Micron (MU) shares might have gained 13% on a year-to-date basis but zoom out and the stock is still down by 30% over the past year.

With the shares trading just slightly “above book,” Rosenblatt Securities analyst Hans Mosesmann believes the depressed valuation is a reflection of a “dismal cyclical bottoming process” although the analyst says there are “early signs of bit ‘demand’ stabilizing and channel inventories normalizing.”

Nevertheless, with the memory giant slated to report fiscal second quarter (February quarter) results next week (Tuesday, March 28th), Mosesmann has low expectations, anticipating “continued ASP pressure in DRAM and NAND, and for the May quarter outlook (as effectively pre-announced at a recent investor conference) to see q/q flat-to-down sales and earnings pressure on a large inventory write down.”

Mosesmann expects the company will deliver revenues of ~$3.8 billion, compared to consensus at $3.74 billion, representing a quarter-over-quarter drop of 7% and 8.6%, respectively. Gross margins are expected to reach ~8.5%, a decline from the 22.9% on display in the November quarter. This leads to Mosemann’s call for non-GAAP EPS of ($0.62), against the Street’s ($0.78) estimate.

For the May quarter guide, Mosesmann is expecting revenues of $4.16 billion – consensus has $3.9 billion. On the bottom-line, the 5-star analyst’s model calls for non-GAAP EPS of ($0.61) vs. the Street’s ($0.81).

While the near-term appears challenging, looking further ahead, Mosesmann thinks the second half of the year could see a shift in sentiment. “Unprecedented industry memory/storage capacity reductions/push-outs that started out last summer/fall we see as leading to a back half of 2023 of S/D balancing as the industry transitions to DDR5 DRAM (no inventory problem here), and as AI memory-centric compute platforms start to inflect,” he explained.

With the analyst expecting downward revisions in the wake of next week’s print, he likes the risk/reward on offer for MU shares right now. Accordingly, Mosesmann reiterated a Buy rating on the stock, while his Street-high $100 price target makes room for 12-month gains of 77%. (To watch Mosesmann’s track record, click here)

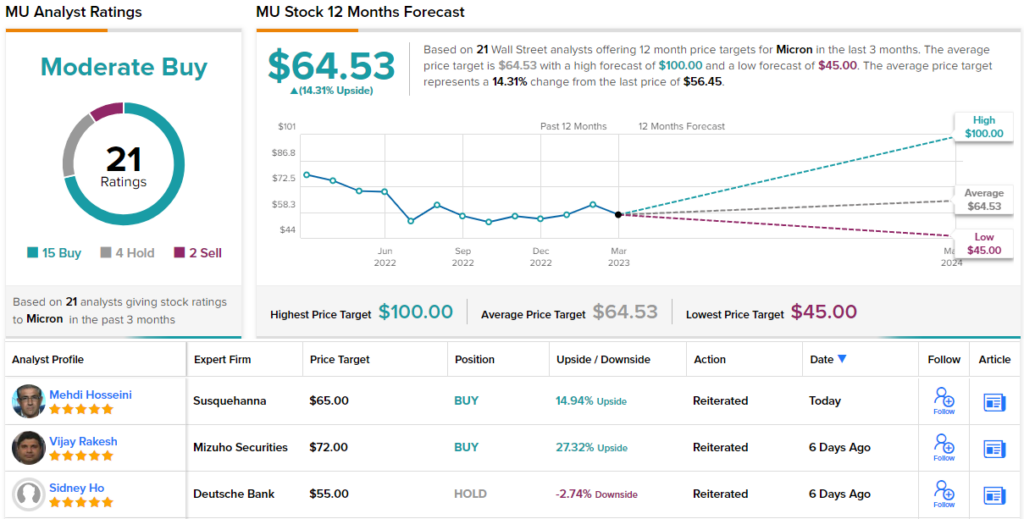

21 analysts have waded in with MU reviews over the past 3 months, and these break down into 15 Buys, 4 Holds and 2 Sells, all culminating in a Moderate Buy consensus rating. The forecast calls for one-year returns of 14%, considering the average target clocks in at $64.53. (See Micron stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.