Investors of MEI Pharma (MEIP) trudged off to the 4th of July celebrations in a downbeat mood. In last week’s final session, shares declined by 18.5%.

The announcement that MEI and its collaboration partner, the Helsinn Group, prematurely ended a Phase 3 trial of pracinostat in acute myeloid leukemia (AML) was to blame for the sell-off. Interim data showed that the candidate’s use most likely won’t lead to better overall survival rates for AML patients.

While the news was greeted by surprise at investment firm BTIG, the trial’s abrupt ending does not overly concern company analyst Thomas Shrader.

Contributing only 6% to the 5-star analyst’s model for the biotech, Shrader has another reason “patients and investors should care.” This reason is MEI’s potential treatment for patients with relapsed or refractory follicular lymphoma (FL), which is currently in a Phase 2 trial.

With the trial ongoing and expected to be fully enrolled by 1H21, Shrader’s base case involves the approval of ME-401 for FL in 2021. While MEI-401 is a PI3 delta inhibitor and belongs to a class of drugs that has been considered risky in the past, recent data supports Shrader’s bullish thesis.

“Overall, we see ME-401 in a good place in the B-Cell malignancy landscape with a very powerful PI3K inhibitor they have learned to dose safely at a time when powerful drugs are increasingly viewed favorably in earlier lines. The drug’s non-overlapping safety profile with other’s in the overall B-Cell malignancy arena (BTK and MDM-2 inhibitors) also suggests combinations are more likely to have acceptable safety profiles… We still like the story, and we are raising our probability of success (POS) for ME-401 in FL to 75% from 60% based on recent data,” Shrader explained.

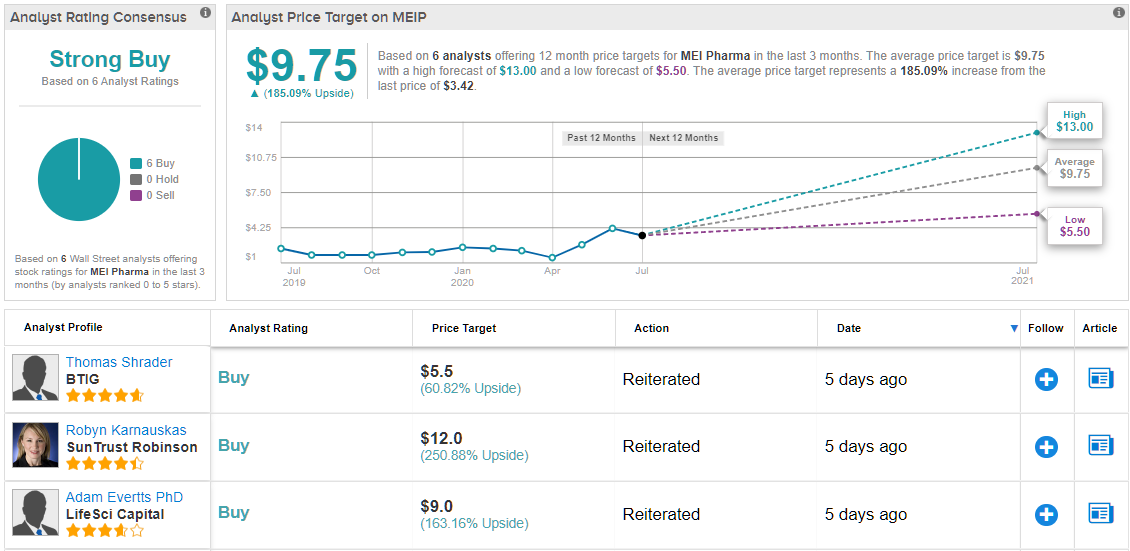

To this end, Shrader maintained a Buy rating along with a $5.50 price target. Investors could be taking home a 64% gain, should Shrader’s thesis play out over the coming months. (To watch Shrader’s track record, click here)

The rest of the Street backs up the BTIG analyst’s call. All 6 analysts tracked over the past three months rate MEI a Buy. With an average price target of $9.75, there’s massive upside potential of 185% in the year ahead. (See MEI Pharma stock analysis on TipRanks)

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.