Shares of chip fabrication equipment maker Lam Research (LRCX) have been climbing steadily, now up around 20% from its $469-per-share low hit just weeks ago.

Lam Research stock flopped approximately 36% from peak to trough, but with the broader basket of chip and tech stocks enjoying a sudden relief rally, the recent momentum may be just one of many things to get excited about going into the second quarter.

Lam Research is an incredibly profitable company, with a 17.4 times trailing earnings multiple and 4.6 times sales multiple. It’s a value play with promising long-term tailwinds. Still, the cyclical nature of Lam’s business and medium-term headwinds could overpower the long-term opportunity at hand. In any case, I remain bullish.

Chip Shortage and Tech Reset Weigh

Lam Research plays a massive role in global chip production.

Ironically, Lam’s equipment production capabilities have been negatively impacted by the recent chip shortage. It needs chips to produce the equipment that other firms use to manufacture chips.

A Tough Q2 for Lam Research

With ongoing COVID-induced headwinds weighing down the second quarter, investors have had more than enough opportunity to throw in the towel. Though the second quarter was technically a slight EPS beat, the numbers were nothing to write about, with component delays and other supply chain challenges.

Despite medium-term challenges common to the entire chip industry, I think the long-term fundamentals are little changed. While it’s tough to gauge when recent supply challenges will fully dissipate, there’s no questioning the firm’s role in helping the world out of the global chip shortage.

Next-generation hardware (think 5G-enabled devices, smart vehicles, mixed-reality headsets, and wearables) are more than likely to continue fuelling the need for the latest and greatest chips. With that, the chip makers will need increased capacity. That’s where Lam comes into play as a leading WFE (Wafer Fab Equipment) producer.

Lam Research doesn’t just offer the equipment to fabricate wafers needed for chip production; it provides a wide range of semiconductor services.

In Q2, Lam’s Services revenues were up a respectable 8% on a sequential basis, with total revenues surging 22.3% year-over-year. As firms that Lam serves continue to grapple with the ongoing shortage, the Services segment should help Lam weather the remainder of the storm.

For now, the stock seems like an intriguing value option.

The Cyclical Factor

Given the hefty price tag on its equipment, Lam Research is a far more cyclical way to play the broader semi space. Some discount versus other semi companies seems warranted, but just how much of a discount is the million-dollar question.

With the U.S. yield curve flirting with inversion on Tuesday afternoon, there are cries on Wall Street that we may be running head on into a recession.

Though the U.S. Federal Reserve doesn’t want to hike interest rates in a way to send the economy into a funk, it may have no choice, as it hopes to set in place a soft landing in its fight against inflation.

A high risk of a recession and cyclical stocks are not the best combo. While no recession is guaranteed, one can’t help but keep watch on the recessionary indicator that is the yield curve. If a soft landing or no recession is in the cards, LRCX stock could prove cheap here, as it looks to power through the global chip shortage.

On the flip side, if the Fed can’t soften the blow of the rising-rate environment, Lam Research could prove one of the riskier semi plays right now, fully warranting the discount on its shares.

Wall Street’s Take

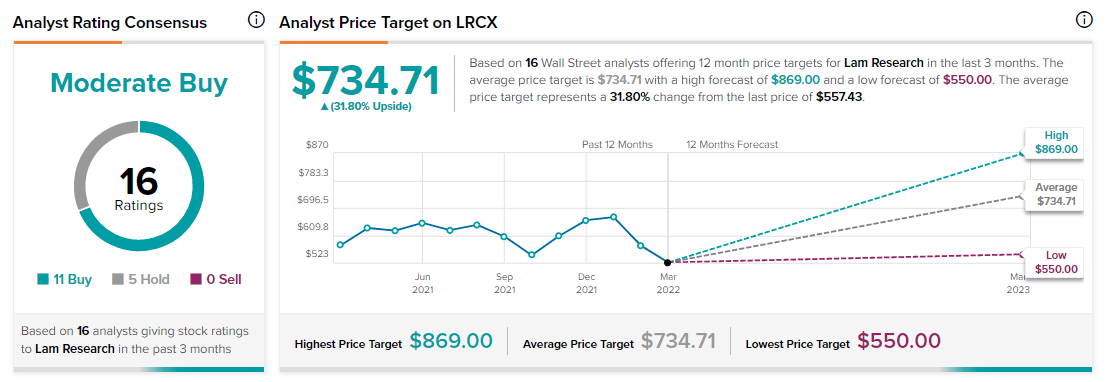

According to TipRanks’ rating consensus, LRCX stock comes in as a Moderate Buy. Out of 16 analyst ratings, there are 11 Buy recommendations and five Hold recommendations.

The average Lam Research price target is $734.71, implying 31.8% upside potential. Analyst price targets range from a low of $550 per share to a high of $869 per share.

Bottom Line on Lam Research Stock

It’s been a turbulent year for Lam Research stock, to say the least. With a healthy balance sheet and solid earnings, the company is well equipped to persevere in a world with slightly higher rates. Supply constraints should linger over the near term, but they should only get better with time.

Yes, there’s some baggage. Still, Lam stock appears to be the epitome of “growth at a reasonable price.”

The real risk, I view, is if rate hikes propel the American economy into a severe recession. If such a scenario happens, those cheap shares of Lam could become even cheaper over the next 18 months. While the light at the end of the tunnel is bright, it’s tough to gauge just how long the tunnel is, with recession risks and pesky COVID supply constraints.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure