In recent weeks, we’ve seen markets pull back after a prolonged upward trend. The reasons are varied, and include rising inflation, a weak jobs market, and the spread of the COVID Delta variant. At the same time, despite the increasing number of cases in this COVID wave, we’re not seeing a jump to lockdown policies – and while cases are up, severe cases are not.

As the danger of COVID starts to ebb, economies are starting to rev up again. JPMorgan’s global equity strategist Dubravko Lakos-Bujas noted, “While many are arguing that we are entering late cycle dynamics with broadening weakness, we believe the recent slowdown is temporary and primarily driven by the Delta variant.”

Looking ahead, however, Lakos-Bujas believes that the economic path will smooth out: “As long as Covid continues to ease, strong momentum should continue into 2022 as businesses start to rebuild depleted inventories and ramp-up capex from historically depressed levels. At the same time, cross-border activity has the potential to more meaningfully rebound for the first time since the onset of the pandemic.”

If this view pans out, we can anticipate plenty of stock opportunities in coming months. Using the TipRanks database, we’ve found two stocks that JPMorgan’s analysts have picked out for 70% or better gains. Here are the details.

Camping World Holdings (CWH)

We’ll start with a company that is well positioned to make gains in a COVID, or post-COVID world. Camping World Holdings is a retailer, specializing in RVs and related outdoor and – you guessed it – camping gear. The company is a leader in its niche, holding the largest market share, and operates through a network of brick-and-mortar stores as well as online.

CWH has shown its usual pattern in terms of quarterly revenues – with seasonal declines in Q4 and Q1 followed by gains in Q2 and Q3. The most recent report, for 2Q21, showed a company-record $2.06 billion at the top line, up 28% year-over-year, along with EPS of $2.33. The earnings per share compared favorably to the $1.53 reported in the year-ago quarter.

Strong financial performance led company management to announce measures to return profits to shareholders, through share repurchases and a dividend increase. Early in August, the company announced that it was increasing its repurchase program by $125 million, and at the end of that month declared a dividend raise, from 25 cents per share to 50 cents. The doubled dividend annualizes to $2 per common share, and yields a robust 5%.

For JPMorgan’s Ryan Brinkman, all of this adds up to a Buy rating. “CWH shares screen highly attractive on valuation,” Brinkman noted. The analyst gives CWH a $66 price target, suggesting an impressive one-year upside of 72%. (To watch Brinkman’s track record, click here)

“With margin only climbing higher since the record reached in 2Q last year — even if margin were to fall from these levels (which we do model), it is clearly now falling from a higher than previously anticipated level and with the likeliest catalyst for lower margin being improving supply, suggesting higher volume could prove an important offset, cushioning overall profit dollars from the impact of normalizing margin. We model 2022 new vehicle gross margin of 21.7% which, while down from a record estimated 25.0% in 2021, would still be by far the second strongest year on record, ahead of next highest 2020’s 18.3% and 2017’s 14.1%,” Brinkman opined.

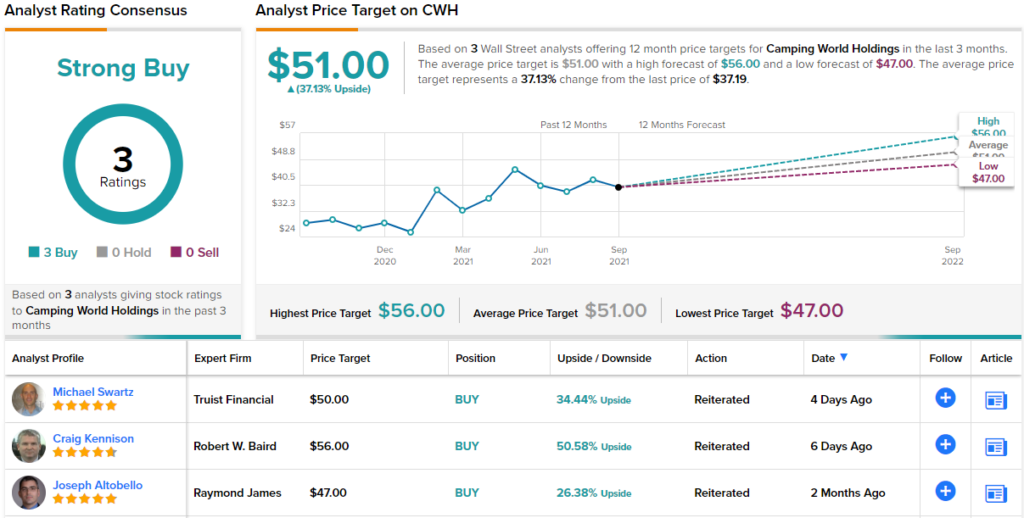

Are other analysts in agreement? They are. Only Buy ratings, 3, in fact, have been issued in the last three months. Therefore, the message is clear: CWH is a Strong Buy. Given the $51 average price target, shares could soar 37% in the next year. (See CWH stock analysis on TipRanks)

Berkeley Lights (BLI)

The second JPM pick we’ll look at is Berkeley Lights, a biotech company developing and using micro-droplet optofluidic technology to locate and culture individual cells for biomedical research. The company’s tech and services promise a revolution in the way that researchers study cells, by providing faster, more accurate, isolation, assay, and culture of single cells.

While this promising technology would seem to be a gainer for both researchers and investors, Berkeley Lights stock has fallen in recent days. The company is the subject of short selling accusations related to its IPO last summer. In that event, BLI sold 8.1 million shares – which opened at $51.05, far higher than the $22 expected initial pricing. Berkeley Lights raised over $178 million in its IPO.

The accusations raised against BLI boil down to a type of fraud, accusing the company of having ripped off both investors and customers by holding the IPO even though its flagship tech product is likely to flop. It’s important to note that, while the stock sold off 30% after the accusations, several market analysts who have been following Berkeley Lights for the past year took care to reiterate their bullish outlook on the company.

Among them is JPMorgan’s 5-star analyst Tycho Peterson, who wrote, “…we see little merit in most of the accusations made in the short report, and we believe the underlying value proposition of BLI’s Beacon platform stays intact. In fact, BLI had customers on site yesterday who expressed no concern in reaction to the [accusations]. Management remains confident in the path forward and will continue to focus on execution. While a few visibility questions remain on the newer commercialization models (subscription and partnerships), this will improve over time as the company gains more operating experience with these models. We believe the drastic stock reaction… is way overdone and creates an attractive opportunity to revisit the story.”

In line with these comments, Peterson places an Overweight (i.e. Buy) rating on BLI, and his $100 price target indicates confidence in an impressive 294% upside for the next 12 months. (To watch Peterson’s track record, click here)

Looking at the consensus breakdown, opinions on BLI are more split. The bulls come in slightly ahead, with 3 Buys compared to 2 Holds received over the previous three months. The upside potential lands at 149% as a result of its $64 average price target. (See BLI stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.