Both Lululemon (LULU), a leading athleisure brand, and Nike (NKE), the global sportswear powerhouse, have faced significant declines in price over the past 12 months. However, Lululemon currently has a more attractive valuation and higher growth rates, although it is possible that the medium-term to long-term growth prospects of Nike could be stronger. I am bullish on both companies, with a preference for LULU stock at this time due to its higher alpha potential.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Lululemon Offers a Stronger Investment Case Than Nike

Transitioning over to a valuation perspective, I am optimistic about both Lululemon (LULU) and Nike (NKE), but right now, I see more upside with LULU stock. It has a more compelling valuation, with a P/E ratio of 19.8 compared to Nike’s 21.7. Additionally, Lululemon’s projected normalized EPS growth for the next three Fiscal years stands at around 9%, significantly higher than Nike’s 2.59%. These factors suggest that LULU presents a particularly strong investment opportunity at this time.

However, this more favorable outlook for Lululemon is largely the result of a slow year for Nike, where it is experiencing both an EPS and revenue decline for the Fiscal period ending May 2025. Based on my research, Nike has faced pressures from high inflation impacting changes in consumer preferences, including a trend toward direct-to-consumer retail, which Nike is having to invest in.

In contrast, Lululemon already has a highly successful direct-to-consumer strategy, with a robust e-commerce platform helping it control its customer relationships and margins. Moreover, Lululemon’s focus on the high-end consumer, while also targeting micro-influencers for its marketing strategies, has allowed it to develop high growth at a lower cost than if it took the celebrity-endorsement approach of Nike.

Additionally, Lululemon’s strong business strategy, focused on pricing power and lean operations, is reflected in its 16.3% net margin compared to Nike’s 11.1%. Furthermore, Lululemon’s gross margin is 58.5%, much higher than Nike’s 44.6%, showing substantial room for further net margin expansion if Lululemon can develop leaner internal operations.

To further explain, Lululemon has achieved a stronger gross margin than Nike through a premium pricing strategy based on fabric technologies and a high focus on core evergreen products that don’t change with seasons. As a result, Lululemon reduces costs related to design and manufacturing by not having to mark down prices frequently to clear seasonal inventory. Most significantly, Lululemon’s focus on distinct and technically advanced products allows its sales prices to be higher than Nike’s.

Lululemon Faces Broader Risks Than Nike

It is critical to outline that while Lululemon presents an attractive investment opportunity, it also comes with its own set of risks. Lululemon has a much smaller market cap of $31.4 billion compared to Nike’s $121.5 billion. Because of this, Lululemon is less diversified and faces more significant supply chain risks, especially as it has less negotiating power with suppliers than Nike during rising cost cycles and geopolitical upheavals. While I’m bullish on LULU stock, I acknowledge that these factors could pose challenges in the short to medium term.

Furthermore, 66% of Lululemon’s operating revenue comes from the United States. This means that it is vulnerable to the weakening state of the middle class in the country right now amid high inflation and unsustainable federal debt. I believe that over the long term, Nike may have a competitive advantage as it focuses significantly on the cost-conscious consumer, a target market it can double down on during the current cost of living crisis.

With Lululemon’s higher risk profile ascertained, it is also important to recognize that as Nike is more globally diversified than Lululemon. As a result, Nike faces more significant risks related to currency fluctuations and cultural differences in consumer preferences, which can change and be more difficult to navigate over time. In addition, Nike’s position in the market is not as distinct as Lululemon’s, and Nike faces fierce competition from established players like Adidas (ADDYY) and Puma (PMMAF).

Lululemon Faces Greater Downward Momentum Than Nike

Despite Lululemon’s strong and unique business model, the stock has experienced a nearly 50% price decline year-to-date. In contrast, Nike has only experienced a 24% decline over the period. Whether this downward momentum will continue for both companies or not is somewhat speculative, but both stocks look heavily undervalued based on my financial and valuation analysis.

In my opinion, both of these investments are worth long-term holding. However, the stronger choice at this time certainly appears to be Lululemon. Despite this, it is worth noting that Nike is expected to have higher normalized EPS growth once its contraction for the Fiscal period ending May 2025 is over, but Lululemon will likely have stronger revenue growth. I believe this state will persist until Lululemon focuses more on efficiency to drive higher earnings growth.

