The growth of e-commerce over the past two decades has been enormous. The convenience of having any item delivered to your doorstep is irreplaceable. With e-commerce companies striving to capture this ever-growing market by delivering the most attractive propositions possible to consumers, such as Amazon (NASDAQ: AMZN) with its Prime subscription, e-commerce sales have been explosive compared to retail.

As online shopping became more convenient, accessible, and scalable over the years, consumers became increasingly reliant on fast deliveries, taking this new comfort for granted. However, behind every next-day order delivery to your doorstep that was sent through the process of a single click, there is a massive infrastructure in place to make it possible.

Up until 2020, the pace of e-commerce growth and the expansion of the underlying infrastructure were mostly going hand in hand. With the COVID-19 pandemic disrupting this balance, companies in the space are still heavily impacted, despite the pandemic having eased.

What Still Causes the Current Supply-Chain Bottlenecks?

To begin with, let’s explain what caused the massive supply-chain issues during the pandemic and then why these issues are still in place even though the world has mostly advanced to a post-COVID era.

The first part is easy to answer. The working-from-home economy led to a surge in demand for fast, reliable, and serial home deliveries of any kind. As retail locations suffered mandatory closures and a large part of the workforce was told to stay inside, consumers turned to e-commerce sites even for their most trivial needs.

Simultaneously, all the infrastructure in place to fulfill these orders saw its optimization and efficiency diminish. With many ports, postal offices, transportation hubs, and airlines operating at limited capacity amid a lack of available workforce and COVID-19 protection measures, fulfilling the ever-pilling backlog of orders on time became impossible. Hence the hundreds of containerships waiting for weeks outside the ports to unload their goods.

However, with COVID-19 easing, why do e-commerce companies continue to suffer from supply-chain bottlenecks? In my view, there are three major catalysts powering this issue.

Firstly, as consumers developed a habit of ordering everything online, order volumes have remained elevated, even though they have come down from their highs. It will take years for the underlying development of infrastructure to catch up.

Secondly, the existing infrastructure in place lacks an adequate workforce. Workers now require higher salaries, fewer working hours, and less demanding jobs. Lately, for instance, dockers at the UK’s most active container port went on strike, demanding pay rises. Such events occur all across the globe, further pressuring the supply chain.

Finally, and the most important factor, in my view, is that the container ship owners and operators have gained all the leverage in the world out of this situation, charging outrageous freight rates. To better understand why this is the case, there are two types of companies in the space.

Firstly, there are the liners. These are the companies that actually operate the vessels on a schedule with a set port rotation. Then, there are the container ship lessors, which are the companies owning the vessels and leasing them to the liners. Of course, some liners own vessels as well, but for various reasons we won’t go into, leasing has become the industry standard lately.

Liners such as ZIM Integrated Shipping Services Ltd. (NYSE: ZIM) took advantage of the underlying supply-chain bottlenecks to profit big time. To demonstrate how enormous the increase in rates was, ZIM IPO’d at $15 per share in January of 2021 and, by the end of the year, had paid $19.50 in dividends per share. With COVID-19 easing and the supply chain somewhat improving from its worst days, freight rates should also be easing, right?

Well, here’s why this won’t be the case anytime soon. While liner companies usually operate short-term contracts (i.e., move cargo from port A to port B), container ship lessors lease their vessels under long-term contracts. In fact, capitalizing on the massive shortage of available vessels and port congestions, lessors such as Danaos Corporation (NYSE: DAC), Global Ship Lease, Inc. (NYSE: GSL), and Euroseas Ltd. (NASDAQ: ESEA), locked-in outrageously expensive leases, with many of them lasting as far as 2027 and beyond.

Thus, for liners to at least cover their lease liabilities in the coming years, it’s quite likely that their rates will also remain sky-high, moving forward. In fact, even though freight rates have somewhat “normalized” lately, they still remain more than 200% higher than their pre-pandemic levels.

What Does This Mean for E-Commerce Stocks?

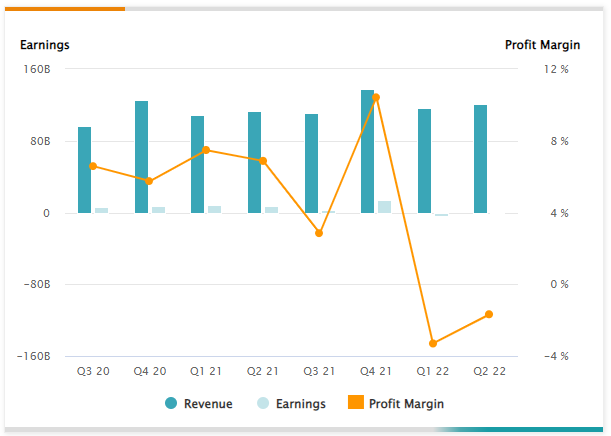

The catalysts just discussed have had a major impact on e-commerce stocks. Specifically, inventory management issues amid the disruption of the supply chain and elevated freight costs are still a significant drag on margins. Amazon’s North American segment saw its operating margins fall from 4.7% to -0.8% in Q2. In its International segment, operating margins fell from 1.2% to a negative (6.5%).

Target’s (NYSE: TGT) operating margin also fell from 9.8% to 1.2% due to higher freight costs in its most recent quarter. Take any company in the space you like, and the effect on margins is more or less the same.

In my view, and based on the current logistics landscape, the margins of e-commerce companies are going to remain considerably impacted in the coming quarters. In turn, this should sustain softened net income growth expectations and compressed valuation multiples.

Thus, investors should be wary when it comes to allocating capital to e-commerce stocks and be well informed regarding the underlying situation of the supply-chain landscape.