Halliburton Company (HAL) stock is up more than 23% so far this year, helped by strong tailwinds in the oil and gas markets.

Halliburton fell sharply from its June peak, following a drop in fossil fuel prices, but factors such as rising oil and gas prices and rising demand are expected to play out throughout the year and help the stock regain better shape.

So I’m bullish on Halliburton as the stock looks cheap given its profitable operations amid a rosy outlook for oil and gas international markets.

Rosy Fossil Fuels Markets Prospects: Expected Higher Demand

Ongoing geopolitical issues will continue to drive up oil and gas prices, fueling the interest of the oil and gas drilling and exploration industry in accelerating operations to meet growing global energy needs.

Halliburton is well positioned to take advantage of the above as it profitably provides equipment and services needed by oil and gas explorers and miners to help many countries solve their energy problems caused by the following circumstances.

The escalating conflict between Ukraine and Russia, which began on February 24, has led to political decisions and caused technical problems on the Nord Stream pipeline, affecting the sourcing of Russian gas. As a result, Europe must now source additional gas outside of Russia, including supplies from the United States in the form of liquid stocks.

In addition, the demand for oil and gas is being stimulated by increases in air travel due to the holiday season, the resumption of Chinese industrial activities after COVID-19 restrictions, and the need for countries to stock up on enough raw materials for the winter season.

Founded more than a century ago, Halliburton is a supplier of equipment and services to the oil and gas industry, operating as one of the largest in the world.

Q1 2022: Excellent Performance Thanks to Profitable Operations

Thanks to Halliburton’s competitive positioning in the North American and overseas markets, which fully compensated for weather and supply chain disruptions, the company delivered excellent performance across all segments.

Halliburton reported revenue of $4.3 billion in the first quarter of 2022, up 23% year-over-year, while operating income was $511 million, up 38% year-over-year. Since operating income outpaced sales, the margin has also improved.

Revenue exceeded analysts’ median forecast by $80 million and pro forma earnings per share (EPS) of $0.35 (up from $0.19 in the year-ago quarter) beat analysts’ median estimate by $0.01.

The company expects strong tailwinds from international markets through the end of 2022, which should support expectations for profitable growth while delivering strong free cash flow and yields above industry averages.

As a result, the dividend to shareholders is expected to increase further, following the rise of 166.7% year-over-year to $0.12 per common share, which was issued on June 22, 2022. The payment, as of this writing, generates a 1.18% dividend yield versus the S&P 500’s 1.67% yield.

The company has consistently increased its dividend for 32 years.

The Balance Sheet Appears Solid

Halliburton’s balance sheet looks solid at $2.2 billion in cash and equivalents despite being weighed down by $9.6 billion in total debt.

The discrepancy doesn’t impact shareholders as the company operates in a capital-intensive industry, so it’s normal to have such high leverage exposure.

At 4.23, the interest coverage ratio, which measures the degree of debt sustainability in terms of the ability to pay the interest due, is well above the acceptable minimum limit of 1.5.

Additionally, the Altman Z-Score of 2.95 suggests a gray area, meaning the company is under some sort of financial stress but not in danger of going bankrupt.

The ratio measures the probability that the company will no longer be able to continue its business activities and will have to shut down permanently due to bankruptcy. A ratio below 1.79 would instead indicate trouble spots and a high risk of bankruptcy. A ratio above 3 indicates a safe area and no risk of bankruptcy.

For the debt-to-EBITDA ratio, which measures the company’s ability to pay off its debt, a score of 3.47 means it will take Halliburton approximately 3.5 years to pay off all debt through EBITDA. This span of time is considered acceptable as the ratio should ideally be less than 4.

The ratio is calculated as the total debt of $9.6 billion (as of March 31, 2022) divided by annualized EBITDA (as of March 31, 2022) of $2.76 billion.

This level of financial leverage will improve over time, supported by favorable oil and gas prices and projected higher demand for these commodities. This could potentially act as a powerful catalyst for higher stock prices.

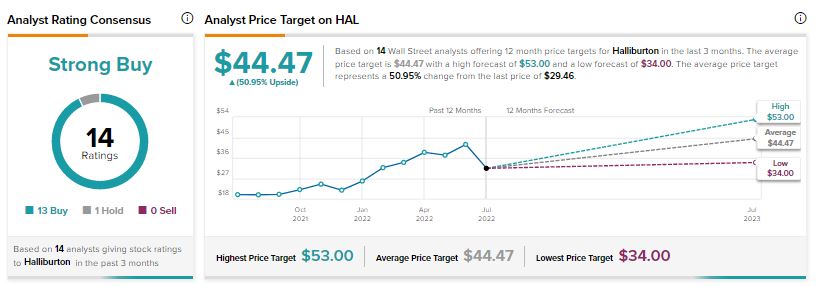

Wall Street’s Take

In the past three months, fourteen Wall Street analysts have issued a 12-month price target for HAL. The stock has a Strong Buy consensus rating based on thirteen Buys and one Hold.

The average Halliburton Company price target is $44.47, implying a 50.95% upside potential.

Valuation – Great Chance of a Bargain

After a sharp fall of about 33% from its all-time high of $42.97 on June 8, the stock is currently cheaper than it was a few weeks ago, according to the stats below.

The stock price is currently trading 6-7% below the middle point ($30.905) of the 52-week range of $17.82 to $43.99.

Compared to the 50-day moving average of $35.04, this stock price is down about 17.7%, while it is still down compared to the 200-day moving average of $30.87, but by a smaller margin of about 6.5%.

Also, the forward (fwd) PE ratio of 15.38, calculated as Monday’s closing price divided by estimated full-year 2022 earnings per share (EPS) of $1.89, suggests that this stock is trading cheap.

The ideal value for a good fwd. P/E ratio is any value below the market average, which is currently between 20 and 25.

This, coupled with a benign oil and gas price outlook, increases the likelihood that the forward P/E ratio will prove us right on the opportunity to get a bargain on the Halliburton Company purchase today.

Technically, there seems to be plenty of room for strong upside potential going forward, as Halliburton Co’s 14-day Relative Strength Indicator (RSI) of 38.68 (at the time of writing) says the stock is anything but overbought.

The indicator ranges between 30 and 70. A reading of around 30 means the stock is oversold, while a reading of 70 means the stock has approached the overbought level.

Conclusion –Cheap with Strong Upside Potential

The Halliburton Company is poised for growth as its operations remain profitable on a rosy fossil fuel backdrop.

These factors make this stock cheap and worth buying.

Read full Disclosure