In uncertain times, investors usually flock to securities that appear less risky and offer more predictability. Two well-established, predictable companies with a track record of delivering low-volatility results are The Coca-Cola Company (NYSE: KO) and PepsiCo (NASDAQ: PEP). However, even though they’re likely to keep producing resilient results in the coming quarters, I find the stocks to be too expensive, which could limit investors’ total returns, moving forward. Accordingly, I am neutral on both names.

The resiliency of these stocks has once again become evident during the current market downturn. While the S&P 500 (SPX) has declined by roughly 13% over the past year, The Coca-Cola Company and PepsiCo have advanced higher by around 7% each. Thus, they have overperformed significantly, and these numbers don’t include their underlying dividends paid over the past year.

Resilient Results During a Tough Environment

The Coca-Cola Company is the largest non-alcoholic beverage corporation, while PepsiCo is one of the largest food and beverage companies globally. The two companies have amassed several iconic brands in their product portfolios that usually generate resilient sales even during the toughest economic environments.

For instance, the current highly-inflationary environment is set to weaken consumer spending. Rising rates, which translate to more expensive mortgages, will further hurt consumers’ pockets. Nevertheless, consumers are likely to downsize spending on discretionary goods and services before they quit purchasing their favorite snacks and beverages.

In fact, both companies’ latest results displayed this notion, with numbers coming in strong despite the current macroeconomic setup suppressing their bottom-line growth prospects.

In its Q2 results, KO reported revenues of $11.36 billion, roughly 12% higher than Q2 2021. More impressively, organic revenues actually grew 16% year-over-year, backed by a 12% increase in pricing and mix and a 4% increase in volumes. If it weren’t for strong FX headwinds amid a strong dollar, revenue growth would have been incredible for such a mature company, but even at 12%, the top-line growth is quite impressive.

The distinctive part of Coca-Cola’s earnings report was that organic sales in EMEA (Europe, the Middle East, and Asia) jumped 21%, while North America also delivered a solid 13% gain. In fact, revenue growth was above inflation in all regions globally, which illustrated the company’s ability to generate higher sales volumes while increasing prices at rates that are above inflation.

Additionally, some investors expected that the bottom line would be compressed substantially in the current environment amid high freight expenses and wage growth. However, Coca-Cola’s world-class logistics network proved itself more useful than ever, contributing to massive cost reductions.

In fact, its comparable operating margin came in at 30.7%, just 100 bps (basis points) lower year-over-year, while comparable EPS actually grew by 4% to $0.70. This further demonstrates why investors flock to the company’s shares during economic downturns.

PepsiCo’s results also demonstrated similar qualities. Q2 revenues increased 5.2% year-over-year to $20.2 billion, primarily impacted by heavy FX headwinds amid PepsiCo’s massive international exposure. Excluding this, however, the company recorded organic revenue growth of 13%, not far from Coca-Cola’s numbers.

Among the report’s several highlights was that net revenues in Africa, the Middle East, and South Asia grew organically by 23% year-over-year. Latin America, another emerging market for PepsiCo, also reported exceptional organic revenue growth of 22%. The fact that we see such strong numbers during a global economic turmoil is quite astonishing. Snacks and beverages are truly incredibly resilient products.

Regarding its profitability, core constant-currency EPS rose by 10% as the company counterbalanced the hit of inflationary forces by focusing its actions on holistic expense-management initiatives. In my view, if inflation continues to rage, KO and PEP are likely to come out on top consistently. Their ability to retain high margins and pass any additional costs to the consumer is just wonderful.

Are Shares of KO and PEP Overvalued?

As I mentioned, the two consumer staples behemoths have advanced higher despite the overall market pacing lower. Due to these advancements, however, their valuation multiples have expanded notably. Specifically, according to consensus EPS estimates for Fiscal 2022, Coca-Cola and PepsiCo are trading at P/E ratios of about 24.2x and 24.8x, respectively.

On the one hand, it makes sense that investors are willing to pay a premium for these two companies due to their defensive characteristics. Thus, investor interest should continue to be attracted. Additionally, featuring 60 and 50 years of consecutive dividend hikes, respectively, KO and PEP have demonstrated that they can continue to grow with their payouts even during a prolonged recession, which further supports a premium multiple.

On the other hand, under normal circumstances, the two companies are unlikely to grow faster than in the mid-single digits, as has been the case historically due to them already being mature. Therefore, I believe that investors will face valuation headwinds once investors rotate sectors amid a recovery in the current macroeconomic landscape.

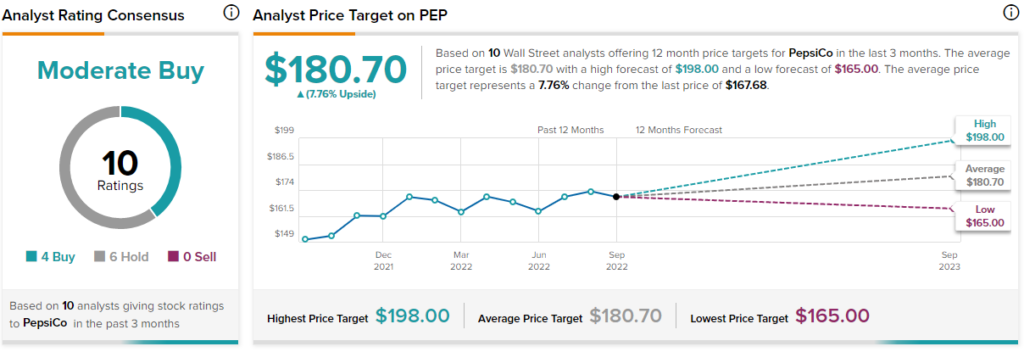

Are PEP and KO Good Stocks to Buy, According to Analysts?

Analysts are rather bullish on both names. Specifically, Coca-Cola has earned a Strong Buy consensus rating based on nine Buys and three Holds assigned in the past three months. At $70.25, the average Coca-Cola stock forecast implies a 17.5% upside potential.

Further upside is also projected for PepsiCo. The stock has a Moderate Buy consensus rating based on four Buys and six Holds assigned in the past three months. At $180.70, the average Pepsi stock forecast suggests 7.8% upside potential.

Conclusion: Quality Companies at a Steep Price

Across the board, The Coca-Cola Company and PepsiCo feature several qualities that truly make a difference during the current economic environment. Their diversified portfolios of iconic brands should keep delivering resilient cash flows, as was the case in their most recent quarters.

Still, prospective investors should be wary of their valuation multiples, as they could pressure one’s total-return potential following a multiple compression from their current, rather hefty levels.