With expectations close to historic lows, Video-streaming giant Netflix (NFLX) is starting to regain its footing. I’d argue that there’s a lot to gain by giving the ailing streamer the benefit of the doubt as it moves into uncharted waters with ads. At this juncture, I think too much damage has been done to the former FAANG staple. I remain bullish as CEO Reed Hastings looks to turn the tide.

Netflix stock saw a strong rally off its recent low of around $169 and change per share. Powered by the latest round of better-than-feared earnings results and numerous strategic moves to help offset recent weakness (freeloader crackdown, move into video gaming, and addition of an ad-based tier), Netflix has shown signs that it’s more than willing to evolve with the times.

Netflix Sheds Nearly a Million Subscribers; Shares Rally Anyway

By no means did Netflix turn the ship around in its second quarter. However, the bar was set incredibly low going into the quarter, with expectations of 2 million net subscriber losses. When Netflix clocked in net subscriber losses of 0.9 million, the stock rallied with a fury.

With various strategic efforts in place, Netflix hopes to ease the subscriber bleed as we head into a recession. It’s been tough for analysts to model how the ad-based tier will affect the firm’s sales growth moving forward. Undoubtedly, such uncertainty has led many to err on the side of caution with their financial model inputs.

Further, the effort to get password sharers to pay up also introduces a major question mark. Netflix is trailing its crackdown on non-paying users in South America.

The real risk from the effort is if paying users will cut subscriptions if they’re disallowed from sharing with close friends and family. Arguably, such a move could exacerbate subscriber losses as the company looks to squeeze out an extra profit.

Content is King for Streamers

An ad-based tier of Netflix doesn’t appear to be a game-changer since many streaming rivals are likely to follow suit. Further, the freeloader crackdown seems to pose more risk than reward. A major differentiating factor for streamers, I believe, is content. Not content-recommending algorithms, social-media-like feeds, or user experience design changes.

As rivals ramp up content spending, Netflix may need to continue spending billions of resources on video and gaming content creation. Fortunately, Netflix is picking up momentum with its exclusive mobile-gaming business, which may be able to offer a better return on investment over the longer run. With plans to add hundreds of titles over the next year or so, Netflix may be able to add a bit of “stickiness” to its subscription.

Further, with the metaverse on the horizon, I’d look for Netflix to start leveraging its powerful brands (think Stranger Things, Squid Game, and Black Mirror) in the fields of VR or AR.

Recently, Netflix teamed up with Immersive Gamebox to launch a “Squid Game” experience. The immersive experience incorporates physical touch screens and other intriguing technologies that don’t include VR headsets. Such an exciting experience would probably translate over very well in VR. Who wouldn’t want to play a game of “red light, green light” without the deadly risks?

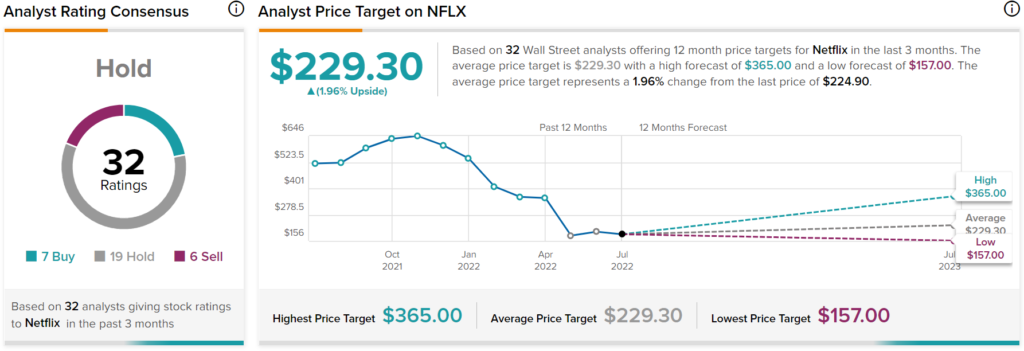

Wall Street’s Take on NFLX

Turning to Wall Street, NFLX has a Hold consensus rating based on seven Buys, 19 Holds, and six Sells assigned in the past three months. The average NFLX price target of $229.30 implies 2% upside potential. Analyst price targets range from a low of $157.00 per share to a high of $365.00 per share.

The Bottom Line: Netflix Can Turn Things Around

Netflix found itself between a rock and a hard place in the first half. With a lowered bar, strategic initiatives incoming, and new games on the way, the firm may have what it takes to reverse the trend.

Undoubtedly, M&A is an arena that could make Netflix more appealing in the eyes of investors. The company has been relatively quiet on the acquisition front over the past few years. This could change as valuations become more attractive across the market.

Personally, I think Netflix should buy a video-game company rather than participate in the consolidation of the media industry. The gaming industry is growing incredibly fast and could help Netflix smoothen its transition into the metaverse.