Last year was brutal for most investors, there’s just no way around that. The S&P 500 index fell 19% through the year, battered by a series of headwinds including stubbornly high inflation, the Federal Reserve’s switch to monetary tightening, supply chains that just wouldn’t unsnarl, China’s long-lasting lockdown policies, Russia’s war in Ukraine… the list was long.

But losses on this scale bring opportunities with them, in the form of lower share prices. The stock analysts at Morgan Stanley haven’t been shying away from that basic market truth, and among their picks are some fundamentally sound stocks that had recorded steep share price losses in 2022.

We’ve used the TipRanks platform to pull up the details on two of these picks; Morgan Stanley’s analysts see more than 50% upside ahead for both of them, so let’s take a closer look now.

Lifestance Health Group (LFST)

We’ll start with Lifestance Health Group, a company founded just 5 years ago that has quickly taken a leading position in the mental health provider field. Lifestance offers a wide range of both in-person and virtual outpatient mental health care services for adults, adolescents, and children, through some 600 centers across 32 states. The company boasts a staff of more than 5,400 psychologists and therapists, advanced practice nurses, and psychiatrists.

As a healthcare segment, mental health has a steadily growing profile. The social stigma long accorded to these issues has begun to recede, and patients are more willing, and more likely, to seek treatment. This is the underlying fact that has brought Lifestance a steady run of sequential revenue gains – modest, though real – since going public in the summer of 2021. In the most recent reported quarter, 3Q22, the company reported a total of $217.6 million at the top line, a gain of 25%, or $43.8 million, year-over-year.

There were improvements at the bottom line, too. Lifestance had a net loss of $37.9 million in the quarter, compared to a loss of $120.5 million in the prior-year period. The 3Q22 loss was attributed mainly to a ‘stock-based compensation expense’ totaling $34.9 million. On a positive note, the company reported an adjusted EBITDA of $15.4 million, up 43% y/y.

On the balance sheet, Lifestance saw $5.7 million in cash flow from operations in Q3, for a total of $16.9 million in the nine months through September 30, 2022. As of that date, the company had $90.3 million in cash assets, and a net long-term debt of $212 million.

The key point for investors in the last earnings report was the guidance, which came in below analyst expectations. The company predicted Q4 revenue between $215 million and $220 million, missing the forecast by 8%. Shares have fallen 30% since then.

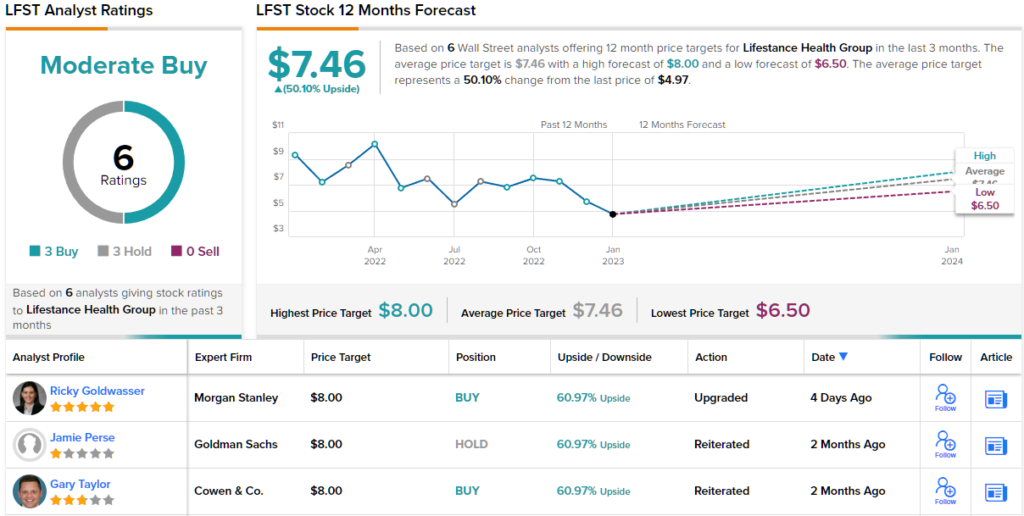

However, Morgan Stanley’s 5-star analyst Ricky Goldwasser recently upgraded her rating on the stock from Equal-weight (i.e. Neutral) to Overweight (i.e. Buy). Backing this stance, Goldwasser points out the company’s new management, and its plans for improving clinician retention and productivity.

“LifeStance has begun to address clinician feedback, with a goal of improving net clinician growth and productivity. New initiatives include: adding front-line resource to attract and retain talent, building a new call center to address patient billing and reducing credentialing timelines. The company is also beginning to leverage technology to improve patient funnel conversion. Notably, its online booking and intake experience (OBIE) platform has been rolled out in 14 states and is expected to be live across all 32 states by the end of Q2’23,” Goldwasser opined.