What Does Wall Street Say About the Stocks?

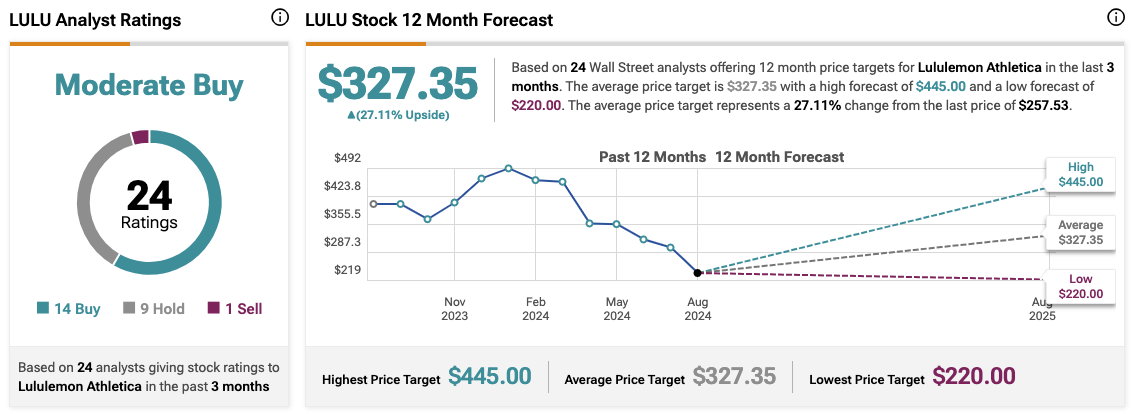

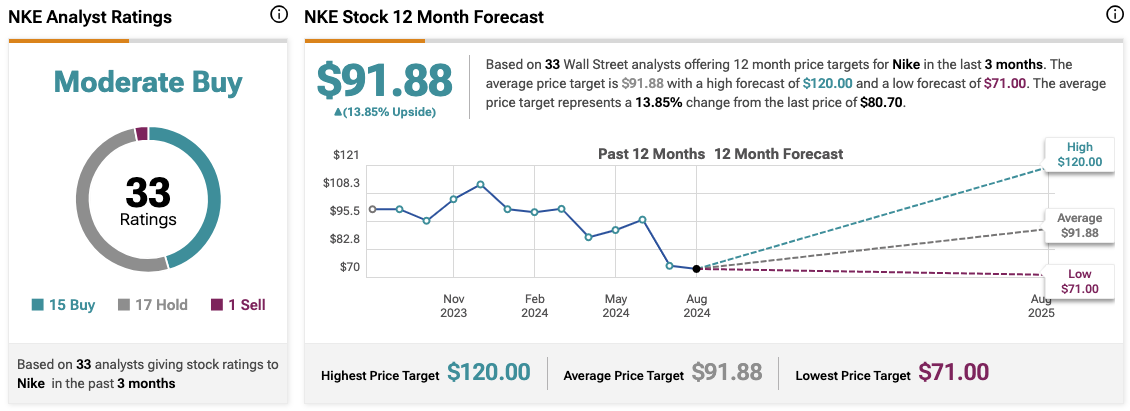

On Wall Street, both Nike and Lululemon are Moderate Buys. Nike has 15 Buy ratings, 17 Hold ratings, and one Sell rating assigned in the past three months, with the average Nike price target being $91.88, indicating a nearly 14% upside potential. On the other hand, Lululemon has 14 Buy ratings, 9 Hold ratings, and one Sell rating assigned in the past three months, with the average Lululemon price target being $327.35, indicating a 27% upside potential.

Takeaway: Lululemon Is the More Attractive Investment

Based on my analysis, both of these investments are compelling buying opportunities. However, if seeking the best alpha potential, I consider Lululemon to offer a better valuation, market position, and current growth prospects than Nike. In addition to its already strong financial position, Lululemon could also expand its net margin further through operational efficiencies to capitalize more substantially on its outstanding gross margin.