After a shaky August for the markets, we have now entered the year’s final third and the bad news is that, going by the history books, September represents the market’s worst month of the year.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The good news, however, is that according to Oppenheimer’s head of technical analysis, Ari Wald, any anticipated lull will be short-lived.

“The key takeaway in our work is that, whether or not the advance is resuming imminently, it should only be a matter of time,” Wald recently said. “The Russell 2000’s ability to uphold its 200-day average, combined with risk-on leadership and bullish inter-market checks, reinforces our view that a seasonal correction should prove temporary and an opportunity to buy into a middle-innings bull cycle.”

So, what should investors be buying ahead of the bull market’s eventual resumption? At Oppenheimer, the stock analysts have some answers to that question, and they have tapped two equities with the potential to double in value over the next 12 months.

Are other Street analysts just as confident? It looks like it. According to the TipRanks database, both stocks are rated as Strong Buys by the analyst consensus, who also see triple-digit gains on the horizon. So, let’s see why the financial prognosticators except these shares to jump big time.

Zura Bio (ZURA)

First up is Zura Bio, a clinical-stage biopharmaceutical firm researching and developing new drugs with a focus on immunology. More specifically, the company has a line-up of new drug candidates, each at or entering Phase 2 clinical trials, targeting a variety of autoimmune disorders. The drug candidates are each designed to follow a different path toward combatting auto-immune disease, providing relief for patients with these difficult conditions.

In June of this year, Zura made two announcements which should interest investors. The first, from June 6, concerns ZB-106 (tibulizumab), a drug candidate licensed from Eli Lilly earlier this year with potential as a first-in-class medication with dual action as an anti-il-17 and anta-BAFF antagonist. The company reported completion of an $80 million private placement financing round, that guaranteed the drug would advance to Phase 2 in the clinic. The drug candidate is scheduled to enter Phase 2 testing against systemic sclerosis and hidradenitis suppurativa during the second half of next year; it has already passed tolerability testing in healthy volunteers.

Also of interest, on June 23, Zura joined both the Russell 3000 and Russell 2000 stock indexes. These indexes aim to capture a broader, more accurate, view of the US stock markets, by including more of the small- and mid-sized public firms and reducing the dependence on the market’s mega-cap stocks as a gauge of performance.

Directing our attention back to Zura’s clinical pipeline, ZB-880, or torudokimab, emerges as a promising Phase 2 candidate for asthma treatment. The drug candidate is a high affinity monoclonal antibody that targets IL33 for neutralization; it has already shown an acceptable tolerability profile in earlier stage clinical trials. Per the 2Q23 update, the company is preparing to initiate the Phase 2 clinical trial next year.

Also in the clinic is ZB-168, a fully human, anti-IL7Rα monoclonal antibody under study as a treatment for several conditions including ulcerative colitis and atopic dermatitis. The drug is active against the IL7 and TSLP immune pathways. Zura plans to initiate Phase 2 trials of this drug next year. The company holds an exclusive, worldwide, license for the development, and the eventual commercialization, of ZB-168 in all indications.

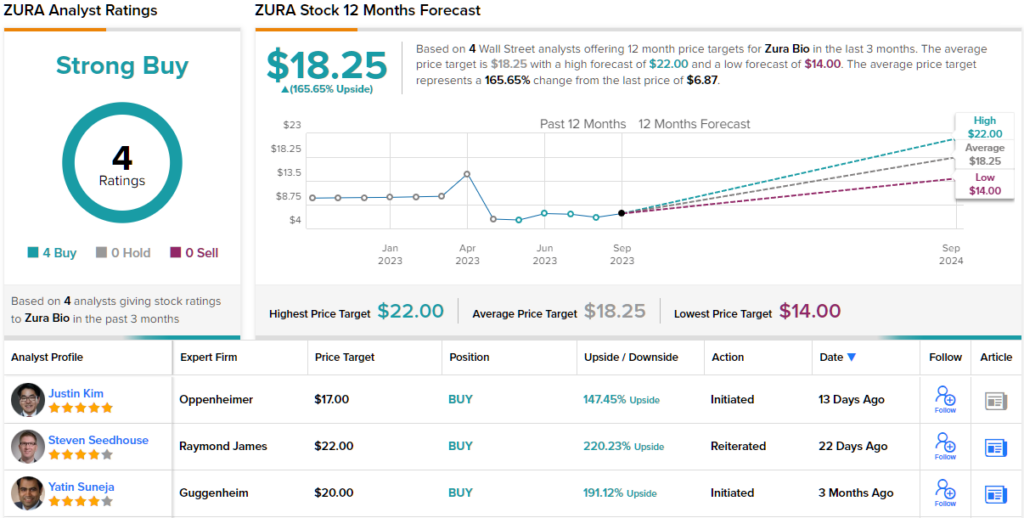

The ZB-106 track, particularly, caught the attention of Oppenheimer’s Justin Kim. The 5-star analyst writes of this candidate and the stock, “With a focus on Phase 2-ready asset ZB-106, aka tibulizumab (an anti-BAFF/IL-17 dual-antagonist), we are intrigued by this asset’s potential to uniquely address HS, where the market opportunity for next generation IL-17 therapies is continuing to be better appreciated by the Street, and systemic sclerosis, where the anti-BAFF activity of the drug could provide clinical benefit where significant unmet need exists. We note the story for Zura and ZB-106 is at an early stage, but believe the upside could well match the long-term risk-reward. We are bullish.”

Kim goes on to rate ZURA shares as Outperform (i.e. Buy), and he sets a 12-month price target of $17, indicating his confidence in a robust 147% upside potential. (To watch Kim’s track record, click here)

Kim is hardly the only bullish analyst on Zura – the stock has a unanimous Strong Buy consensus rating based on 4 recent positive analyst reviews. The shares are trading for $6.87, and their $18.25 average price target implies a one-year potential gain of ~166%. (See ZURA stock forecast)

Crinetics Pharmaceuticals (CRNX)

The endocrine system is one of our most important bodily systems, comprising glands and hormones that regulate the body’s growth and functions. Endocrine diseases can be some of the most dangerous, and some of the most difficult to treat. Crinetics Pharmaceuticals, the second stock we’ll look at here, focuses on these diseases, particularly the more rare endocrine diseases. The company is working on therapies to provide patients with effective disease control.

Pursuing this end, Crinetics has developed a varied pipeline, featuring both clinical-stage drug candidates and pre-clinical research programs. The endocrine conditions targeted are equally varied, and include well-known names such as diabetes and thyroid eye disease, as well as lesser-known conditions such as acromegaly and carcinoid syndrome. The latter two are the subjects of Crinetics’ most advanced clinical trial studies.

These clinical trials focus on the drug candidate paltusotine (CRN00808). The company currently has three trials of paltusotine ongoing, including the Phase 3 PATHFNDR-1 and -2 trials of the drug in the treatment of acromegaly and a Phase 2 trial in the treatment of carcinoid syndrome. Paltusotine belongs to a new class of orally-dosed, selective, non-peptide somatostatin receptor type 2 (SST2) agonists and shows high promise in the treatment of acromegaly.

On the acromegaly track, Crinetics is expected to release topline data from the Phase 3 PATHFNDR-1 study this month. The study is a placebo-controlled trial of orally dosed paltusotine in patients switching from standard-of-care peptide depots.

During Q2 of this year, Crinetics completed enrollment in the PATHFNDR-2 trial, another placebo-controlled Phase 3 study of oral paltusotine. Topline data from this study is anticipated for 1Q24.

Following up on these studies, Crinetics plans to submit its new drug application (NDA) to the FDA regulatory agency next year. The company is seeking regulatory approval of the drug for both treatment and maintenance of treatment in acromegaly.

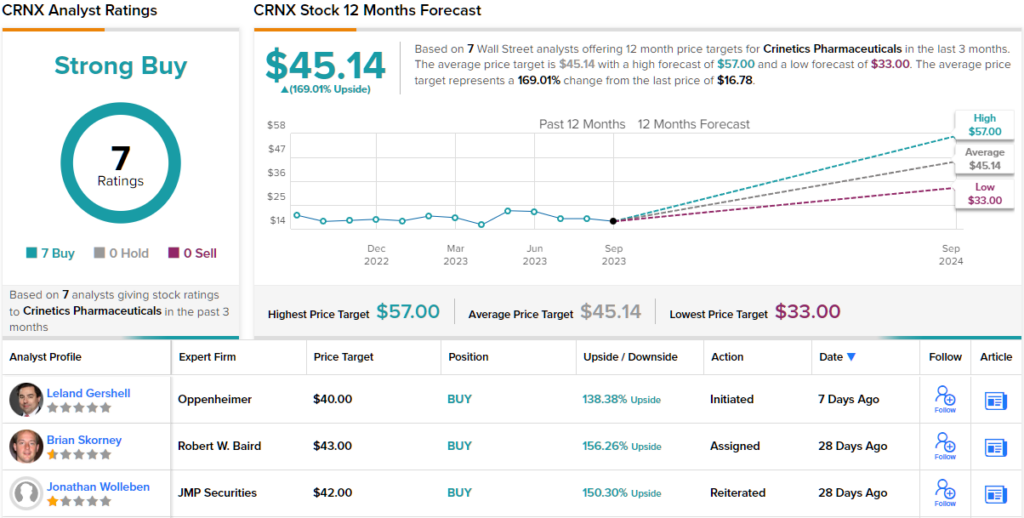

The acromegaly track, and the high potential of paltusotine for success, attracted Oppenheimer’s Leland Gershell to this stock. The analyst writes in a recent note, “We anticipate positive upcoming news flow around lead candidate paltusotine’s opportunity to treat acromegaly, which we see as the main value driver for the stock in the near term. We believe paltusotine is likely to succeed in both of its Phase 3 trials in this indication, with the first to report in September and the second in 1Q24, which together should pave the way to US and EU approvals and launches by CRNX in 2025 and 2026, respectively. We expect its distinct advantages over the standard of care to enable paltusotine to take substantial market share and project peak revenue of $250M.”

Quantifying his position on Crinetics, Gershell gives the stock an Outperform (i.e. Buy) rating with a $40 price target pointing toward a strong 138% upside on the one-year horizon. (To watch Gershell’s track record, click here)

Once again, we’re looking at a stock with a Strong Buy consensus rating, and once again where the bullish take is unanimous – Crinetics has 7 recent positive analyst reviews on file. The stock’s trading price of $16.78 and average price target of $45.14 combine to suggest an upside of 169% for the year ahead. (See CRNX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.