Stocks have sold off heavily since the start of this year, with a 14% decline in the S&P 500 and a bearish 22% drop in the NASDAQ. But while the selloff is broad-based, it’s not affecting everything. Oil stocks have proven resistant to the downward trend, buoyed by high prices for crude at the wellhead and gasoline at the pump. And with summer driving season underway to goose demand, and inflation rising steadily, we can expect that the high energy prices will continue for the foreseeable future.

The result is an environment in which investors need to be wary – and need to be ready to jump on any opportunity. Normally, in a stock market downturn, investors will take their chance to ‘buy the dip,’ and pick up favored equities at low cost, trusting that the market will bring gains down the line, long-term. But Jim Cramer, the well-known host of CNBC’s ‘Mad Money’ program, sees this as a poor recipe given today’s mix of market ingredients.

In recent comments on market strategy, Cramer said, “I want to be kind to this market and tell you it’s the same old buy the dips game plan. But in reality, the only dip that can be bought right now, at least, is the dip in oil.”

Of course, oil hasn’t dipped yet. Oil stocks remain high. But Cramer is suggesting a readiness strategy for investors, to keep a sharp watch for any potential dip in oil stocks. In his view, “[The] lesson is simple: Just get long on some oil stock.”

With this in mind, we’ve used the TipRanks database to pinpoint three oil stocks that are considered ‘Strong Buys’ by the consensus of the Wall Street analysts. Not to mention considerable upside potential is on the table here. Let’s take a closer look.

Matador Resources Company (MTDR)

The first oil stock we’re looking at is Matador Resources. Operating in several energy reserve regions in New Mexico, Texas, and Louisiana, this company focuses on unconventional plays in the North American hydrocarbon industry. Matador engages in exploration, development, and extraction activities, mainly in oil and liquids-rich formations. The company’s largest assets are located in the Delaware Basin of New Mexico-West Texas and in the Eagle Ford shale of South Texas.

While this company produces oil and natural gas, it generates cash – and a lot of it. Matador’s cash flow in 2021 was sufficient to pay down almost $400 million in debt. In the first quarter of this year the company paid down an additional $50 million. At the end of 1Q22, Matador had just $50 million remaining in outstanding debt on its reserves-based revolving credit facility. The company had an adjusted free cash flow in Q1 of $246 million, more than double the 4Q21 figure.

Matador generated that cash flow from its $565 million in total revenues for the quarter, up from $266 million in the prior-year quarter. The company has seen 7 quarters in a row of sequential revenue gains. This has supported a similar streak of earnings gains. Diluted EPS was $2.32 in 1Q22, up from just 71 cents in 1Q21.

This stock strikes Truist’s 5-star analyst Neal Dingmann as ripe for an acquisition, as he describes: “We forecast well over $1B of FCF this year that will allow MTDR numerous shareholder return and growth options. Further, given the company’s enviable upstream and infrastructure assets, along with larger companies’ appetites, we would not be surprised to see a premium offer for MTDR this year.”

In Dingmann’s view, this stock deserves a Buy rating, and his price target, $89, suggests a 12-month upside gain of 35%. (To watch Dingmann’s track record, click here)

Overall, it’s clear that the Street agrees with Dingmann on the investment-grade quality of this stock, as MTDR has 7 unanimously positive analyst reviews for a Strong Buy consensus rating. The average price target of $79.14 implies a 20% upside from the current trading price of $65.87. (See MTDR stock forecast on TipRanks)

California Resources Corporation (CRC)

Next up is an LA-based hydrocarbon exploration and extraction company. California Resources has operations in the San Joaquin, Los Angeles, and Sacramento Basins of its namesake state, with some two-thirds of its activities in the first-named area. The company’s holdings include proven reserves totaling approximately 480 million barrels of oil equivalent, with which 71% is crude oil and 20% is natural gas, with the remainder being natural gas liquids. CRC generated some $2.56 billion in revenue last year.

In the first quarter of this year, the company’s total operating revenues came it at $153 million, down from $363 million in the year-ago quarter. Adjusted net income was reported at $1.13 per diluted share, down from the $2.13 reported in 4Q21.

On a positive side, the company’s income supported its 17-cent per common share dividend payment, to be paid out on June 16. At 68 cents annualized, the dividend yields a modest 1.4%; the key point is that the company has embarked on a commitment to return profits to shareholders.

While fossil fuels have gotten poor press in recent years, as the source of carbon pollution, CRC has embraced a commitment to carbon management. The company is working with both private and public sector actors to reduce emissions, with a goal of full-scope net zero for 2045.

