Last week, the S&P 500 finished Friday’s session with a rally that gave the index a small gain of 0.15% for the day. It was a good thing, too, since the index flirted with a net-20% loss during the session. That’s bear market territory, the kind of market move that will further spook investors after a springtime of headwinds.

Inflation is running at 40-year high levels, Q1 showed a net economic contraction, Russia’s war on Ukraine promises to further damage supplies and prices in the food, cooking oil, and petroleum markets heading into summer, COVID has receded but not really gone away, and China’s activities – a combination of strict anti-COVID lockdown policies and geostrategic aggression on several fronts – is exacerbating all of these factors.

Market pundits are not just talking about a likely recession, they are tossing around the idea of stagflation, that poisonous combination of inflation, high unemployment, and economic contraction that we haven’t seen since the Carter Administration.

While the market situation is starting to grow grim, however, JPMorgan global markets strategist Marko Kolanovic sees potential for risk-friendly investors.

“Equity markets price in too much recession risk: We estimate US and Euro area equity markets are pricing in a ~70% probability of a near-term recession, compared to ~50% in HG credit, ~30% in HY, and ~10-20% in rate markets. We are also skeptical of the idea that April’s equity fund outflow, the highest since March 2020, is only the beginning of a more protracted phase of outflows. We therefore maintain a pro-risk stance,” Kolanovic wrote.

“If recession doesn’t come through, multiple derating was already very substantial, and given the reduced positioning and downbeat sentiment, Equities stand to recover from here,” Kolanovic added.

In addition to Kolanovic’s look at the macro situation, JPMorgan’s stock analysts have also been diving into three stocks that are down, but are still showing strong upside potential, on the order of 90% or better for the year ahead. Using TipRanks’ database, we found out that the rest of the Street is also on board as all three have earned a “Strong Buy” consensus rating.

ACV Auctions (ACVA)

The first stock we’ll look at, ACV Auctions, brings the wholesale auto dealer auction to the online realm, a move that makes the wholesaling process both faster and more transparent, benefiting both dealers and buyers in the long run. ACV’s subsidiary companies handle every aspect of the wholesale auction process, from transporting vehicles to and from, to providing third-party inspections of those vehicles, to managing the auctions – and even down to providing financing for the buyers.

While ACV fills a necessary niche, and the company’s revenues have trended upwards over the past year, the stock has fallen considerably in that time. ACV went public at the end of March in 2021, an since then, the stock is down 74%.

The share-price drop has come even though, as noted, revenues have gained. The company reported $69 million at the top line in its first public quarterly report, for 1Q21. In the most recent report, for 1Q22, that top line came in at $103 million, an impressive gain of 49%. Investors, are worried, however, by the company’s deepening net losses. In that first publicly reported quarter, the total GAAP net loss came to $17 million. It was $26.3 million in 4Q21, and increased to $29 million in 1Q22.

Not every net loss is a net negative. ACV has a history of smart spending, with investments in online tech and sales tools to improve its quality of service. This is the key point for JPMorgan analyst Rajat Gupta, who writes, “Despite the continued uncertainty around the wholesale industry, ACVA continues to invest prudently in new tools and offerings for customers and market share expansion remains on track, which should ultimately bode well when the market eventually recovers. There is no change to our view on the L-T story, which remains compelling given the sizeable ~22 mn addressable market with <10% online penetration today.”

In line with these comments, Gupta gives the stock an Overweight (i.e. Buy) rating, with a $15 price target suggesting a one-year upside of ~91%. (To watch Gupta’s track record, click here)

JPM’s view is hardly an outlier here. The stock has 10 recent analyst reviews, and they are unanimously positive, for a Strong Buy consensus rating. The shares are priced at $7.92 and their $18.90 average price target implies an upside of ~140% for the next 12 months. (See ACVA stock forecast on TipRanks)

Boot Barn Holdings (BOOT)

Image matters, and people will pay the image they want. That’s the secret behind lifestyle retail – and it’s a secret that Boot Barn Holdings understands well. The company is a fast-growing retail chain offering a line of western-styled footwear and apparel, as well as work clothes and accessories. Boot Barn has over 300 locations across 38 states, and in its fiscal year 2022 it reported total revenues of $1.48 billion.

That total included strong year-over-year gains in each quarter, as consumers got back to shopping with the lifting of COVID restrictions. In the most recent quarter reported, fiscal 4Q22, the company showed $383.3 million at the top line, a year-over-year revenue gain of 48%.

The company is profitable, too. The net income of $44.7 million in fiscal Q4 was up 81% from the $24.6 million in the year-ago quarter, and translated to a diluted EPS of $1.47. The company saw its same-store sales grow by 33% in the quarter, and 53% in the fiscal year. Despite these positive metrics, however, the market downturn has pushed BOOT shares down 41% so far this year.

That just opens up a chance for investors to get in while the getting is good, according to analyst Matthew Boss. Writing for JPMorgan, Boss described BOOT as ‘Top Small Cap Growth Idea,’ and writes at the bottom line: “With about 90% of sales at full price, 30% of assortment work wear, and its western offering differentiated given its niche positioning (and destination nature of its store base), BOOT targets steady merchandise margin improvement over time combined with low fixed-cost hurdles to drive EBIT margin expansion toward 10%+ over time.”

