Like a dance partner falling down, cryptocurrency exchange Coinbase (NASDAQ:COIN) is only as healthy as the underlying sector allows it to be. Unfortunately, with both blockchain-based assets and rival platforms imploding, the narrative imposes severe pressure on COIN stock. Therefore, it’s time for investors to wake up to the harsh reality. I am bearish on Coinbase.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

While hope springs eternal in the crypto sphere, those anticipating a reprieve in COIN stock may be found waiting indefinitely. Structurally, the underlying company finds itself in an incredibly tight spot. Unlike the stock market, the virtual currency arena doesn’t conveniently offer opportunities to trade both sides of the aisle.

Log onto Coinbase, and users will find plenty of cryptos to buy. However, they will not be able to easily short digital assets without putting up collateral and engaging in complex transactions.

Under a bullish cycle, the inability to short the market in question won’t represent that much of a hindrance. After all, if assets rise, people tend to go long rather than short. However, when the sector melts down, the one-way street of popular retail crypto exchanges essentially shuts out participation. Indeed, many folks turned to safekeeping their cryptos in cold storage wallets rather than trading them.

As a result, it’s not just Coinbase suffering from a liquidity and engagement crunch; the overall blockchain ecosystem succumbed to a lack of interest. To be fair, it’s very much possible that this interest can rise again. However, this might take years, and COIN stock desperately needs help now.

Sadly, the news cycle won’t cooperate, clouding Coinbase’s viability.

COIN Stock May Suffer from the FTX Fallout

Although the broader blockchain industry incurred several failures and catastrophes in the past, none might be as painful as the FTX implosion. Once one of the world’s largest crypto exchange, the platform recently filed for bankruptcy. Per TipRanks reporter Sheryl Sheth, FTX announced that it owed roughly $3.1 billion to its 50 major creditors. Adding to the ignominy, Sheth noted that FTX has more than a million creditors combined across all its platforms. While COIN stock represents a completely different entity than FTX, the latter’s fallout will likely negatively affect the former.

Part of the reason – perhaps most of the reason – comes down to psychology. Unlike dollars held in a bank, the Federal Deposit Insurance Corporation (FDIC) does not insure virtual currencies. Thus, it’s quite possible to be a millionaire one day and a penniless pauper (if you have all your eggs in one basket) the next.

Moreover, akin to navigating a minefield, both investors and users have no way of knowing beforehand whether their crypto platform will fail. Particularly for those that have significant funds in these now-questionable services, it makes sense to cash out and be safe. The consequences of being sorry are too severe in the crypto realm.

Not surprisingly, Bank of America Securities’ Jason Kupferberg “thinks risks are increasing for the company amid falling investor faith in digital assets and a rising regulatory spotlight,” as TipRanks reporter Kailas Salunkhe mentioned.

Taken as a whole, COIN stock may suffer from a double whammy: investors exiting as well as crypto users. With risks of crypto exposure (either directly or indirectly) skyrocketing, the rewards become exponentially less enticing.

Financial Data Clouds Coinbase

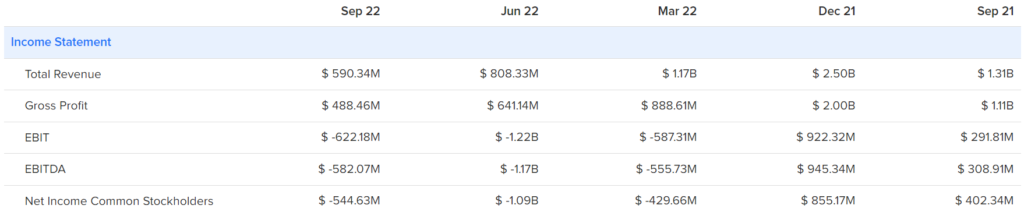

Fundamentally, it should already be enough that one’s investment can implode overnight to warrant extreme caution on COIN stock. However, for the stubbornly committed, such investors only need to consider the financial picture and its correlation with crypto valuations. Between the third and fourth quarters of 2021, Coinbase’s revenue increased from $1.31 billion to just under $2.5 billion. Likewise, the market capitalization of all cryptos soared from around $1.8 trillion in late September to just under $3 trillion in early November.

Since then, however, cryptos have succumbed to bearish pressure. Like clockwork, Coinbase’s top line shrank. From Q4 2021’s near-$2.5 billion sales tally, Q1 2022 came in at $1.17 billion. Later, in Q2, revenue slipped to $808 million. Most recently, for Q3, revenue slipped again to $590 million.

You don’t need to be a mathematics expert to recognize what’s going on. As demand for cryptos fades, so too does the demand for Coinbase’s services. In turn, investors exited out of COIN stock, fearing a long winter for the blockchain ecosystem.

To be clear, some contrarians might interpret the volatility in COIN stock as a discounted opportunity. Should Coinbase avoid melting down like its embattled peers, a turnaround may be in the works. However, the Federal Reserve must cooperate by implementing a dovish monetary policy. Unfortunately, with the central bank tightening, cryptos will likely swim in red ink.

Is COIN Stock a Buy?

Turning to Wall Street, COIN stock has a Moderate Buy consensus rating based on nine Buys, seven Holds, and three Sells assigned in the past three months. The average COIN price target is $75.82, implying 75.88% upside potential.

COIN Stock is a High Risk, Low Reward Investment

Ultimately, the narrative for COIN stock comes down to high risk and low reward. Without a robust interest in cryptos, Coinbase’s revenue channel will take a beating. Further, those holding cryptos in Coinbase will likely wonder about FTX and its implications. Therefore, at the moment, very little incentive exists for exposing yourself to this investment idea.