Scott Hanold, RBC’s 5-star analyst, was deeply impressed with California Resources after a recent field tour of the company’s facilities. He writes, “We were impressed by CRC’s expertise and operational/regulatory positioning across its assets. Additionally, our confidence in its ability to execute the future Carbon Management business increased, and we thought there was strong support for its initiatives. We think CRC has optimally located assets and a first mover advantage.”

Hanold doesn’t hold back in his rating on the stock, which he sets at Outperform (i.e. Buy). His price target, of $70, implies a one-year upside potential of ~49%. (To watch Hanold’s track record, click here)

The leading analyst from RBC is hardly the only one who’s taken a good impression of this oil stock. CRC has a unanimous Strong Buy consensus rating, based on 4 positive analyst reviews. The shares are priced at $46.97 and their $60.33 average price target indicates room for ~28% growth in the year ahead. (See CRC stock forecast on TipRanks)

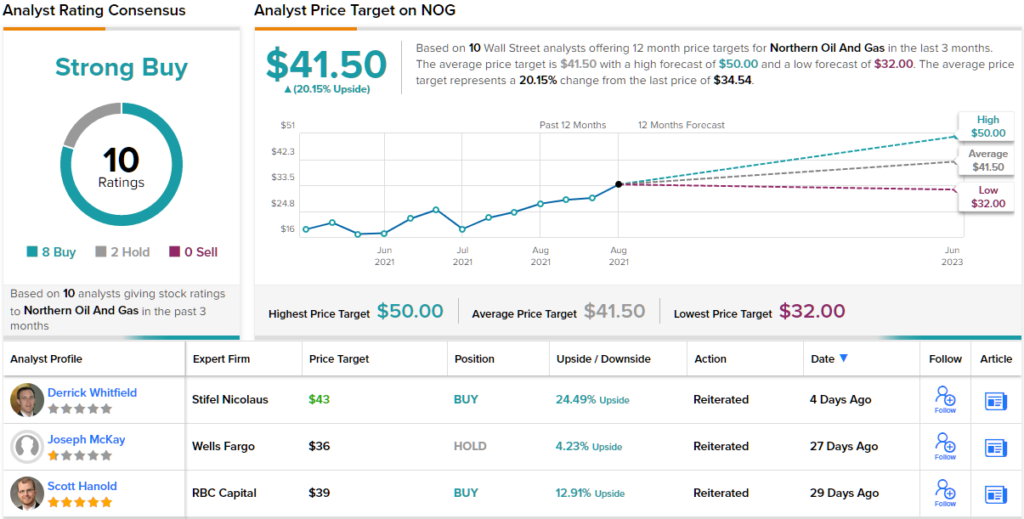

Northern Oil and Gas (NOG)

We’ll wrap up with Northern Oil and Gas, one of the many exploration companies working the hydrocarbon resources of Montana-North Dakota Williston Basin. This formation generated more than its share of headlines some years ago, when it was home to a fracking boom that put North Dakota back on the energy resources map. Northern Oil and Gas also has production holdings in New Mexico and Pennsylvania; the company is a major player in the North American shale regions, and has some 205 million barrels of oil equivalent in proved reserves.

In the first quarter of 2022, NOG’s total production reached a record level, at 71,255 Boe per day. This was up 85% year-over-year, and 60% of the total was petroleum. This production level generated a total cash flow from operations of $235 million, which represented a 49% sequential gain from 4Q21. The company’s free cash flow in Q1 was $146 million, a gain of 106% from the previous quarter.

With these numbers in mind, NOG updated its guidance for 2022 full-year production, increasing it by 1,000 Boe per day at the both the lower and upper ends, to 71,000 to 76,000 Boe.

In addition to the increased guidance, company management also bumped up the common share dividend, increasing it by 36% in the last declaration to a new payment of 19 cents per share. While the yield is only 2.2%, the size of the increase – and the fact that it was the fourth quarterly dividend increase in a row – underscores NOG’s stated policy of returning profits to shareholders. The company Board also increased the authorized repurchase plan from $68.1 million to $150 million.

All of this adds up to a situation that strikes Piper Sandler analyst Mark Lear as a sound choice for investors of all stripes. He writes, “The company has continued to demonstrate solid execution and in its deal-making and we think that progress on the capital return front will be received positively by investors.”

Lear backs his bullish stance with an Overweight (i.e. Buy) rating on the stock, and he puts a $43 price target on it. At current levels, that implies a ~25% one-year upside. (To watch Lear’s track record, click here)

With 10 recent analyst reviews, breaking down 8 to 2 in favor of Buys over Holds, Northern Oil and Gas gets a Strong Buy consensus from the Street. It’s current trading price is $34.54 and it has an average price target of $41.50, which together suggest an upside of 20% in the next 12 months. (See NOG stock forecast on TipRanks)

To find good ideas for oil stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.