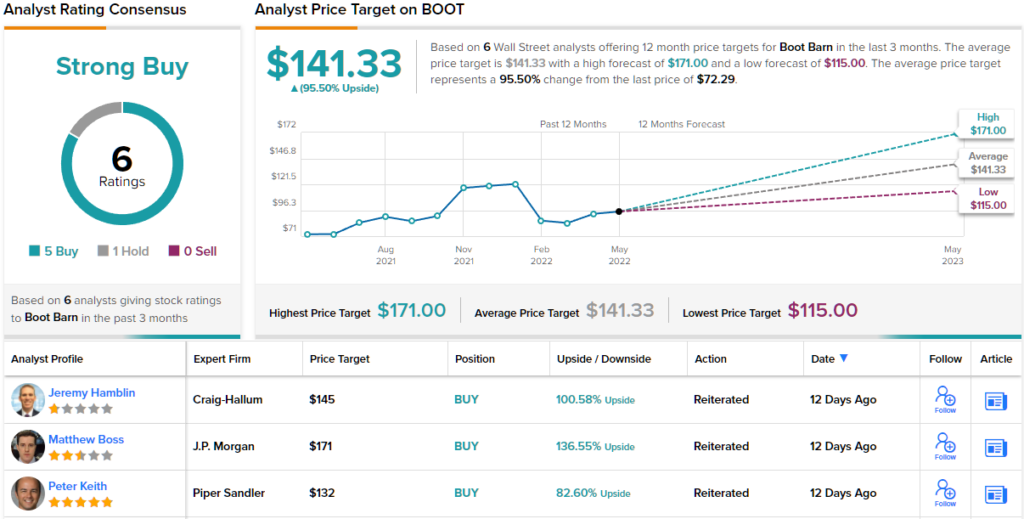

These comments support Boss’ Overweight (i.e. Buy) rating, while his $171 price target implies an upside of ~135% by year’s end. (To watch Boss’s track record, click here)

Other analysts are on the same page. With 5 Buys and 1 Hold received in the last three months, the word on the Street is that BOOT is a Strong Buy. Shares are currently priced at $72, and the $141.33 average price target suggests double-digit growth of ~95%. (See BOOT stock forecast on TipRanks)

Springworks Therapeutics (SWTX)

We’ll wrap up in the biopharma industry, where Springworks is a clinical-stage research firm developing new treatments for rare diseases, including various cancers. The company operates both by developing new drug candidates and acquiring rights to existing programs, and moves the drug through the clinical research stages to the commercialization process.

Springworks has two main drug candidates, both in early- and late-stage clinical trials, which trials conducted by both Springworks along and in conjunction with other drug companies. The more advanced of the two, nirogacestat, is a gamma secretase inhibitor with no fewer than 10 research tracks ongoing.

The farthest along is a Phase 3 monotherapy study in the treatment of adult desmoid tumors. This study, the DeFi trial, has its primary endpoint progression-free survival. The company expects to release topline data in 2Q22. In addition to this trial, the company is recruiting for a Phase 2 trial in pediatric patients with desmoid tumors. This trial will conducted in conjunction with, and sponsored by, the Children’s Oncology Group. Finally, Springworks is working with GSK on a randomized Phase 2 cohort expansion trial of nirogacestat in combination with BLENREP against multiple myeloma. The company expects to release data on these studies at the American Society of Clinical Oncology meeting in June.

In addition to the nirogacestat programs, Springworks is developing mirdametinib as an MEK inhibitor. The two most advanced tracks here are the Phase 2b ReNeu trial and the ongoing Phase 1/2 trials in children with pediatric gliomas. The ReNeu trial is fully enrolled and will evaluate the drug as a treatment for adults and children with Neurofibromatosis type 1-associated plexiform neurofibromas. The Phase 1/2 study is being conducted in collaboration with BeiGene, and is evaluating mirdametinib as a treatment for a variety of malignancies, including refractory solid tumors harboring RAS mutations, RAF mutations, and other MAPK pathway aberrations.

Despite the highly diverse and active pipeline, Springworks shares have fallen 53% over the last 12 months. However, JPMorgan analyst Anupam Rama thinks this low stock price could offer new investors an opportunity to get into SWTX on the cheap.

“SWTX shares remain on the J.P. Morgan Analyst Focus List ahead of the busy ~4-6 weeks, with likely multiple key data readouts anticipated. In our view, the phase 3 DeFi study has a high probability of success and the initial BCMA combination data could underscore multiple modality catalysts for the program over the next ~6-18 months,” Rama opined.

To this end, Rama rates SWTX an Overweight (i.e. Buy), and sets a $98 price target that implies an upside potential of ~166% this year. (To watch Rama’s track record, click here)

All in all, this small-cap biopharma has slipped under the radar a bit, and only has 3 recent analyst reviews. They all positive, however, and back the stock’s Strong Buy consensus rating. The shares are trading for $36.81 and the $116.67 average price target suggests a powerful 218% gain for the months ahead. (See SWTX stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.