A trio of headwinds are buffeting the markets, making investors skittish. Stealing the headlines is the Russia-Ukraine situation. Foreign policy pundits are openly speculating on the prospect of war, in the event that Russia invades its neighbor and the US objects. For now, that situation is fluid and unpredictable.

On the domestic front, stubbornly high inflation remains a problem – and it’s continuing to rise. Market watchers are expecting the Federal Reserve to raise interest rates at least 3 times this year, perhaps by as much as 50 basis each time. While high by recent standards, that would still keep rates historically low, and so may or may not curb inflation.

In the meantime, the 4Q21 earnings have been largely positive, with aggregate year-over-year gains near 15% and some three quarters of companies reporting results above expectations.

The overall result, for the stock market, has been some 6 weeks of increased volatility to start off 2022. It raises the question, ‘How do you find the next hot stock to buy in this environment?’ One way might be to screen for stocks that have been endorsed by analysts at major investment banks in particular, such as Wall Street banking giant Morgan Stanley.

The firm’s stock analysts are showing their upbeat outlook by selecting the stocks they see as winners for the coming year – and winners with substantial upside, on the order of 90% or better. Using the TipRanks database, we’ve looked up two of these Morgan Stanley picks, to see what makes them stand out.

Safehold (SAFE)

We’ll start with Safehold, a pioneer in the ground lease segment of the real estate investment trust sector. Ground leases are way for landowners to ‘unlock value,’ by permitting long-term tenants to build on and make improvements to land holdings, with the stipulation that all such development will revert to the property owner when the lease ends. The company offers long-term ground leases, for up to 99 years. Safehold has a $4.5 billion portfolio of such ground lease properties.

That portfolio brought the company $47 million in revenue in 3Q21, the last reported, for a 24% year-over-year gain, and the fifth quarter in a row of sequential gains. EPS came in at 38 cents, beating the forecast by 8.5% and growing 35% yoy.

Safehold has properties across the US, but in recent weeks has been moving to expand its footprint in the South and Southwest. The company on February 10 closed a ground lease in the Nashville area that will capitalize a $128.4 million multifamily development – and that marks the company’s fourth major ground lease in the Nashville area. On February 11, Safehold closed its third ground lease in Phoenix, Arizona, for $54 million. That property will be developed as student housing for Arizona State.

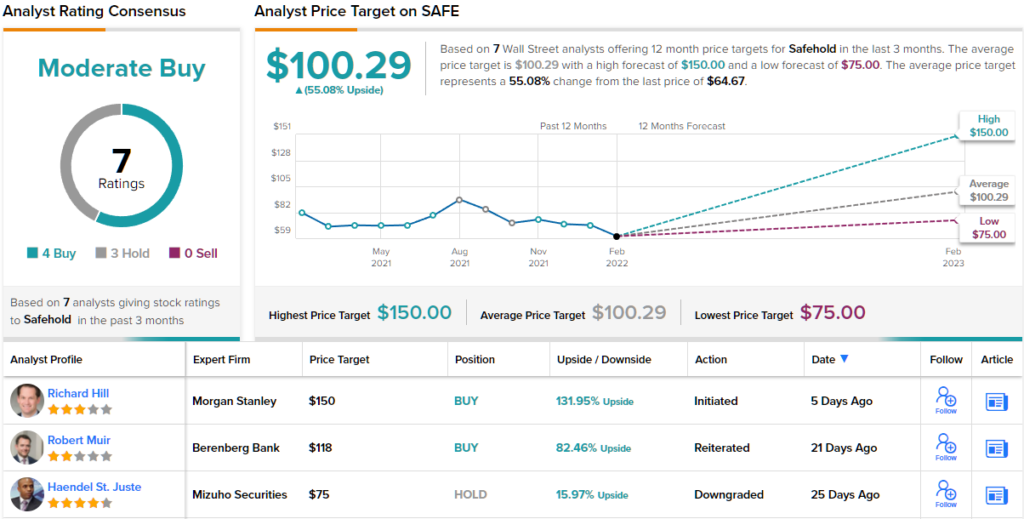

Despite the positive developments, Safehold’s stock has been falling, and is down 18% year-to-date. However, according to Morgan Stanley analyst Richard Hill, the selloff in SAFE is unwarranted.

“Our work indicates SAFE shares are significantly undervalued… The market fails to recognize SAFE’s growth potential, reflected in 2021 underperformance as growth outperformed and a challenging start to ’22 as bond proxies underperform given a sharp rise in rates. The company is targeting aggressive growth… SAFE laid out a growth target in 4Q20 to double the size of their portfolio to $6.4bn by the end of 2023. Over the longer term, internal growth can contribute significantly to value: its leases yield 3% and typically have 2% annual rent bumps with periodic CPI look-back adjustments capped between 3.0-3.5% to mitigate inflation,” Hill explained.

Hill’s comments back up his Overweight (i.e. Buy) rating, and his $150 price target indicates potential for ~132% share appreciation in the next 12 months. (To watch Hill’s track record, click here)

Overall, Safehold has a Moderate Buy rating from the analyst consensus, with 4 Buys and 3 Holds set in recent weeks. The stock is selling for $64.67, and at $100.29 the average price target suggests 55% upside potential. (See SAFE stock analysis on TipRanks)

New Relic (NEWR)

Next up, New Relic, is a tech company from Silicon Valley. New Relic offers cloud-based software solutions for monitoring, debugging, and improving app stacks. Data analytics is an urgent and growing need in the digital world, and New Relic combines it with troubleshooting and optimization for an efficient package to meet customer needs.

