Financial research firm Tigress financial released a bombshell with its bullish analysis on Meta Platforms (META), stating that the stock might surge to $466, which implies an increase of 195%.

According to Tigress, Meta “remains well-positioned to benefit from the evolution of social commerce, commercial aspects, and future monetization potential of the Metaverse.”

Tigress’ analysis provides a valuable juxtaposition to Needham’s Laura Martin, who recently downgraded META stock from Outperform to Hold.

According to Martin: “We lower our estimates because we believe cost growth will far exceed revenue growth for the next two years.” In addition, Martin pointed out that Meta’s moat is diminishing, causing much concern for its stock.

Although Martin’s argument should be considered, I’m bullish and support Tigress Financial’s stance on Meta stock; here’s why.

Meta in the Current Market

BlackRock’s (BLK) iShares MSCI USA Quality Factor ETF (QUAL) has Meta as one of its primary holdings, meaning that Meta is considered a high-quality stock with a robust balance sheet, a flying income statement, and dominant market share.

High-quality stocks such as Meta could be rare performers if a recession or stagflation had to occur because risk-aversion will likely cause the market’s liquidity to gravitate towards high-quality assets.

Furthermore, Meta is a “best-in-class” asset, as its presence in the technology market can’t be doubted. For example, the firm’s illustrious net income margin of 31.2% illustrates its pricing and bargaining power, which could sustain the company’s investors’ value accumulation.

Meta Platforms’ Earnings Prospects are Bright

Meta’s first-quarter results revealed a 7% year-over-year revenue increase as family app daily activity across its platforms rose 6%, and its ad impressions on its family apps surged 15% year-over-year.

According to the firm’s CEO and founder, Mark Zuckerberg: “We made progress this quarter across a number of key company priorities, and we remain confident in the long-term opportunities and growth that our product roadmap will unlock.”

Despite its maturity, Meta is still considered a secular growth company, which is conveyed by its five-year revenue CAGR (compound annual growth rate) of 31.6%. Secular growth stocks tend to brush off economic headwinds, making them exceptionally lucrative investments during uncertain times.

There’s been much concern that an economic contraction would dent Facebook’s advertising revenue as enterprise spending wanes. However, investors must bear in mind that the online advertising industry is expected to grow at a CAGR of about 11% from 2021-2026, according to a report from technavio.

This categorizes it as a high-growth domain. Moreover, Facebook is projected to own 24.1% of the ad-selling industry by 2023, which suggests that its segment earnings could be non-cyclical.

Lastly, Meta’s Beneish M-Score of -3.11 means that the firm is on the back of a period of conservative accounting practices. As such, Meta could likely surprise to the upside with a few of its following earnings releases.

Valuation Metrics Suggest Meta is Undervalued

Relative valuation metrics suggest that Meta stock is undervalued. The stock’s price-to-earnings ratio (12.4x) trades at a 55% discount to its five-year average, implying that Meta stock is trading below its cyclical peak.

Additionally, with a PEG ratio of 0.94x, the market underscores the company’s earnings-per-share growth, which leaves an earnings-driven value gap in play.

Another aspect that supports the claim that Meta is undervalued is the firm’s cash flow statement. Meta’s levered free cash flow has surged by 102% in the past year, and its price-to-cash-flow ratio is at a 58.3% discount to its five-year average, substantiating a theory that the market underscores Meta’s cash-flow-generating abilities.

Lastly, out of most of the big technology stocks, Meta seems the most reasonably priced if judged on its price-to-earnings ratio. Thus, it’s valid to conclude that the stock stacks up impressively from a peer-analysis vantage point.

Wall Street’s Take on Meta Platforms

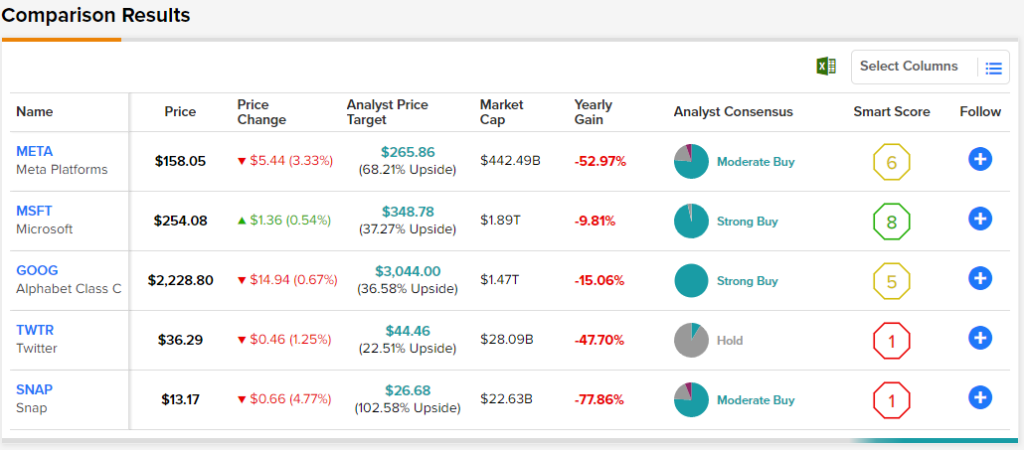

Turning to Wall Street, Meta Platforms earns a Moderate Buy consensus rating based on 29 Buys, seven Holds, and two Sell ratings assigned in the past three months. The average META stock price target of $265.86 implies 68.2% upside potential.

Concluding Thoughts – Tigress Financial May be Right

Meta has lost more than half of its market value since the turn of the year. However, the firm’s fundamentals remain robust and quantitative metrics suggest that it’s an undervalued stock. As such, Tigress Financial could be correct in predicting that the stock might surge soon.