“Of note,” the analyst added, “if LifeStance were to improve clinician retention from 80% today to the pre-IPO level of 87%, it could add more than $30mn in annual revenue, or 3% to our estimate in 2024.”

Along with her Overweight rating here, Goldwasser gives LFST shares a price target of $8, suggesting a one-year upside potential of 61% for the stock. (To watch Goldwasser’s track record, click here)

Overall, there are 6 recent analyst reviews for LFST stock, and they show an even split: 3 Buys and 3 Holds, for a Moderate Buy consensus rating. The stock is trading for $4.98 and has an average price target of $7.46, implying an upside of 50% in the next 12 months. (See LFST stock forecast on TipRanks)

Definitive Healthcare Corporation (DH)

Next up is Definitive Healthcare, a software and data analytics company whose customer base includes physicians, payers, hospitals, and consultants on the provider side of the industry. Definitive offers a data platform on the SaaS model, giving users capabilities to collect, collate, understand, and navigate the information in the healthcare market. Definitive calls its product healthcare commercial intelligence, and boasts that it is used by more than 2.5 million physicians and other practitioners, and by more than 9,300 hospitals, nationwide.

In recent years, the evident advantages that data analysis brings to businesses of all sorts have turned the field into a big business in its own right. Definitive has ridden that wave to success, and since its September 2021 IPO, the company has seen rising trends in both revenues and earnings. The last set of financial results that Definitive released were for 3Q22, and showed a 33% year-over-year increase at the top line, to $57.4 million. Over the same period, the company’s adjusted earnings per share grew from just 1 cent to 6 cents. Not only did EPS show strong y/y growth, it also came above the 5-cent estimate.

Definitive’s business has delivered plenty of cash, too. The unlevered free cash flow in the third quarter came to $15.5 million, an impressive 27% of revenues.

The stock, though, was unable to withstand 2022’s bear conditions and shed 60% of its value over the course of the year.

That said, looking ahead, Morgan Stanley’s Craig Hettenbach sees plenty to like about DH. The 5-star analyst writes: “While macro pressures are having a greater than expected impact on growth heading into 2023, Definitive is managing the business well and we expect the company to sustain best in class profitability. It’s early innings for the adoption of analytics in healthcare and Definitive is off to a strong head start, leveraging its primary data sources and AI engine to greatly enhance the sales efforts of customers. With less than 3% customer penetration and a TAM of $10bn, we see a long runway for growth.”

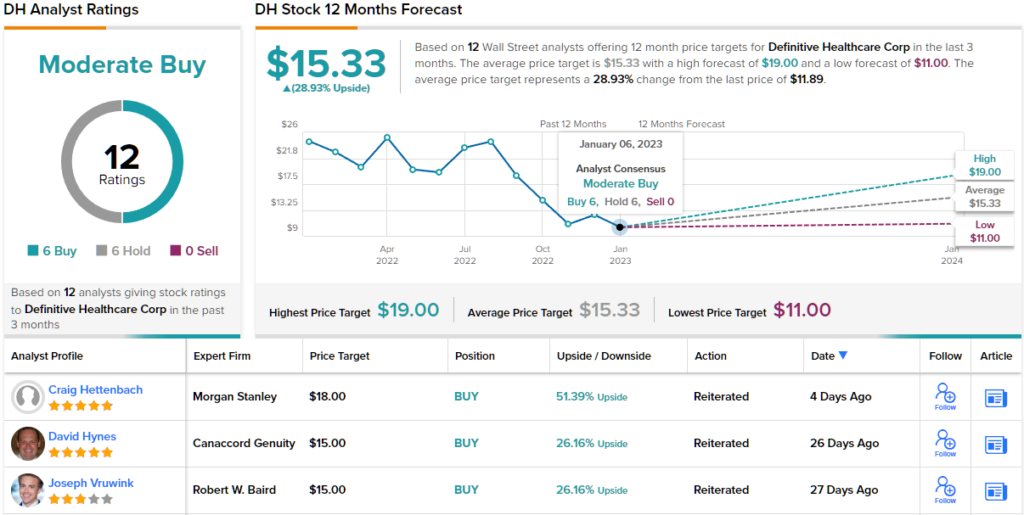

Looking forward from this position, Hettenbach rates DH shares an Overweight (i.e. Buy), with an $18 price target to indicate a one-year potential gain of 51%. (To watch Hettenbach’s track record, click here)

We’re looking here at another stock with an even split among the analyst reviews; the 12 recent reviews go 6 to 6 for Buys and Holds, giving the shares their Moderate Buy consensus rating. DH is selling for $11.91, and its $15.33 average price target suggests it has ~29% upside ahead of it this year. (See DH stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.