Social media stocks have been in focus of late as they are expected to benefit from the potential ban on TikTok by the Biden Administration. Rising competition from TikTok, Apple’s (AAPL) iOS privacy update, and the impact of macro pressures on ad spending had a major impact on social media companies last year. Using TipRanks’s Stock Comparison Tool, we placed Meta Platforms (NASDAQ:META), SNAP (NYSE:SNAP), and Bilibili (NASDAQ:BILI) against each other to pick the stock that scores Wall Street’s Strong Buy consensus rating despite near-term pressures.

Meta Platforms (NASDAQ:META)

Meta impressed investors with better-than-anticipated fourth-quarter revenue. Nonetheless, weak ad spending continues to weigh on the company’s top line, which declined for the third consecutive quarter.

Meta is taking several measures to bring down costs and streamline its business to improve its profitability. The company recently announced that it will reduce its employee count by 10,000 and close about 5,000 additional roles that it hasn’t filled yet. The new round of job cuts follows more than 11,000 layoffs announced in November 2022.

Meta calls 2023 the “Year of Efficiency” and now expects its full-year expenses in the range of $86 to $92 billion, down from the prior estimate of $89 to $95 billion.

Is META stock a Good Buy?

Several analysts raised their price targets following Meta’s announcement of further job cuts. Stifel analyst Mark Kelley raised his price target for Meta Platforms to $230 from $210 and reiterated a Buy rating. That said, Kelley marginally lowered his revenue growth estimates as he anticipates some level of disruption given that a major portion of the job cuts are expected in April and May.

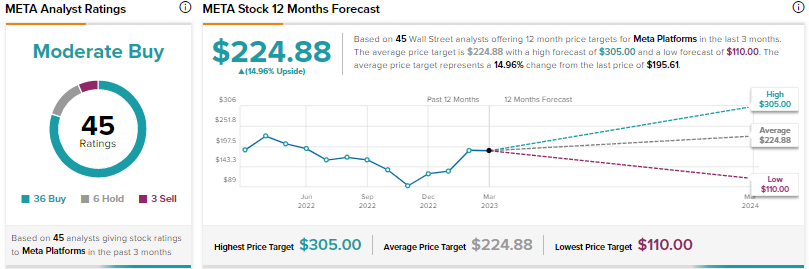

Overall, Wall Street’s Moderate Buy consensus rating is based on 36 Buys, six Holds, and three Sells. The average META stock price target of $224.88 suggests nearly 15% upside. Shares have jumped over 63% so far in 2023.

Snap (NYSE:SNAP)

Snap faced multiple headwinds last year but managed to deliver revenue growth of 12%. The company cautioned investors that it expects continued weakness in Q1 2023, with revenue projected to decline by 2% to 10% year-over-year.

At the recently held Investor Day, management discussed several themes, including augmented reality. The company is optimistic about its long-term potential and stated that at its current growth rate, it could reach over 1 billion people in the next two to three years.

It’s worth noting that Snap recently launched My AI, a new OpenAI-powered chatbot for its Snapchat+ subscribers. The new chatbot is created on the latest version of OpenAI’s GPT technology. The buzz created by OpenAI’s ChatGPT tool has made several tech giants accelerate their initiatives in the AI space.

Is Snap a Buy, Sell, or Hold?

Following the Investor Day, Truist Financial analyst Youssef Squali stated that he “walked away from Snap’s Investor Day cautiously optimistic.” The analyst noted that the company mentioned several product and monetization initiatives to revive growth supported by an expanding user base that now stands at over 750 million monthly active users.

That said, Squali prefers to remain on the sidelines, as Snap navigates current headwinds and until he starts seeing the company’s initiatives “translate into ad revenue growth again,” which he doesn’t expect until the second half of 2023.

With four Buys, 16 Holds, and three Sells, Wall Street has a Hold consensus rating for Snap stock. The average Snap stock price target of $10.63 suggests the stock could be range-bound over the near term. Shares have advanced over 19% year-to-date.

Bilibili (NASDAQ:BILI)

China-based Bilibili is one of the leading video streaming and sharing platforms in the country. The company markets itself as the online home for Gen-Z fans of anime, comics and games.

Earlier this month, the company announced its fourth-quarter results. Revenue grew 6% to RMB 6.1 billion ($890.6 million). Higher revenue from value-added services helped in offsetting the impact of lower ad revenue and a decline in revenue from mobile games due to the lack of new game launches in the quarter. Meanwhile, better cost controls helped Bilibili in narrowing its net loss by 29% to RMB1.5 billion ($217.1 million).

Bilibili ended the fourth quarter with 326 average monthly active users, reflecting a 20% year-over-year rise.

What is the Price Target for Bilibili Stock?

Earlier this month, Citigroup analyst Brian Gong upgraded Bilibili to Buy from Hold and kept the price target unchanged at $28. Gong expects the company’s Q1 2023 revenue to be roughly flat year-over-year, but projects growth to pick up from the second quarter, driven by new game launches and re-acceleration of value-added services.

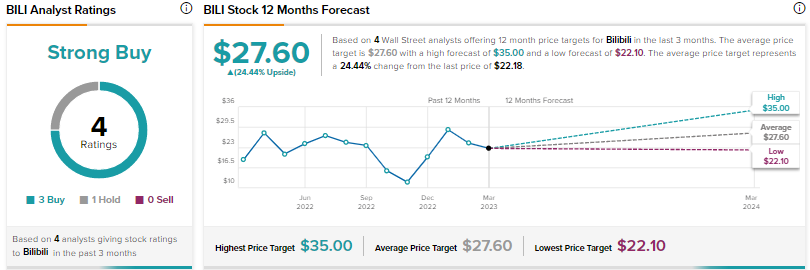

Wall Street’s Strong Buy consensus rating for Bilibili is based on three Buys and one Hold. The average BILI stock price target of $27.60 indicates 24.4% upside. Shares are down 6% since the start of this year.

Conclusion

Social media companies might remain under pressure over the near team due to the impact of macro challenges on ad spending. Analysts are very bullish about Bilibili and see higher upside potential in the stock from current levels based on narrowing losses and improvement in the top line as the year progresses.