering customers a cloud-based AI data analytics engine for customer acquisition and retention. This New York-based firm boasts of having the largest ‘opted-in’ dataset in omnichannel consumer marketing, with more than 235 million US individuals opted in to the database. Zeta uses its platform to sort through the data generated by these and other sources, totaling approximately 2.5 billion consumer profiles.

This is another company that went public recently – Zeta’s ticker has only been trading since June of last year. In that time, the company has recorded solid growth, including 25% year-over-year revenue growth for 2021, up from 20% growth in the prior year. ZETA shares have appreciated, too. The stock is up 44% from its first-day’s close.

In its most recent quarter, 4Q21, Zeta showed a top line of $135 million, up from $115 million in 3Q21, and up 18% y/y. The company generated a quarterly cash flow of $20.9 million from operations, almost half of 2021’s total cash flow of $44.3 million. Zeta’s growth was powered by its direct platform revenue, which made up 77% of the revenue total, compared to 60% in 4Q20.

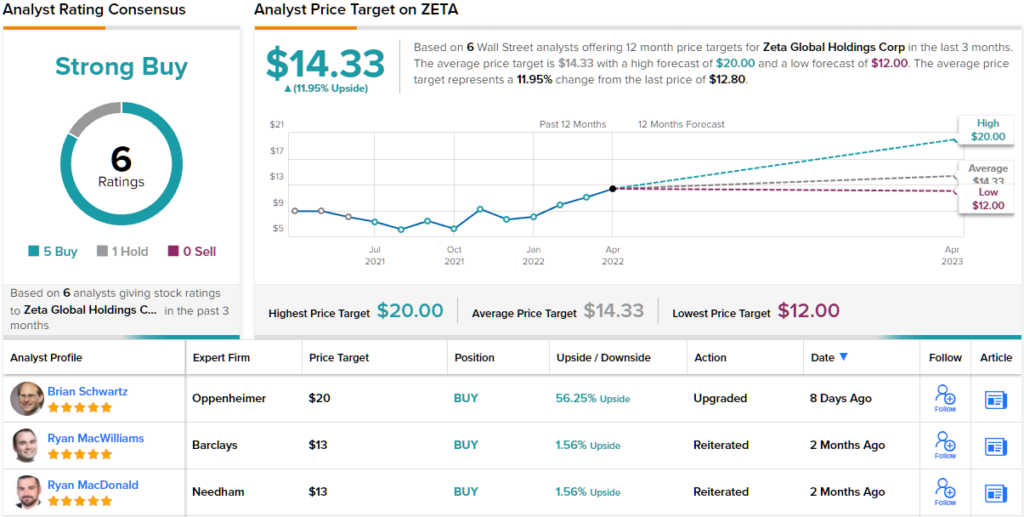

Growth of this magnitude is sure to get some serious notice – and it has piqued the interest of Brian Schwartz, another of Oppenheimer’s top analysts. Schwartz, who is rated #25 overall by TipRanks.

“We see substantial upside from current prices based on valuation, improving fundamentals, and transparency… Zeta looks well-positioned to take advantage of the growth market, given its best-of-breed ZMP platform and large CDP. Marketing companies that boast modern SaaS platforms with first-party behavioral-intent data, like Zeta’s, should outperform legacy marketing software rivals over the next several years because privacy-tracking changes and modern architecture give them competitive advantages in marginal cost and attribution,” Schwartz opined.

It should come as no surprise, then, that Schwartz rates ZETA a Buy. His price target is set at $20, indicating confidence in a 56% one-year upside. (To watch Schwartz’s track record, click here)

That the Oppenheimer view is no outlier is clear from the analyst consensus on ZETA – the stock has 6 reviews, including 5 Buys and just 1 Hold, for a Strong Buy consensus. The stock’s average price target of $14.33 points toward ~12% upside from the trading price of $12.80. (See ZETA stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.