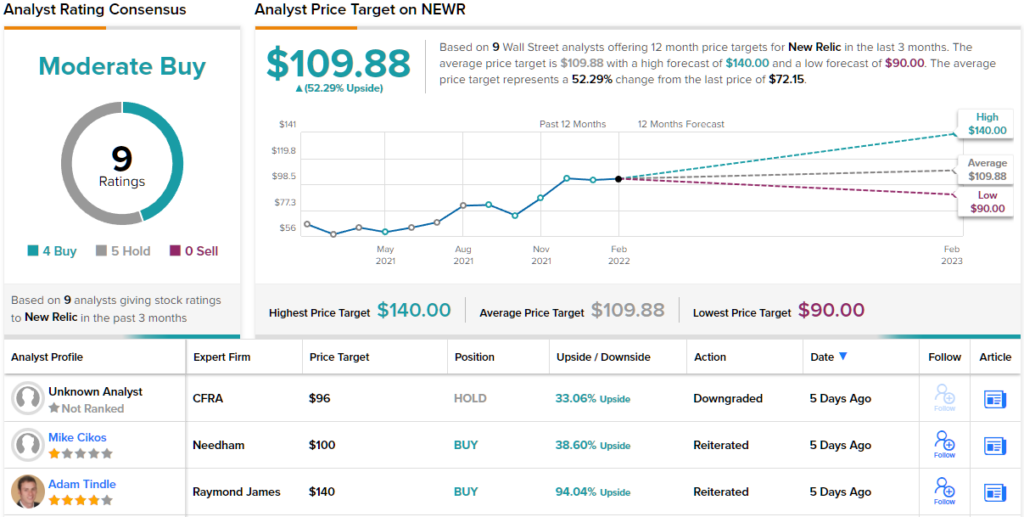

This company has seen increasing revenues – the top line has increased sequentially every quarter for over two years now – but also saw a sudden drop in share value after the last earnings report. For fiscal 3Q22, New Relic reported $203.6 million at the top line, up 22% year-over-year. On a negative note, the company issued fiscal fourth-quarter guidance that represent a slowdown from recent quarters. For fiscal Q4, the company is predicting revenue growth of 18% to 19%, while for the full year of fiscal 2022, management sees a yoy revenue improvement of 17% to 18%.

In his coverage of this stock for Morgan Stanely, analyst Sanjit Singh sees the investor worries as overblown. He writes, “We think there are multiple factors explaining the conservative guide including a lack of detailed understanding of consumption behavior for customer cohorts switching to the new pricing model given a lack of history. In addition, the benefits from the significant improvement in churn over the last few quarters are beginning to fade. Finally, data consumption growth at the end of December slowed and persisted into January likely due to seasonal reasons…”

“Bigger picture, we think the resumption in new customer growth combined with the fact that customers on the new model are signing up for a materially higher level of commitments upon renewal suggest that New Relic’s business is getting better and that our revenue acceleration and improving margin thesis is intact,” the analyst summed up.

To this end, Singh rates NEWR shares an Overweight (i.e. Buy), and sets a $138 price target that suggests an upside of ~91% for the 12 months ahead. (To watch Singh’s track record, click here)

Overall, New Relic has picked up 9 recent analyst reviews, and those include 4 to Buy and 5 to Hold, for a Moderate Buy consensus. The average price target here is $109.88, indicating a 52% upside from the current trading price of $72.15. (See NEWR stock analysis on TipRanks)

Affirm Holdings (AFRM)

The last stock on Morgan Stanley’s radar is Affirm Holdings, a fintech company that faces the customer. Affirm is working on the next generation of digital and mobile commerce apps, specifically an app to facilitate consumer credit through installment loans approved at the point of purchase. The upshot to this is, Affirm’s customers can access credit when they need it, for the amounts they need, and rates they can afford, with payment schedules they determine. It’s a flexible system, designed to facilitate commerce. Affirm has applications in online retail, and even has partnerships with Walmart for on-site use.

Since going public last year, Affirm has shown an increase in revenue for every reported quarter. The most recent, for fiscal 2Q22, showed total revenue of $361 million, easily beating the forecast and growing 76% year-over-year. The top line gain was driven by three major metrics: a vast yoy increase in active merchants, from 8,000 to 168,000; a 150% increase in active consumers, to 11.2 million; and a 15% increase in the transaction per active consumer.

At the same time, the company’s net loss per share widened yoy from 38 cents to 57 cents – and even worse, that increased loss occurred while investors had expected it to narrow slightly, to 34 cents per share. That was the key point for investors, and the stock fell heavily after the report.

However, Morgan Stanley’s James Faucette, rated 5 stars by TipRanks, has been covering Affirm, and he remains bullish on the stock. Faucette isn’t too worried about the specific numbers in the quarterly reports; he writes, “We think that the most important success factors at this stage are customer acquisition, increasing frequency of use, building acceptance network to assure that cycle continues, and navigating economic and credit cycles well enough to assure that those efforts aren’t derailed. So far, so good… The key metrics we track as an indicator of credit performance all showed positive development.”

In line with these comments, Faucette rates the stock an Overweight (i.e. Buy), with a $140 price target to indicate a robust 212% one-year upside. (To watch Faucette’s track record, click here)

For now, AFRM has a Moderate Buy analyst consensus rating, based on 14 reviews that include 8 Buys, 5 Holds and a single Sell. The stock is trading for $44.62 and has an average price target of $84, for an 87% upside prediction by year’s end. (See AFRM stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.